Earth Has Been a Hydrogen Factory for a Billion Years — Nobody Noticed

Summary

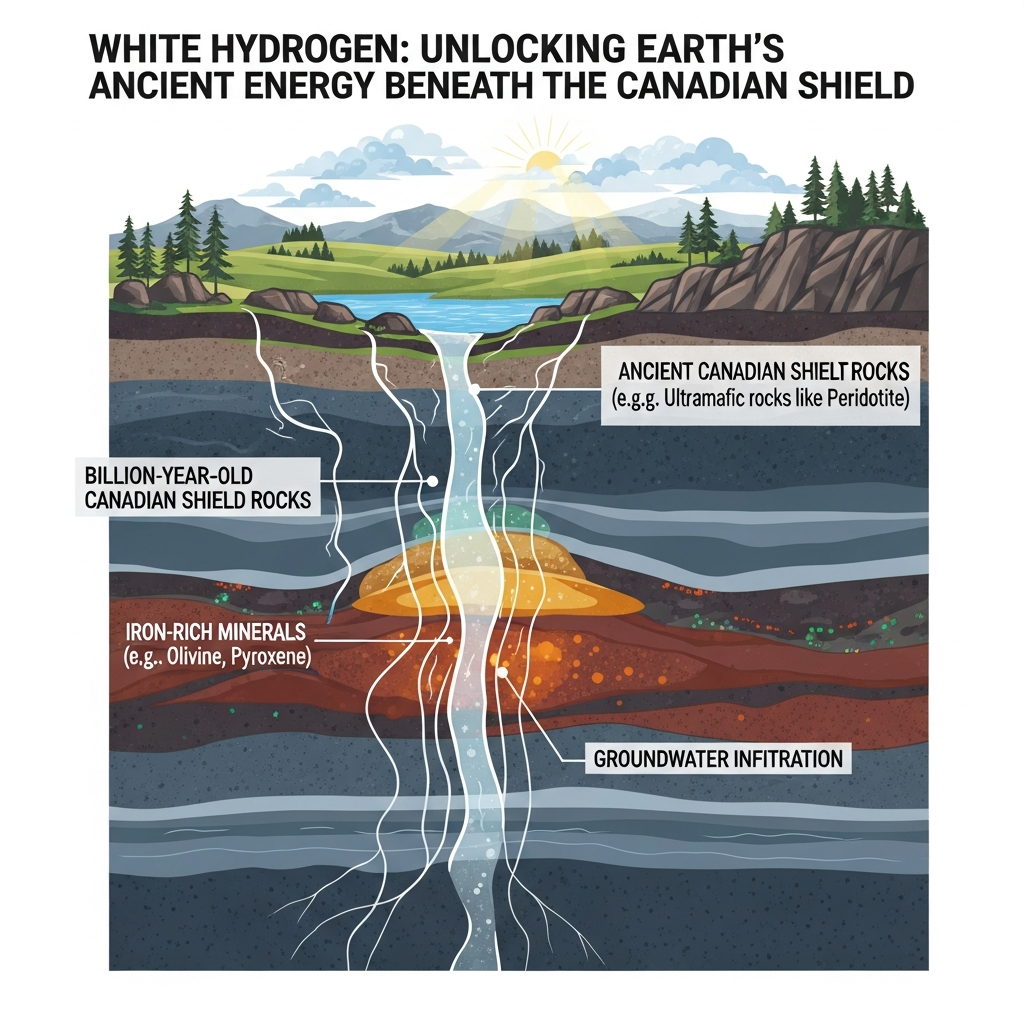

A PNAS study published in May 2026 by researchers at the University of Toronto and University of Ottawa confirmed continuous white hydrogen emissions from billion-year-old Precambrian rocks in the Canadian Shield, establishing a critical milestone in geologic hydrogen research. Systematic analysis of approximately 15,000 existing mine boreholes revealed annual emissions exceeding 140 tonnes of naturally occurring hydrogen, produced through serpentinization reactions in which iron-rich olivine reacts with water at temperatures of 200–350°C to generate hydrogen gas with zero carbon emissions. USGS estimates global underground hydrogen reserves at between 1 billion and 10 trillion tonnes — a range spanning four orders of magnitude that reflects fundamental uncertainty in current geological mapping capabilities and simultaneously suggests immense long-term potential alongside real limitations in what science can confidently assert today. White hydrogen's geographic distribution, concentrated in ancient craton formations across Canada, Australia, Siberia, and West Africa, carries profound geopolitical implications that could reshape global energy hierarchies away from traditional fossil fuel producers and toward countries with ancient geological foundations. Commercialization faces substantial barriers including low extraction concentrations, absence of proven extraction technology at industrial scale, and unresolved questions about recharge rates, yet early evidence from Mali's Bourakébougou site suggests production costs potentially below $1/kg — a figure that, if broadly replicable, would make white hydrogen the cheapest clean hydrogen source by a considerable margin.

