Starlink Earns It, xAI Burns It — The Real Deal SpaceX Is Hiding From IPO Investors

Summary

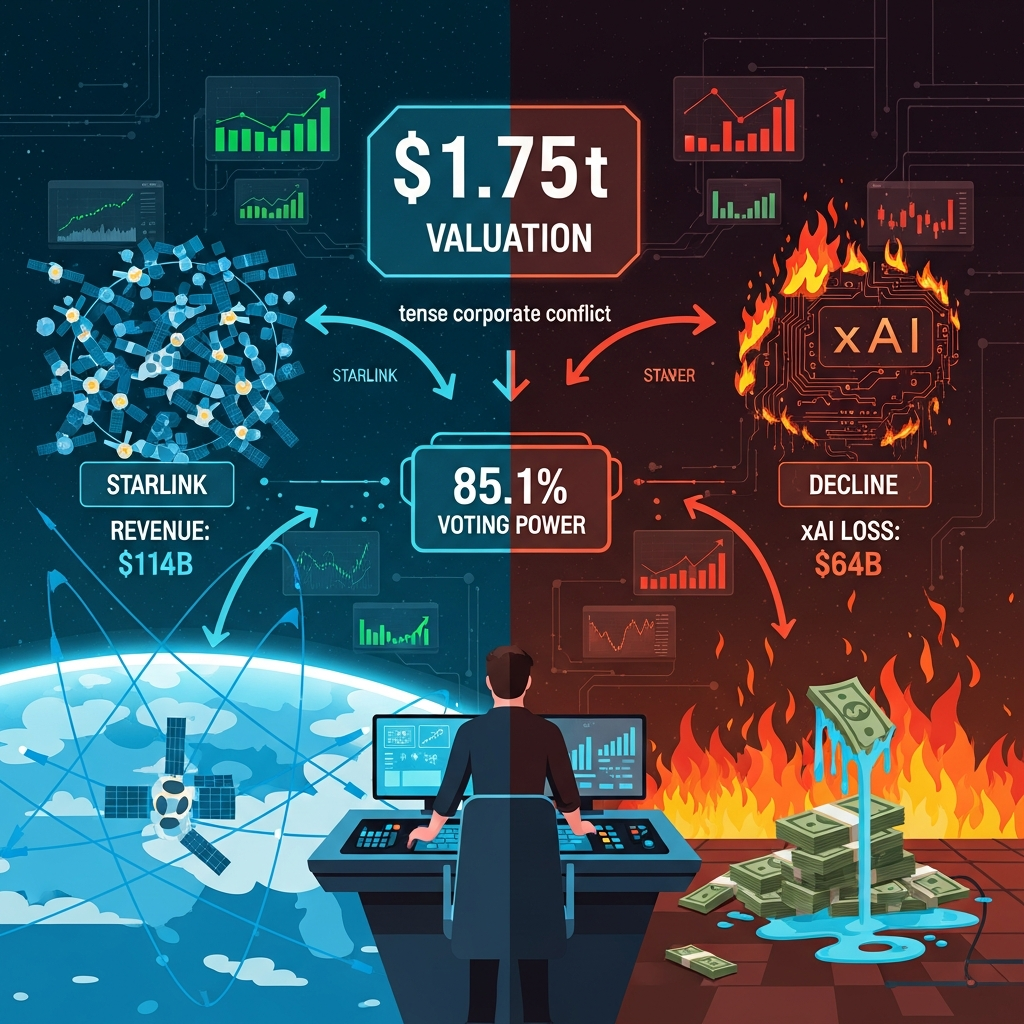

SpaceX's landmark IPO filing with the SEC on May 20, 2026 — targeting a $1.75 trillion market capitalization and a $75 billion public offering — represents the most ambitious capital markets debut in recorded financial history, nearly tripling Saudi Aramco's previous record of $29.4 billion. A methodical reading of the 280-page S-1 prospectus reveals that SpaceX's genuine profit engine is not its rocket business but its satellite internet subsidiary Starlink, which generated $11.4 billion in revenue and $4.4 billion in operating income in 2025 while commanding roughly 90% of the global satellite internet market, effectively underwriting the entire enterprise valuation. The merged xAI entity, absorbed into SpaceX in February 2026, posted a $6.4 billion operating loss in 2025 and deployed $7.7 billion in AI capital expenditure in Q1 2026 alone — an annualized rate of $30.8 billion that exceeds SpaceX's total 2025 revenue — systematically draining the cash flows that Starlink's dominant market position generates. Elon Musk's Class B super-voting shares concentrate 85.1% of total voting power in a single individual, while controlled-company exemptions, mandatory arbitration clauses, and a 3% derivative-suit threshold collectively strip public shareholders of virtually all meaningful governance recourse over management decisions and capital allocation. The IPO's structural character is not that of a space company accessing public markets but of a mechanism for transferring the financial burden of an unvalidated AI wager from private capital onto public investors.

