Is Nvidia a Chip Company or an AI Empire? — The Uncomfortable Question GTC 2026 Is Forcing Us to Ask

Summary

Nvidia GTC 2026 simultaneously reveals the Vera Rubin architecture and NemoClaw agent platform, making it impossible to ignore that Nvidia has evolved far beyond a chip company into an AI infrastructure empire.

Key Points

Vera Rubin NVL72 Overwhelming Specs

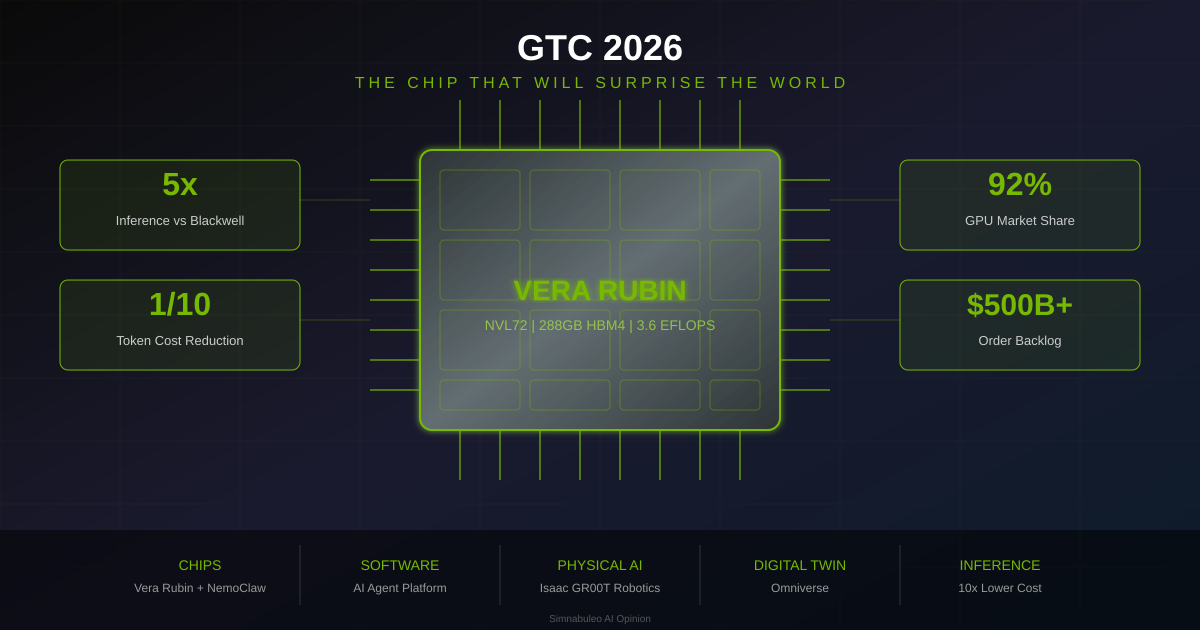

The Vera Rubin NVL72 packs 72 GPUs and 36 CPUs into a single rack, with 288GB HBM4 memory per GPU and 22TB/s bandwidth. It delivers 5x Blackwell inference performance at one-tenth the cost per token. A single rack achieves 3.6 EFLOPS, compressing supercomputer-class compute into one server rack.

NemoClaw — Signal of Software Platform Transformation

Nvidia's open-source AI agent platform NemoClaw is hardware-agnostic, running on AMD and Intel processors too. This mirrors Google's Android and Microsoft's Windows strategy — control the software layer to ultimately pull hardware decisions your way. Salesforce, Cisco, Google, and Adobe are already in partnership discussions.

Double-Edged Ecosystem Lock-in

From CUDA to NeMo, Nemotron, NIM, and now NemoClaw, Nvidia's vertically integrated stack is nearing completion. The lock-in operates at a more fundamental level than Apple's ecosystem. Once developers enter, escaping becomes extraordinarily difficult — a strength for Nvidia but a concern for technological diversity.

Meta's Custom Chip Challenge and Its Limits

Meta unveiled four MTIA chips (300/400/450/500) with plans for new chips every six months, but these are purpose-built for internal inference workloads only. Nvidia delivers a full stack spanning training, inference, agentic AI, and physical AI — an entirely different game in terms of scale and scope.