Key Points

Billion-year-old Canadian Shield rocks confirmed emitting hydrogen by direct field measurement for the first time

The joint study by the University of Toronto and University of Ottawa represents a pivotal turning point in geologic hydrogen research — not because it speculated about what might exist underground, but because it directly measured what is already escaping into the atmosphere. Using systematic analysis of approximately 15,000 existing mine boreholes in Ontario's Canadian Shield, the team confirmed continuous hydrogen emissions at a rate exceeding 140 tonnes per year from rocks that are over one billion years old, marking the first rigorous field confirmation of this mechanism in the Canadian Precambrian basement. This hydrogen originates from a process called serpentinization: iron-rich minerals like olivine, found deep in Precambrian formations, react with groundwater at temperatures between 200 and 350°C, releasing hydrogen gas as a byproduct while the olivine gradually transforms into serpentine mineral. The energy equivalent of these emissions is approximately 4.7 million kilowatt-hours annually — enough to power around 400 households for a full year — a figure that, while modest in industrial terms, carries profound scientific significance as direct proof that Earth manufactures clean hydrogen continuously through natural geochemical processes. What makes this research particularly methodologically innovative is that the team required no new drilling: all measurements came from pre-existing infrastructure left behind by decades of mining activity, demonstrating that resource discovery can emerge from reinterpreting data we already hold rather than physically expanding into new territory. The paper's publication in PNAS in May 2026 immediately triggered interest from geological survey agencies worldwide, with researchers in Australia, France, and Siberia announcing plans to apply the same borehole reanalysis approach to their own ancient craton formations. The Canadian Shield study is not merely a local geological finding — it is a methodological blueprint for a global search that is now officially underway and that will define the pace of white hydrogen science for years to come.

USGS estimates underground hydrogen reserves at 1 billion to 10 trillion tonnes, with a 10,000-fold uncertainty range

The United States Geological Survey has published an estimate suggesting that between 1 billion and 10 trillion tonnes of naturally occurring hydrogen may reside underground globally — a figure whose upper bound represents approximately 100,000 years of current annual global hydrogen consumption of roughly 100 million tonnes per year. Even the lower bound of 1 billion tonnes represents a decade of global supply, which is substantial by any conventional resource accounting standard and explains why this estimate has generated significant attention across both the scientific and investment communities. However, the critical context that must accompany this number is the astonishing width of the uncertainty range: the difference between 1 billion and 10 trillion tonnes is a factor of 10,000 — and that's not statistical noise or measurement error, it reflects the fundamental reality that geologic hydrogen does not pool into convenient reservoirs the way petroleum does, but disperses across vast rock formations at varying concentrations that are exceptionally difficult to map with existing technology. The scientific community's honest way of expressing "we don't fully understand this resource yet" is to report a range this wide, and treating the upper bound as a planning assumption would be exactly the kind of analytical error that produces investment cycles followed by painful corrections. For the estimate to narrow to something actionable for policy or commercial planning, systematic field measurements like the Canadian Shield study need to be conducted across dozens of major craton formations worldwide — a process measured in years, not months. The USGS number is legitimately exciting and scientifically grounded; the discipline required to treat it as a hypothesis to be tested rather than a resource confirmed is the difference between intelligent engagement with white hydrogen and speculative excess.

White hydrogen commercialization would completely redraw global energy geopolitics

If white hydrogen extraction becomes economically viable at industrial scale, the geopolitical consequences would reach far beyond the energy sector — they would fundamentally alter which countries hold strategic leverage in the 21st-century energy order, in ways that cut across every existing assumption about the clean energy transition. The current renewable energy transition concentrates geographic advantages in nations with abundant sunlight or long coastlines at favorable latitudes, while fossil fuel wealth has historically accrued to regions with conventional hydrocarbon geology in the Middle East, Russia, and North America. White hydrogen breaks both patterns entirely: its geological occurrence correlates with ancient cratons and ophiolite formations distributed very differently from either conventional energy resources or renewable energy potential zones. Canada's Shield, Russia's Siberian Craton, Australia's Yilgarn Craton, and West Africa's craton belt are the geological winners in a white hydrogen world — regions currently peripheral in energy geopolitics that would become strategically pivotal if the resource can be tapped at commercial scale. The most striking implication is for Africa: much of the continent overlies ancient cratonic geology, and if high-concentration hydrogen hotspots analogous to Mali's Bourakébougou are discovered broadly across sub-Saharan Africa, the continent's relationship with global energy markets could shift from historical dependency toward genuine leverage. This is not a story about one country's energy portfolio adjustment; it is about rewriting the rules of energy geopolitics in ways that nobody anticipated when the renewable energy transition began, forcing recalibration across Gulf states, European energy import strategies, and China's Belt and Road energy infrastructure investments simultaneously.

