A Japanese Lab Just Cracked the 100-Year-Old Insulin Pill Problem — But Can It Survive the Leap From Mice to Humans?

Summary

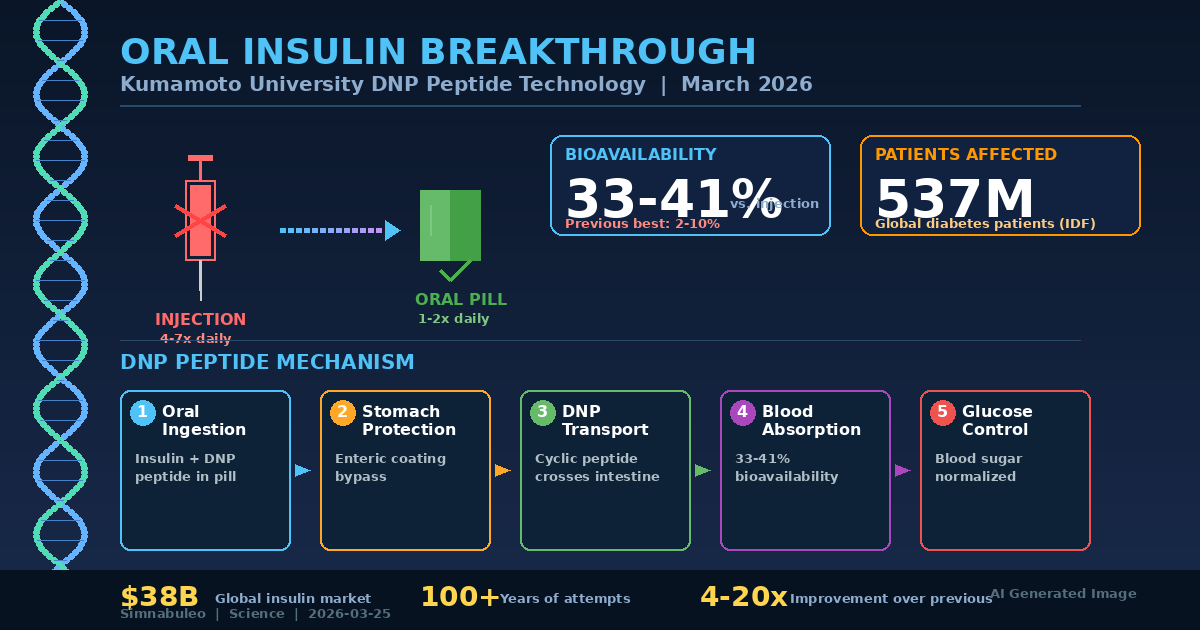

Kumamoto University's DNP peptide technology pushed oral insulin bioavailability to 33–41%, a range previous attempts never reached. In a field littered with a century of failures, this research deserves serious scrutiny — what makes it different, and what does it mean for 537 million diabetes patients worldwide.

Key Points

Breaking Through a Century-Old Barrier

Since insulin's discovery in 1921, oral delivery has been considered virtually impossible. Stomach acid destroys insulin's 3D structure, and the intestinal epithelium blocks absorption of proteins with a molecular weight of 5,808 daltons. Oramed's ORMD-0801 failed in Phase 3 in 2023, unable to beat placebo, and all previous attempts plateaued at 2-10% bioavailability. Kumamoto University's achievement of 33-41% represents the first meaningful crack in this wall — a 4-20x improvement over any prior technology.

A Fundamentally Different Mechanism: DNP Peptide Transport

Unlike previous approaches that forced open tight junctions or wrapped insulin in protective shells, the DNP peptide exploits existing intracellular transport pathways in the small intestine. This cyclic peptide does not artificially open the gut barrier, avoiding the side effect of unwanted substance absorption. The technology was validated through two independent methods — simple mixing with zinc-stabilized insulin hexamers and covalent conjugation via click chemistry — both producing equivalent blood glucose normalization in diabetic mouse models.

537 Million Patients and the Compliance Crisis

According to the International Diabetes Federation, 537 million adults have diabetes globally, projected to reach 783 million by 2045. Type 1 patients inject 4-7 times daily; Type 2 insulin-dependent patients inject 1-3 times. Approximately 30% of insulin injection patients experience needle anxiety (trypanophobia), with a significant portion delaying or discontinuing treatment. Oral conversion could dramatically improve treatment adherence, particularly among pediatric and elderly patients.