Key Points

Starlink Carries the Enterprise; xAI Consumes the Surplus

SpaceX's 2025 total revenue reached $18.7 billion, of which Starlink contributed $11.4 billion — 61% of the consolidated figure — along with $4.4 billion in operating income and a 63% EBITDA margin that outperforms most major global technology platforms on a like-for-like basis. Starlink's 10.3 million subscribers across 164 countries represent approximately 90% of the global satellite internet market, and the business adds an estimated 20,000 new subscribers daily, reinforcing its near-monopoly position in a market that no competitor can challenge at scale in the near term. The xAI segment — absorbed in February 2026 — generated $3.2 billion in 2025 revenue while recording $6.4 billion in operating losses, a two-to-one loss ratio, with Q1 2026 AI capital expenditure of $7.7 billion annualizing to $30.8 billion — a figure exceeding SpaceX's total 2025 revenue across all segments. The consolidated operating result after merging the launch, Starlink, and xAI segments is a $2.6 billion operating loss, with cash declining from $24.7 billion to $15.9 billion in a single quarter, representing $8.8 billion in net cash consumption at a pace that cannot be sustained without external financing. Quilty Space projects Starlink reaching $20 billion in revenue, $14 billion in EBITDA, and $8.1 billion in free cash flow on a standalone basis by 2026, illustrating both how exceptional the Starlink asset is individually and how significantly the xAI drag distorts the consolidated financial picture that public investors are being asked to value.

85.1% Voting Concentration — History's Largest IPO, History's Weakest Shareholder Rights

Elon Musk holds 93.6% of Class B shares, each carrying 10 votes per share, producing 85.1% of total voting power concentrated in a single individual, a structural arrangement that Fortune summarized as follows: "Musk is mathematically the only person who can fire himself." SpaceX compounded this concentration by electing controlled-company status, which in a single move waives majority-independent board requirements, compensation committee independence requirements, and nominating committee independence requirements — removing the primary institutional constraints that public company boards normally impose on executive discretion. Mandatory arbitration provisions eliminate class action lawsuits and federal court access entirely, cutting off the legal channels through which shareholders in other public companies enforce rights when management acts against investor interests. The derivative suit threshold is fixed at 3% of all outstanding shares — a bar practically only Musk can meet — while SpaceX's 2024 reincorporation sequence from California through Delaware to Texas raised procedural barriers to proxy contests and shareholder proposals further. CalPERS and New York State pension funds filed formal objections to the governance structure; securities attorney Joseph Lucoski characterized it as the most management-protective package he had observed at this scale in U.S. capital market history; and Harvard Law School Forum research documents that dual-class control companies tend to underperform on both governance and financial metrics compared to single-class peers over time.

Grok: 3 Federal Deployments vs. OpenAI's 234 — The AI Story Meets Reality

The federal government's AI procurement inventory functions as one of the clearest available proxies for enterprise AI adoption, and the comparison is stark: OpenAI's products appear in 234 documented federal agency deployments, while Grok appears in three, with those three installations covering basic document drafting and social media management rather than core infrastructure or mission-critical AI applications. The per-agency pricing contrast makes the adoption gap even more pointed: Grok is available at $0.42 per agency versus $1.00 for OpenAI products, a six-to-one price advantage that still fails to generate competitive government adoption — indicating the gap is a product competitiveness problem, not a pricing problem. DARPA prioritizes Google Gemini for engineering analysis workflows and Anthropic Claude for coding and research functions, with Grok absent from both; enterprise adoption in the commercial sector sits at approximately two users per thousand — a penetration rate that registers as a rounding error in a market the S-1 projects at $26.5 trillion. The AI chatbot market more broadly sees ChatGPT holding 60-80% share while Grok's estimated share sits in the low single digits, and xAI's founding team — 10 of 12 original members departed by April 2026 — has largely been replaced, raising additional questions about product trajectory. The S-1 itself acknowledges that "certain target markets do not yet exist," making the chasm between the $26.5 trillion AI TAM thesis and Grok's observable market position the single most consequential valuation risk embedded in this offering.

Dissecting the $1.75 Trillion Target — Premium, Speculation, or Faith?

NYU professor Aswath Damodaran, widely recognized as the foremost practitioner of rigorous corporate valuation methodology, applied a discounted cash flow analysis to SpaceX and arrived at $1.22 trillion in fair value — a 30% discount to the $1.75 trillion IPO target — while PitchBook's independent analysis places the fair value range at $1.1 trillion to $1.7 trillion, positioning the IPO price at the absolute ceiling of the credible band. A 94x trailing revenue multiple exceeds normal valuation territory even for high-growth software companies at peak market conditions, and structural analysis from Investing.com estimates that the two validated business segments — Starlink and the launch division — justify only 10-20% of the total enterprise value, with the remaining 80-90% dependent on unverified future scenarios including Starship's commercial revenue, Starlink's margin durability under competitive pressure, and an orbital AI data center concept that exists only as an FCC filing. The S-1's $28.5 trillion total addressable market figure allocates 93% — approximately $26.5 trillion — to AI markets that the prospectus itself concedes are not yet fully realized, creating a valuation architecture where the great majority of implied value rests on markets that do not currently exist at anything approaching the projected scale. Baron Capital holds $14.9 billion as its single largest position, demonstrating institutional conviction among the bull camp, but conviction among optimists and absence of valuation risk are not the same thing, and the Scottish Mortgage implied value of $1.25 trillion alongside PitchBook's floor of $1.1 trillion suggest a meaningful downside range for investors who enter at the offering price. The core finding across all independent valuation frameworks is consistent: investors paying $1.75 trillion are paying a substantial speculative premium above the current demonstrated value of validated assets, and the premium is justified only if markets and technologies that have not been commercially proven come to fruition within a reasonable investment horizon.