Oil majors are paradoxically positioned to become white hydrogen's biggest beneficiaries

There is a structural irony embedded in the white hydrogen story that deserves direct confrontation rather than diplomatic circumvention: the companies best positioned to dominate white hydrogen commercialization are the same fossil fuel giants that have spent decades as primary targets of climate advocacy and decarbonization policy. TotalEnergies has already secured exploration licenses in France's Lorraine region for geologic hydrogen; Shell and BP have begun investing in related research. The reason is straightforward and uncomfortable: white hydrogen extraction requires exactly the competencies these companies have built over decades — precision drilling technology, subsurface geological mapping and modeling, pipeline infrastructure, and the financial and organizational capacity to manage large-scale projects in geographically remote environments at commercial timelines. Smaller startups and academic teams can pioneer the science and the early pilot demonstrations, but when the commercialization phase demands scaling from hundreds of kilograms to millions of tonnes, the majors hold structural advantages that are extraordinarily difficult for new entrants to overcome. The shale gas revolution offers an instructive parallel: independent operators led initial exploration and technology development, but as the industry matured, major oil companies acquired the most productive assets and consolidated market position through acquisition rather than innovation. I expect white hydrogen to follow a similar arc — discovery and early development by independents, consolidation by majors — unless deliberate policy design actively creates pathways for new entrants to remain competitive at scale. The moral dimension deserves naming: companies that lobbied against climate legislation becoming primary beneficiaries of the clean hydrogen age is not coincidental, it is a structural consequence of how capital, infrastructure, and expertise compound in favor of incumbents across technological paradigm shifts.

Reanalyzing existing borehole data is as methodologically revolutionary as the white hydrogen discovery itself

The deepest contribution of the Canadian Shield study may ultimately be recognized not as what it found, but as how it found it. Rather than proposing expensive new drilling campaigns, the research team systematically reanalyzed data from approximately 15,000 boreholes that were already drilled during decades of mining activity — extracting entirely new resource intelligence from infrastructure that was built and data that was collected for entirely different purposes. This "recycled discovery" methodology has immediate global applicability: Natural Resources Canada maintains databases of hundreds of thousands of borehole records, the U.S. Department of Energy's National Energy Technology Laboratory holds similarly vast archives of subsurface data, and Geoscience Australia has systematically catalogued underground measurements across the country's ancient craton regions for decades. If machine learning and geochemical pattern recognition algorithms are applied systematically to these existing datasets, the number of confirmed white hydrogen emission sites could multiply dramatically within a few years, at a fraction of the cost of traditional exploration programs. The implications extend beyond white hydrogen itself: the same methodological approach could identify previously unrecognized geothermal gradients, subsurface microbial ecosystems, rare earth element concentrations, and other resources that escaped notice when data was originally collected for different scientific questions. In the history of science, some of the most consequential discoveries have come not from finding new phenomena, but from reinterpreting data that was already known with new analytical frameworks. The age of computational geoscience — using machine learning to surface patterns invisible to human analysts working through physical records manually — is arriving precisely as global demand for clean energy intelligence reaches a historic peak. The Canadian Shield study is early proof that this combination of historical data and modern analytical tools can yield discoveries of genuine scientific and commercial consequence.

Positive & Negative Analysis

Positive Aspects

- Genuinely zero-carbon at the production stage, with natural carbon sequestration as a bonus