A $38 Billion Market Poised for Disruption

The global insulin market is worth approximately $38 billion, with the total diabetes drug market reaching $116.1 billion. Oral insulin would reduce cold-chain distribution dependency, dramatically improving access in sub-Saharan Africa, Southeast Asia, and Latin America. The WHO estimates that roughly half of patients who need insulin lack adequate access. The DNP platform extends beyond insulin to other protein therapeutics including GLP-1 receptor agonists, potentially addressing a market worth hundreds of billions.

The Mouse-to-Human Chasm Remains Wide

Preclinical-to-clinical failure rates in biopharmaceuticals reach approximately 90%. The mouse small intestine measures about 35cm versus 6-7m in humans, with fundamentally different gut microbiome environments. If human bioavailability drops to 15-20%, the advantage over previous technologies narrows considerably. Insulin's narrow therapeutic window — where dosing errors can cause fatal hypoglycemic shock — combined with oral absorption variability poses serious safety concerns. Commercialization is estimated at 8-12 years with $1-2 billion in development costs.

Positive & Negative Analysis

Positive Aspects

- Elimination of needle phobia and dramatic compliance improvement

Approximately 30% of insulin injection patients experience trypanophobia (needle anxiety), with many delaying or discontinuing treatment. Replacing 4-7 daily injections with 1-2 oral doses could dramatically transform quality of life. This is particularly impactful for pediatric diabetes patients and elderly patients with limited dexterity. Long-term, improved compliance would reduce diabetic complications (neuropathy, retinopathy, nephropathy), generating substantial healthcare cost savings.

- Revolutionary access improvement for developing nations

The WHO reports that approximately half of patients who need insulin cannot access adequate treatment due to supply and infrastructure limitations. Oral insulin would dramatically reduce dependence on cold-chain distribution networks, transforming insulin availability across sub-Saharan Africa, Southeast Asia, and Latin America. The elimination of needle and syringe medical waste disposal burdens is an additional significant benefit for resource-constrained healthcare systems.

- DNP platform extensibility: biopharmaceutical paradigm shift

The DNP peptide technology is not limited to insulin. It could serve as an oral conversion platform for GLP-1 receptor agonists (semaglutide, tirzepatide), growth hormones, and antibody fragments. The current oral semaglutide (Rybelsus) has a bioavailability of only about 1%, requiring high-dose formulations. If DNP technology dramatically improves this, the addressable market — including the obesity treatment space — expands into the hundreds of billions of dollars.

- Technical elegance and favorable safety profile

While previous methods artificially opened tight junctions — allowing unwanted substances to pass through alongside insulin — the DNP peptide leverages the small intestine's existing intracellular transport pathways, avoiding this side effect entirely. The validation through two independent methods (mixing and click chemistry conjugation) demonstrates platform robustness and opens multiple commercialization pathways with different manufacturing and pharmacokinetic profiles.

- Reassertion of Japan's global biotech competitiveness

Japan has a long tradition in Drug Delivery Systems (DDS) but has received less global attention recently compared to US and European biotech firms. Kumamoto University's breakthrough, if successfully translated into a commercialization pathway, could serve as a catalyst for rebuilding Japan's global positioning in the biopharmaceutical sector. Licensing interest from major Japanese pharma companies like Takeda and Astellas is anticipated.

Concerns

- The 90% preclinical failure rate and mouse-human translation gap

The preclinical-to-clinical failure rate in biopharmaceuticals is approximately 90%, and the oral insulin field is particularly notorious for wide translation failures. The mouse small intestine (35cm) versus human (6-7m) length difference, fundamentally different gut microbiome environments, and variations in meal content, intestinal motility, and individual microbiome composition create variables that mouse studies cannot fully capture. There is no guarantee the 33-41% bioavailability will hold in humans.

- Insulin's narrow therapeutic window and hypoglycemic shock risk

Insulin has a narrow therapeutic window where even slight dosing errors can cause fatal hypoglycemic shock. While injections allow precise dose control, oral administration introduces absorption variability driven by meal content, intestinal motility, and gut microbiome status. If patient-to-patient bioavailability variance is large, the same pill could be therapeutic for one patient and dangerous for another. This variability was a core reason for Oramed's ORMD-0801 Phase 3 failure.