Physical AI and the AI Infrastructure Empire

Isaac GR00T N1.6, unveiled at GTC 2026 Physical AI Days, is a vision-language-action model integrating language comprehension, visual processing, and physical action for humanoid robots. Combined with autonomous driving, industrial robotics, and Omniverse digital twins, Nvidia aims to dominate both software and physical world AI infrastructure.

AI Infrastructure Investment Acceleration and Scenario Analysis

Vera Rubin deployment will trigger a race among cloud providers to secure Rubin first. Bull case (40%): annual revenue exceeding $400B by 2028, market cap breaching $5T. Base case (45%): market share stabilizing at 80%, revenue around $300B. Bear case (15%): AI bubble burst or geopolitical crisis, share dropping to 65-70%.

Positive & Negative Analysis

Positive Aspects

- AI Democratization Acceleration

Vera Rubin's inference cost dropping to one-tenth of Blackwell's means running large-scale AI models becomes accessible to small and medium enterprises, not just Big Tech. When cost per token falls to roughly one-seventh, enterprise AI service pricing could drop dramatically, fundamentally disrupting the class hierarchy of AI technology.

- Open-Source NemoClaw Security Innovation

NemoClaw embeds multi-layer security and privacy controls directly into the platform core while providing full source code access. Enterprises can inspect and customize the code, overcoming distrust of black-box AI services. Salesforce, Cisco, Google, Adobe, and CrowdStrike are already in partnership discussions.

- Physical AI Era Begins

Isaac GR00T N1.6 vision-language-action model integrates language comprehension, visual processing, and physical action execution for humanoid robots. Combined with autonomous driving, industrial robotics, and Omniverse digital twins, innovation extends beyond software into physical world AI infrastructure.

- AI Infrastructure Investment Virtuous Cycle

A 10x reduction in inference cost per token enables handling 10x more AI workload with the same investment. Per the Jevons Paradox, efficiency improvements drive demand explosions. Data center investment is projected to grow 40% annually between 2025 and 2030, with AWS at $75B and Microsoft at $80B set to increase further.

Concerns

- Monopolistic Market Dominance

A 92% GPU market share is not a healthy competitive ecosystem. Vertical integration of hardware, software, dev tools, and inference services reduces customer bargaining power to near zero. Meta, AWS, Google, and Microsoft are developing custom chips to escape dependency, but closing the performance gap requires considerable time.

- Energy Consumption Crisis

Blackwell NVL72 consumed 120kW per rack; Vera Rubin is likely higher. With AI data centers already accounting for 2-3% of global electricity consumption, more powerful chips intensify pressure on power infrastructure at a critical time.

- Dark Side of Ecosystem Lock-in

Deepening CUDA dependency risks biasing AI development toward Nvidia hardware optimization, stifling technological diversity and constraining innovation. While NemoClaw claims hardware agnosticism, it will likely be best optimized for Nvidia hardware, extending lock-in into the software layer behind an open-source banner.

- Geopolitical Supply Chain Risk

Nvidia's complete manufacturing dependence on TSMC in Taiwan means escalating cross-strait tensions could paralyze global AI infrastructure. Overseas fabs are being built but matching Taiwan's bleeding-edge capabilities takes time. U.S. chip export controls on China also create revenue headwinds.

Outlook

Within this very week, Jensen Huang's keynote at GTC 2026 will reveal the identity of the "chip that will surprise the world." The industry is weighing three main possibilities. First, an early reveal of a next-next-generation data center accelerator. Second, the official announcement of Nvidia's laptop CPUs, the N1 and N1X. Third, an entirely new chip category — for instance, a dedicated accelerator for agentic AI or a processor purpose-built for robotics. Personally, I'm putting my weight on the third possibility. The reasoning is straightforward: Nvidia organized NemoClaw and Physical AI Days as separate tracks specifically because it intends to support agentic AI and physical AI at the hardware level. Huang said he'd "surprise" us, and a simple performance upgrade wouldn't surprise this market. Delivering an entirely new paradigm would.