White hydrogen stands apart from every other hydrogen type in the current energy taxonomy because it produces no carbon emissions at the source — not merely "low-carbon," but structurally zero-emission by nature of its geological origin. Green hydrogen is theoretically clean, but the electricity powering electrolysis is rarely 100% renewable in practice; when grid electricity is used, indirect carbon emissions from fossil-fueled power generation get embedded in the final product's lifecycle footprint. Blue hydrogen captures carbon during natural gas reforming but cannot achieve true zero-emission status because real-world carbon capture efficiency tops out well below 100%. White hydrogen requires no manufacturing energy input whatsoever — it is a byproduct of a natural geochemical reaction that has been running for millions of years with no human involvement. What makes this even more remarkable is that serpentinization doesn't just produce hydrogen; it also mineralizes atmospheric CO2 as part of the same reaction process, effectively combining hydrogen production with natural carbon sequestration in a single geological event. This is functionally equivalent to a carbon capture and storage system that operates without human energy input, at geological scale, continuously, and as a side effect of producing useful fuel. For nations designing net-zero roadmaps, a hydrogen source that simultaneously reduces atmospheric carbon while providing clean fuel is not an incremental improvement — it is qualitatively different from anything currently in the clean energy toolkit. Early cost estimates from Mali's Bourakébougou operation suggest production costs potentially below $1 per kilogram, compared to $4–6/kg for green hydrogen, which means white hydrogen may eventually deliver the cleanest emissions profile at the lowest production cost — a combination that no existing hydrogen production method can currently approach.

- Existing infrastructure dramatically lowers initial capital requirements for exploration and early extraction

One of the largest barriers to new energy resource development is the capital expenditure required to build infrastructure from scratch — and white hydrogen's relationship with existing infrastructure is unusually favorable compared to every clean energy alternative currently in development. The PNAS study demonstrated the principle directly: 15,000 pre-existing mine boreholes provided all the measurement infrastructure needed to identify and quantify white hydrogen emissions without any new drilling activity. Globally, millions of abandoned and active boreholes already penetrate the depths where serpentinization occurs, and many of these retain associated monitoring equipment, wellhead infrastructure, and access roads that can be repurposed rather than newly constructed. Industry estimates suggest initial capital expenditure for white hydrogen exploration could be 30–50% lower than equivalent green hydrogen facility construction, which requires a complete package of electrolyzer equipment, dedicated renewable power generation, water treatment systems, and storage infrastructure built from nothing. The petroleum industry's parallel investment in drilling technology, subsurface monitoring systems, and pipeline networks represents not just competitive positioning but genuinely complementary infrastructure that white hydrogen extraction could directly utilize rather than duplicate. This reuse economy dimension is particularly meaningful for regions where mining industries have declined — communities in northern Ontario, the Australian Outback, and former industrial regions of West Africa where infrastructure from a previous resource era could anchor an entirely new energy sector without requiring a full greenfield buildout. The capital efficiency argument is one of white hydrogen's most compelling commercial cases precisely because it narrows the financing gap between pilot demonstration and first meaningful commercial production.

- Genuine potential to address energy access inequality in historically underserved regions

The geographic distribution of white hydrogen resources maps onto regions that have been underserved by both conventional energy infrastructure and the first wave of renewable energy investment — and that alignment is one of the discovery's most socially significant features. Sub-Saharan Africa, large portions of which overlie ancient craton formations, has an electricity access rate of roughly 48%, meaning more than half a billion people live without reliable electricity supply despite being located on some of the oldest and most geochemically active geology on Earth. Mali's Bourakébougou has been producing over 90% pure natural hydrogen from a single artesian well since 1987, already powering a local microgrid that serves the surrounding village community. If high-concentration hydrogen hotspots are identified broadly across the African craton belt, the implications for decentralized energy access could be transformative in a way that neither centralized grid expansion nor utility-scale solar has yet achieved. Rather than waiting decades for centralized grid infrastructure to reach remote communities, distributed white hydrogen generation could allow villages and small towns to achieve genuine energy self-sufficiency using a resource literally beneath their feet — requiring no imported fuel, no grid connection, and no large capital investment in generation equipment. The same logic applies to Indigenous communities in northern Canada, rural settlements in the Australian interior, and remote regions of South America where ancient basement geology has barely been surveyed. White hydrogen's craton distribution offers a rare case where geological luck may align with communities historically excluded from energy abundance — a form of structural equity that conventional clean energy transitions have not reliably delivered.

- New research momentum and career pathways revitalizing the geoscience field

The white hydrogen exploration wave is generating a genuine renaissance in geoscience disciplines that had been narrowing toward petroleum-focused applications for decades, with the intellectual territory opening up in multiple directions simultaneously. Exploration projects have launched across France's Lorraine region, Spain's Aragon, Australia's South Australia, the U.S. state of Kansas, and Brazil's São Francisco Basin — and each project is creating demand for geological, geochemical, and hydrological expertise that had been in structural decline as traditional oil industry employment contracted. The intellectual frontier is genuinely stimulating: questions about deep-earth chemistry, subsurface fluid dynamics, rock-water interaction kinetics, and hydrogen transport through geological formations at varying temperatures and pressures are now high-priority research topics attracting graduate students and postdoctoral researchers who might otherwise have left the field. The methodological bridge between traditional field geology and modern data science is also generating a new hybrid discipline — computational geoscience — that combines machine learning with subsurface geochemical analysis in ways that weren't feasible a decade ago, opening career paths that are intellectually rich and practically relevant. University earth science departments are adding geological hydrogen exploration to their curriculum alongside traditional petroleum geology, and professional geoscience organizations are establishing new certification tracks to meet industry demand. For early-career geoscientists uncertain about prospects outside the shrinking conventional oil and gas sector, white hydrogen research offers an exciting alternative that authentically combines field work, laboratory chemistry, data analysis, and real-world energy applications with meaningful implications.