- 8-12 year commercialization timeline and massive development costs

From the current mouse stage through large animal testing (primates, pigs), Phase 1-3 human clinical trials, and regulatory approval, at least 8-12 years are expected. Development costs could reach $1-2 billion, with risks of technology acquisition, funding depletion, and regulatory obstacles throughout. There is also the secondary risk that patients hearing pills are coming soon may become less diligent about their current injection therapy.

- Rapidly advancing competing technologies

If oral insulin takes a decade to reach market, next-generation insulin patches, inhaled insulin, automated insulin pump + CGM integrated systems, and stem cell-based beta cell regeneration therapies could preempt the market. As of 2026, miniature pump + continuous glucose monitoring combinations already provide nearly automated insulin management, suggesting that market demand for oral insulin at its eventual launch may be smaller than current projections.

Outlook

In the short term, over the next six months to one year, the Kumamoto University team will embark on validation experiments in large animal models such as pigs or non-human primates. How well the bioavailability holds in a digestive environment more similar to humans will be the first critical gate. The porcine gastrointestinal tract is considered the most human-analogous model in terms of length, pH environment, and gut microbiome composition — if bioavailability above 20% is confirmed here, the substantive basis for clinical entry will be established. If confirmed, a licensing competition among pharmaceutical companies will likely intensify. Novo Nordisk, Eli Lilly, and Sanofi — the insulin Big Three — along with Japanese majors like Takeda and Astellas, are expected to show interest. During this period, Kumamoto University will begin strengthening its patent portfolio and initiating technology transfer negotiations, with the establishment of an early-stage bioventure also a plausible scenario.

The key watchpoints in large animal trials are threefold. First, how well the absolute bioavailability figures hold relative to mouse data. Second, whether the coefficient of variation (CV) of absorption between pre- and post-meal dosing falls within clinically acceptable ranges (typically under 30%). Third, whether long-term safety on the intestinal mucosa is established with repeated dosing. If all three criteria are met, the preclinical package for IND submission will be essentially complete. If any one fails, additional formulation optimization or peptide modifications will be required, potentially delaying the timeline by 1-2 years. Japan's PMDA regulatory pathway is also an important variable — Japan operates a priority review system (SAKIGAKE designation) for innovative drugs, and if DNP technology receives this designation, the development timeline could be shortened significantly.

In the medium term, looking 1-3 years ahead, the platform value of DNP peptide technology will come into sharper focus. If its potential as an oral conversion platform not just for insulin but for GLP-1 receptor agonists (semaglutide, tirzepatide) is validated, the technology's valuation could grow exponentially. Rybelsus, the current oral version of semaglutide, has a bioavailability of only about 1%, requiring high-dose formulations and the inconvenient condition of 30-minute fasting before dosing. If DNP technology can improve this to 10-20%, pill size shrinks, dosing conditions become more flexible, and patient convenience improves dramatically. The GLP-1 agonist market, including the obesity treatment space, is projected to exceed $150 billion by 2030, and if the DNP platform accelerates oral conversion in this market, the potential value reaches tens of billions of dollars.

During this period, competition in the global biotech industry for oral protein therapeutics will also intensify. Companies like Enteral Bio (US) and Enteria (Israel) are advancing their own oral delivery platforms, and sustained R&D investment and patent defense will be essential for DNP technology to maintain its competitive edge. Additionally, by 2027-2028, large pharmaceutical companies like Novo Nordisk and Eli Lilly may be running their own oral insulin programs, making the timing of licensing negotiations critical. Japan's Bio Strategy 2030 also serves as an important backdrop — the Japanese government is actively supporting academic-industry technology transfer to restore global competitiveness in biopharmaceuticals, making it likely that the Kumamoto University research will receive government support.

In the long term, beyond 3-5 years, whether oral insulin enters clinical trials becomes the decisive inflection point. In the bull case scenario, large animal trials proceed smoothly, the preclinical package is completed by 2028, and Phase 1/2a human clinical trials begin around 2029-2030. If Phase 1 confirms safety and pharmacokinetic profiles, and Phase 2a demonstrates initial efficacy in Type 2 diabetes patients, oral insulin could reach the market by 2033-2035. This would fundamentally transform the diabetes treatment paradigm, with 30-50% of the $38 billion global insulin market potentially shifting to oral formulations. That opens a new annual market of $12-19 billion, making it one of the largest market transitions in biopharmaceutical history.