Once NemoClaw officially launches, the enterprise AI agent market landscape will shift significantly within three to six months. Currently, this market features competition between OpenAI's OpenClaw, Microsoft's Copilot, and Google's Gemini agents, and NemoClaw's open-source nature gives it a differentiated position. I expect adoption rates to climb quickly in finance, healthcare, and defense — sectors hypersensitive to security and privacy. With the agentic AI market projected to reach $28 billion by 2027, NemoClaw has a realistic shot at capturing a substantial portion of that pie. The key variable is whether existing enterprise software powerhouses like Salesforce and Cisco join as partners. If they begin integrating NemoClaw into their own platforms, enterprise proliferation could be explosive.

The most immediate short-term impact will be the acceleration of AI infrastructure investment. As Vera Rubin NVL72 begins deploying to major cloud providers in the second half of 2026, an investment race to "secure Rubin first" will erupt. AWS invested $75 billion in data centers in 2025 alone; Microsoft committed $80 billion. Vera Rubin's arrival will only push these figures higher. A 10x reduction in inference cost per token means the same investment handles 10 times more AI workload, triggering simultaneous AI service price drops and demand explosions.

Looking at the medium term of six months to two years, the competitive landscape of the AI chip market will undergo serious restructuring. Meta's MTIA series promises a new chip every six months, but Nvidia is moving at the same pace. The difference is scale and scope. Meta's chips serve its own data centers internally; Nvidia supplies every enterprise on the planet. AMD's MI300 series shows competitive price-performance in some areas, but the software ecosystem gap remains vast. ROCm closing the gap with CUDA faces an overwhelming developer community size disadvantage. Intel's Gaudi series has effectively exited the race. The medium-term outlook: Nvidia will maintain market dominance above 80%.

Another critical medium-term shift is the software platform war going into full swing. NemoClaw's launch is Nvidia's declaration that it will add software revenue on top of chip revenue. Nvidia's software annual recurring revenue (ARR) hasn't been officially disclosed, but industry estimates peg it around $2 billion and growing rapidly. If NemoClaw succeeds, this software revenue could surpass $10 billion by 2027. This would transform Nvidia's revenue structure from "hardware-dependent" to a "hardware + software hybrid."

In the long-term view of two to five years, we must consider the possibility that the AI infrastructure paradigm itself changes. If Nvidia's forecast holds and data center investment grows to $3-4 trillion annually by 2030, that's five to six times the current size of the entire global semiconductor industry. Most of that investment will flow into AI training and inference infrastructure, and if Nvidia maintains its current position, it could become a mega-corporation with annual revenue exceeding $500 billion. But if quantum computing commercializes faster than expected or neuromorphic chips demonstrate GPU-beating performance, Nvidia's position could crumble sooner than anticipated.

A more realistic long-term threat is geopolitical. Nvidia's complete manufacturing dependence on TSMC means escalating tensions across the Taiwan Strait could paralyze global AI infrastructure. Scenarios combined: Bull case (40%) — AI investment cycle holds through 2030, annual revenue surpasses $400B, market cap breaches $5T. Base case (45%) — growth moderates, share at 80%, revenue around $300B. Bear case (15%) — AI bubble bursts or geopolitical crisis, share drops to 65-70%. The Jevons Paradox applied to AI infrastructure suggests efficiency improvements will drive demand explosions rather than reductions.

Sources / References

- NVIDIA GTC 2026: Live Updates on What's Next in AI — NVIDIA Blog

- Jensen Huang Promised to Surprise the World: GTC Starts Monday — Let's Data Science

- NVIDIA GTC 2026: Jensen Huang promises a chip reveal meant to surprise the world — VideoCardz

- Inside the NVIDIA Vera Rubin Platform: Six New Chips, One AI Supercomputer — NVIDIA Developer Blog

- Nvidia plans open-source AI agent platform NemoClaw — CNBC

- Meta reveals custom AI chips it says beat Nvidia — The Register

- Nvidia reports earnings and guidance beat as AI boom pushes data center revenue up 75% — CNBC

- NVIDIA Controls 92% of the GPU Market — Carbon Credits