- Revolutionary cost potential compared to all existing clean hydrogen production methods

White hydrogen's economic case, if technical challenges are solved, is compelling by any standard of comparison to existing clean hydrogen production methods and represents a potential step-change rather than incremental improvement. The current cost landscape for clean hydrogen is stark: green hydrogen runs $4–6 per kilogram under current technology and scale conditions, while blue hydrogen with carbon capture lands at $1.5–3/kg, and even gray hydrogen from natural gas without carbon capture costs roughly $1–2/kg. Early analysis of Mali's Bourakébougou operation generated preliminary estimates suggesting white hydrogen extraction could potentially achieve production costs below $1/kg at favorable geological sites — a figure that would make it not merely competitive with but substantially cheaper than any existing clean hydrogen production pathway. The cost advantage derives from the fundamental resource structure: there is no electrolyzer to power, no natural gas feedstock to purchase, no carbon capture system to maintain, no steam methane reforming equipment to service. The input cost for the chemical reaction itself is effectively zero; real costs are drilling, borehole maintenance, gas compression, purification, and transport. If this cost structure is replicable beyond exceptional hotspots like Bourakébougou and into broader geological white hydrogen resource categories, it would remove what has been the single largest obstacle to hydrogen economy adoption: the price differential between clean hydrogen and conventional fossil fuel alternatives that has made hydrogen industrial applications economically marginal for decades. A broadly available hydrogen source below $1/kg would not just compete with green hydrogen — it would dramatically improve the economics of hydrogen fuel cell transportation, hydrogen-based steel and fertilizer production, and power generation applications that have remained carbon-intensive because clean alternatives were too expensive to adopt at scale.

Concerns

- Concentration and scale limitations remain fundamentally unresolved engineering challenges

The 140-tonne annual figure that headlines this discovery is genuinely meaningful from a scientific standpoint, but industrial contextualization is a sobering exercise that must accompany any discussion of commercial potential. World hydrogen consumption runs at approximately 100 million tonnes per year; 140 tonnes represents 0.00014% of global demand — a figure so small that it underlines how far this resource sits from commercial significance at present scale. More fundamentally, white hydrogen doesn't behave like petroleum: oil accumulates in high-concentration reservoir structures where a single production well can yield thousands of barrels per day, but white hydrogen disperses across vast rock formations at low concentrations, requiring collection from large surface areas to aggregate meaningful quantities, and no proven technology exists to do this economically. Developing the gas gathering, compression, and pipeline infrastructure needed to economically handle such diffuse low-concentration emissions will require years of engineering development that may or may not produce results competitive with existing production methods. The analogy to gold dissolved in seawater is instructive: oceanographers have known for decades that every cubic kilometer of seawater contains roughly 13 milligrams of dissolved gold, and total oceanic gold vastly exceeds all gold ever mined in human history, but the energy cost of extracting it from solution renders the exercise economically impossible in practice. White hydrogen's existence underground is now confirmed; the pathway from confirmed existence to economical extraction at industrial concentration remains technically uncharted and represents the central challenge that all commercial development must ultimately solve before this resource category can claim significance in global energy accounting.

- Hype cycle dynamics pose serious risks to legitimate research programs and responsible investment

The energy industry's institutional memory includes a long catalog of technologies heralded as civilization-altering breakthroughs before stalling far short of commercial deployment, and white hydrogen's early reception is already showing several recognizable warning signs of premature hype cycle inflation. Nuclear fusion, methane hydrates, algal biofuel, wave energy conversion, and enhanced geothermal systems all generated substantial investor and media enthusiasm before encountering commercialization barriers that their early champions underestimated. Gartner's hype cycle pattern of peak expectations followed by the trough of disillusionment is particularly virulent in energy technology, partly because the capital cycles are long, the engineering challenges are systematically underestimated in early research phases, and the gap between laboratory results and industrial deployment is almost always wider than initial projections suggest. In Australia and France, junior mining and exploration companies are already acquiring craton exploration licenses based on minimal geological due diligence, citing USGS upper-bound reserve estimates in promotional materials as though they represent confirmed accessible resources rather than speculative geological modeling. When hype-driven capital floods into an emerging sector before technical fundamentals justify it, the inevitable disappointment doesn't just punish speculators — it contaminates funding conditions for well-grounded research programs, causes regulators to impose blanket restrictions rather than targeted oversight, and sets back legitimate technical progress by years or even decades at exactly the moment when the science is genuinely advancing. Protecting white hydrogen from its own hype is as important as advancing the underlying technology.