In the base case scenario, bioavailability drops to 15-25% in large animal trials, requiring additional formulation optimization. Peptide sequence modifications, enteric coating optimization, and improved insulin stabilization strategies add 1-2 years, pushing clinical entry back to 2031-2032. Commercialization shifts beyond 2036, but the technology retains its game-changer status. Even in this scenario, the DNP platform's value remains valid, as 15-25% bioavailability still represents a 2-10x improvement over previous oral insulin technologies (2-10%). The key risk in the base case is competitive technology catch-up. Automated insulin pumps and continuous glucose monitoring technology are advancing rapidly, and by the time oral insulin reaches market, insulin delivery automation may already be at a considerable level. In this case, the market size for oral insulin may be smaller than projected, but for patients in developing countries who cannot access automated pump systems, it would still carry revolutionary significance.

In the bear case scenario, inter-individual absorption variability in humans proves too large for safe dose-setting. If meal patterns, gut microbiome diversity, and gastrointestinal conditions push the coefficient of variation above 50%, application to drugs with narrow therapeutic windows like insulin becomes untenable. In this case, the technology would pivot to other protein therapeutics where dose precision is less critical. Growth hormone, parathyroid hormone (PTH), calcitonin, and erythropoietin are first-line candidates, as they have wider therapeutic windows and greater tolerance for absorption variability. Even so, the value of the DNP platform itself would be preserved, as it remains a core technology for the largely untapped oral biologics market.

With the global biopharmaceutical market projected to exceed $600 billion by 2030, even if only 1% of those drugs could be converted to oral delivery, that opens a $6 billion market opportunity. In reality, the potential targets for oral conversion include dozens of drugs — insulin, GLP-1 agonists, growth hormone, PTH, interferons, antibody fragments — and their combined addressable market is estimated at $20-50 billion. One additional dimension worth monitoring is the shift in pharmaceutical value chains. The current insulin market is an oligopoly dominated by Novo Nordisk (34%), Eli Lilly (31%), and Sanofi (18%) controlling 83%. An entirely new oral formulation could crack this oligopoly structure, as the core competitive advantages of injectable insulin — large-scale bio-manufacturing facilities and global cold-chain distribution networks — become less relevant. This could enable biosimilar manufacturers and generic pharmaceutical companies to rapidly enter the oral insulin market, ultimately driving price reductions and expanded access.

Furthermore, oral insulin could create synergies with the digital healthcare ecosystem for diabetes management. When combined with continuous glucose monitoring (CGM) devices and AI-based dose adjustment algorithms, the biggest weakness of oral insulin — absorption variability — could be monitored and compensated for in real time. For example, an AI system that automatically recommends the next dosage based on CGM data becomes feasible, potentially elevating oral delivery safety to levels approaching injection precision.

The key milestones to watch unfold as follows. Large animal trial results expected in the second half of 2026 will constitute the first inflection point. Whether a licensing agreement with a major pharmaceutical company materializes in 2027-2028 will be the second. The submission of an IND in 2029-2030 will be the third inflection point that determines this technology's trajectory. And Phase 2 results around 2031-2033 will serve as the fourth inflection point — if statistically significant blood sugar improvement over placebo and an acceptable safety profile are confirmed, large-scale pharmaceutical investment ($1 billion-plus) will follow. Regardless of which scenario materializes, it is clear that this research has raised the technological baseline for oral protein therapeutics by a meaningful and potentially historic step.

Sources / References

- Small Intestine-Permeable Cyclic Peptide-Based Technology Enables Efficient Oral Delivery — PubMed / Kumamoto University

- Insulin pills may soon replace daily injections — ScienceDaily

- Scientists Achieve Long-Sought Breakthrough Toward Oral Insulin Pills — SciTechDaily

- Oral insulin (ORMD-0801) in type 2 diabetes mellitus: Phase 3 randomized trial — PubMed / Oramed Pharmaceuticals

- Diabetes Drugs Market Size, Share and Growth Report 2026 — Fortune Business Insights

- Insulin pill breakthrough could replace daily diabetes injections — Open Access Government

- IDF Diabetes Atlas - Global Diabetes Statistics — International Diabetes Federation