- Environmental risks at commercial extraction scale remain almost entirely unstudied

The "clean energy" label attached to white hydrogen has appropriately dominated early coverage of the geological and economic aspects, but it embeds an assumption that large-scale extraction would be environmentally benign — an assumption that has not been empirically tested and that historical parallels suggest should be examined rigorously before, not after, commercial deployment begins. Extracting large volumes of hydrogen from subsurface formations could alter groundwater flow patterns, disrupt subsurface microbial ecosystems that have evolved over millions of years, and disturb the chemical equilibria that drive serpentinization in ways that are difficult to model and potentially impossible to reverse. If stimulated serpentinization — artificially injecting water into rock formations to accelerate hydrogen production — becomes a commercial technique, the potential for induced seismicity and groundwater contamination deserves serious pre-deployment evaluation given the documented parallel history of hydraulic fracturing, which generated over 900 human-induced earthquakes in a single year in Oklahoma at peak activity. There is also a scientifically real but underreported concern about hydrogen's indirect atmospheric effects: hydrogen escaping during extraction and transport reacts with hydroxyl radicals, extending the atmospheric lifetime of methane and indirectly amplifying greenhouse warming at a rate estimated at 11 times methane's direct warming potential per kilogram over 100 years. Without reliable measurements of leakage rates during white hydrogen extraction at operating scale, the net climate benefit of this resource cannot be confirmed through any lifecycle accounting method currently available. "Clean energy" must describe a full lifecycle outcome, not a marketing claim derived solely from the absence of combustion emissions during production.

- Hydrogen transport infrastructure is absent and prohibitively expensive to build at necessary scale

Even under the optimistic scenario where white hydrogen extraction becomes technically feasible and economically competitive at multiple geological sites worldwide, the logistics of moving it from geological source to end-use application represent a separate and substantial challenge that is consistently underweighted in early-stage commercial analyses. Hydrogen's molecular properties create unique and significant transportation challenges: its extremely small molecular size enables it to permeate and embrittle conventional metal alloys through hydrogen embrittlement, making existing natural gas pipeline networks largely unsuitable for dedicated hydrogen service without costly retrofitting or complete reconstruction using hydrogen-compatible materials. Dedicated hydrogen pipelines are technically proven but require specialized materials, engineering standards, and weld quality controls that add approximately 20–40% to equivalent conventional pipeline construction costs. Alternative transport approaches — converting hydrogen to ammonia or liquid organic hydrogen carriers (LOHC) for shipping, then reconverting at the destination — add energy conversion losses of 20–40% at each transformation step, substantially eroding the cost advantage that makes white hydrogen economically attractive in the first place. The IEA has estimated that global hydrogen infrastructure buildout will require minimum investment of $1.7 trillion by 2040 — applying to the hydrogen economy as a whole, not white hydrogen specifically, but illustrating the scale of the shared problem. White hydrogen's most geologically abundant occurrences are likely concentrated in remote craton regions far from population centers and industrial demand, making the last-mile distribution challenge particularly acute and the infrastructure investment requirement disproportionately large relative to the initial resource value that pilots can demonstrate.

- Recharge rates are unproven, meaning white hydrogen could function as a finite rather than renewable resource

The optimistic framing of white hydrogen as a "renewable" energy source rests on the assumption that serpentinization reactions continuously replenish underground hydrogen at rates that make extraction sustainable over human economic timescales — functioning analogously to solar radiation or wind patterns as an inexhaustible natural energy flux. This assumption has not been validated by any long-term production data from sites operating at meaningful extraction rates, and the geological physics of the situation warrant genuine caution about the analogy. Serpentinization reactions operate at geological timescales spanning millions to hundreds of millions of years, while human economic extraction timescales run decades to centuries — and if extraction rates exceed recharge rates at any significant fraction of what would be needed for commercial scale, white hydrogen behaves not as a renewable resource but as a very slowly replenishing finite one. There is also a less obvious but physically plausible risk: intensive extraction could disrupt subsurface pressure gradients, groundwater availability, and temperature conditions that enable serpentinization, potentially reducing or halting natural hydrogen production in a given formation through a feedback mechanism that proves difficult or impossible to reverse. The harvest paradox — where extraction of a naturally occurring process disrupts the conditions sustaining it — is a documented pattern in ecological resource management, and there is no fundamental reason that geological systems are categorically immune to analogous dynamics. Treating a potentially finite resource as genuinely renewable would be repeating, in a different geological register, the same analytical failure that defined the fossil fuel era. Long-term recharge rate monitoring under real extraction conditions should be a non-negotiable prerequisite for commercial-scale deployment, not a research afterthought.

Outlook

The next six months will almost certainly see a wave of follow-up studies targeting other ancient craton formations worldwide. The methodology demonstrated by the Toronto-Ottawa team — systematic reanalysis of existing borehole data rather than new drilling programs — is immediately replicable at minimal cost, which means geological survey agencies sitting on decades of accumulated mine monitoring records now have both the scientific framework and the institutional motivation to apply it. I expect at least three to five new white hydrogen emission studies to emerge within the next six months, focusing on the Siberian Craton, West African Craton, and Australia's Yilgarn Craton specifically. Australia's government has been proactive: South Australia's Gold Hydrogen startup has been conducting test drilling since 2023, and the federal clean energy policy framework makes accelerated white hydrogen funding a natural political move in direct response to the PNAS findings. Canada's Natural Resources department is also likely to announce increased craton hydrogen survey budgets as a direct policy response to the domestic significance of the discovery.

The near-term period carries an equally important warning alongside its scientific promise: speculative capital is already circulating in the white hydrogen investment space, and the dynamics are recognizable. Junior exploration companies are acquiring craton licenses and citing USGS upper-bound reserve figures in promotional materials as though confirmed reserves had been mapped. Australia's ASX has reportedly seen share price jumps for companies that added "hydrogen" to their corporate names without substantive operational changes — a behavioral pattern that should immediately trigger caution among investors who remember the clean energy hype cycles of the early 2010s. I believe the next six months will function as a critical test of whether scientific standards and regulatory disclosure requirements can maintain appropriate guardrails against the white hydrogen story becoming another short-cycle retail investor trap that discredits the underlying technology before it has a genuine chance to develop.

Over the medium term — roughly 18 months to two years out — the most consequential single variable will be whether stimulated serpentinization technology achieves any meaningful commercial milestone at pilot scale. The fundamental commercial constraint on white hydrogen is that natural emission concentrations are insufficient for economical collection at most geological sites outside of exceptional hotspots like Bourakébougou. Stimulated serpentinization — artificially injecting water into iron-rich rock formations to accelerate hydrogen production reactions — is the most promising technical pathway to unlocking the broader geological resource base. France's CNRS and the U.S. Department of Energy are both committing funding to this approach. I anticipate that at least two to three pilot-scale stimulated serpentinization field tests will be initiated within 18 months across different geological settings. If any of those pilots achieves sustained production costs below $2/kg at scale, it would represent a genuine commercial inflection point that would accelerate white hydrogen deployment timelines significantly. If they produce unacceptable environmental side effects — particularly induced seismicity or groundwater impact — the investment narrative will cool rapidly and the field will retreat into a longer period of fundamental research before any commercial revival is plausible.

The geopolitical reconfiguration that white hydrogen enables will begin showing early signals during this same medium-term window, even before commercial production begins at any meaningful scale. Canada will integrate Shield hydrogen potential into national energy strategy documents. Australia will accelerate exploration licensing in Queensland and South Australia, driven by both the commercial opportunity and the geopolitical framing of competing with Canada for early-mover positioning. The most geopolitically significant developments will likely come from Africa: Mali's demonstrated operational hotspot gives West Africa a credible claim to being the white hydrogen analog of the Middle East in conventional petroleum terms, and the African Union and individual member states are likely to begin asserting resource sovereignty frameworks over craton hydrogen rights before international exploration companies move in at scale. I predict that at minimum one formal bilateral white hydrogen exploration or resource-sharing agreement between nations will be signed within two years, establishing international legal precedents for how this resource category is governed. The oil majors will become increasingly visible actors during this window, with TotalEnergies expanding beyond Lorraine and at least one significant acquisition of a white hydrogen exploration startup by a major seeking early-mover positioning in the emerging sector.

Looking out to the five-year horizon, white hydrogen's role in the global energy system will be determined by whether it can solve the production-cost-and-transport problem at sufficient scale to matter. Production cost needs to consistently beat green hydrogen's current $4–6/kg threshold across geological conditions beyond Mali's exceptional natural hotspot — and the IEA's $1.7 trillion estimate for global hydrogen infrastructure investment by 2040 underscores that the transport challenge is real and expensive regardless of how competitive production costs become. My specific five-year forecast: global white hydrogen production reaches 100,000–500,000 tonnes annually by 2031, remaining 0.1–0.5% of total global hydrogen consumption at a rounding-error scale globally, but representing 5–15% of local energy supply in specific regions such as Ontario, South Australia, and West Africa where geological conditions are favorable. The economic and employment benefits will be geographically concentrated in craton-adjacent communities — a form of geological luck that will matter enormously at the regional level even while the global aggregate remains modest.

The longest-range implication is a potential paradigm shift in how clean energy is conceptually organized. The renewable energy transition has been defined by manufacturing — you build solar panels and wind turbines to convert ambient energy flows into electricity. White hydrogen would reintroduce geological extraction alongside manufacturing — you access a resource that accumulated through natural processes over geological time. If both paradigms operate simultaneously in the energy economy, policy frameworks, subsidy structures, investment models, and geopolitical calculations all become more complex in ways that current clean energy governance is not fully prepared to handle. Does extraction-based white hydrogen qualify as renewable under existing energy accounting frameworks if its recharge rate is uncertain? Should it receive the same regulatory treatment and carbon pricing signals as manufactured clean hydrogen? These definitional questions will become live policy debates within the next three to five years. My assessment is that coexistence of the manufacturing and extraction paradigms will ultimately increase energy system resilience by reducing over-dependence on any single technology class and by providing genuinely different options across different geographic and geological contexts. White hydrogen baseload in craton regions buffering the intermittency of solar and wind in the same grid areas is a hybrid model with real technical merit — and one that the current renewable transition planning framework is largely not equipped to optimize for.

Three scenarios bracket the realistic outcome range through 2031. In the bull case — probability 25% — stimulated serpentinization achieves commercial success by 2028 with costs consistently below $1.50/kg, a recognizable "white hydrogen belt" forms across Canada, Australia, and Mali, and the technology claims 3–5% of global hydrogen market share by 2031. At least two oil majors formally restructure white hydrogen as a core business unit rather than a research initiative, and observable early signals of energy geopolitical reconfiguration emerge. In the base case — probability 50% — technical progress is slower than hoped, meaningful commercial extraction doesn't begin until 2029–2030, costs stabilize at $2–3/kg competitive with but not dominant over green hydrogen, and white hydrogen functions as a niche regional resource covering 50,000–100,000 tonnes globally by 2031 — significant locally, invisible in global aggregates. In the bear case — probability 25% — serious environmental complications emerge from early stimulated serpentinization pilots, or multiple high-priority craton surveys return insufficient concentration data, triggering withdrawal of speculative investment and leaving the field in a funding drought from which recovery takes several years. White hydrogen joins the list of technologies that remain perpetually "ten to fifteen years from commercial deployment," and most junior exploration companies that formed during the 2026–2027 enthusiasm wave cease operations.

My honest final caveat: the scenario that most fundamentally invalidates the entire optimistic framework is not technical failure in stimulated serpentinization, but resource classification failure — if extended monitoring of active extraction sites reveals that hydrogen recharge rates fall far below extraction rates at any commercially relevant scale, then the "renewable" framing collapses entirely. A resource that one generation exhausts at commercial scale is not a clean energy transition tool — it is a differently labeled version of the same finite resource problem that the transition is trying to solve. That determination requires longitudinal data that will not exist for at least three to five years of monitored commercial-scale extraction. For practical decision-making: this space absolutely warrants close attention and scientific investment. It does not yet warrant large capital commitments by investors without the risk tolerance and time horizon of early-stage resource development. Earth has been patient for a billion years; waiting three more for adequate evidence is not missing the boat. It is being thoughtful enough to make sure there actually is a boat before boarding it.

Sources / References

- ScienceDaily — White hydrogen found in billion-year-old Canadian rock — ScienceDaily

- Phys.org — White hydrogen: Billion-year-old Canadian Shield rocks — Phys.org

- EurekAlert — University of Toronto and University of Ottawa Research Team Press Release — EurekAlert (AAAS)

- USGS — Potential for Geologic Hydrogen as Next-Generation Energy — U.S. Geological Survey

- Interesting Engineering — Natural white hydrogen source in Canadian Shield — Interesting Engineering

- Discovery Alert — White Hydrogen Exploration 2026 — Discovery Alert (Australia)

- The Brighter Side News — White hydrogen found in billion-year-old Canadian rock — The Brighter Side News