ASC 805-50 Common Control Accounting — How the xAI Merger Obscures Individual Segment Health

The xAI merger was structured as a common-control transaction and processed under ASC 805-50, meaning xAI and X Holdings were absorbed into SpaceX's consolidated financials at historical book value rather than at current market price — an accounting treatment that eliminates the write-down disclosures and goodwill impairment assessments that would have been mandatory under standard third-party acquisition accounting applied to the $44 billion consideration. The practical consequence is that Starlink's 63% EBITDA margin now structurally subsidizes xAI's AI infrastructure losses and X Holdings' declining advertising revenue — projected to fall from $3.4 billion in 2024 to $2.1 billion in 2026 — presenting a consolidated income statement that obscures the standalone financial performance of each constituent entity and makes it difficult for investors to assess the individual investment merit of the businesses they are actually buying. xAI's capital expenditure trajectory — from $1.5 billion in 2024 to a projected $12.5 billion in 2026 — and X Holdings' steady revenue deterioration would present a more alarming picture if either were required to stand alone on a balance sheet, but under common control consolidation, Starlink's exceptional margins provide structural cover for both. The S-1 acknowledges in its risk factor disclosures that the SEC may challenge the accounting treatment applied to the xAI merger, creating a regulatory contingency that exists as a live overhang on the company's reported financials from the moment trading begins. Investors evaluating this offering should understand that the consolidated income statement they are being shown is not equivalent to the sum of three independently viable businesses — it is a blended picture in which Starlink's extraordinary economics provide cover for two subsidiaries that could not currently justify their own capital structures if required to stand alone.

Positive & Negative Analysis

Positive Aspects

- Starlink's Unassailable Market Position and Exceptional Cash Generation

Starlink holds approximately 90% of the global satellite internet market and operates around 60% of all active orbital satellites, a competitive moat built over years of satellite deployment that no rival can close within a near-term timeframe. The 2025 financial profile — $11.4 billion in revenue, $4.4 billion in operating income, 63% EBITDA margin — places Starlink's unit economics favorably above most large-cap technology platforms operating globally, and Quilty Space projects these figures growing to $20 billion in revenue, $14 billion in EBITDA, and $8.1 billion in free cash flow by 2026 on a standalone basis. Amazon's Kuiper constellation had approximately 300 satellites deployed as of early 2026 against Starlink's 9,600-plus, a gap measured in years of catch-up build time, and the network effect compounds: more satellites enable better coverage, attracting more subscribers, generating more cash to fund more satellites. The global satellite internet market is projected to expand from $10.4 billion in 2024 to $22.6 billion by 2030 at a 13.9% compound annual growth rate, and Starlink's position as the absolute market leader with a 164-country operational footprint and 10.3 million existing subscribers creates a structural compounding advantage that late entrants cannot easily replicate regardless of capital deployed. The combination of subscription model predictability, diversified government and enterprise contract revenue, and structural barriers created by the existing satellite fleet makes Starlink one of the most defensible recurring revenue businesses that public investors have had the opportunity to access at any scale in the history of technology IPOs.

- Rocket Launch Market Dominance and Starship Optionality

SpaceX commands approximately 85% of the U.S. orbital launch market and has accumulated $24.4 billion in federal contracts since 2008, including a NSSL Phase 3 Lane 2 contract worth $5.9 billion covering 28 missions through 2027-2032, providing durable contracted revenue that anchors the launch segment regardless of commercial market conditions. Falcon 9's reusable first-stage technology reduced payload-to-orbit costs by an order of magnitude compared to industry baseline, creating a cost advantage that competitors have spent years attempting to match without success, while generating the revenue that funded Starship's development program. Starship's full reusability program — if successfully validated at commercial scale — would deliver another step-change reduction in launch costs below $100 per kilogram, fundamentally altering the economics of large-scale satellite constellation deployment and potential deep-space commercial missions in ways that no existing competitor is positioned to replicate. Defense and intelligence community launch requirements are growing rather than contracting, driven by both national security priorities and the proliferation of small satellite programs, and SpaceX's certified launch heritage with classified payloads provides a competitive barrier that new entrants cannot easily overcome. If Starship achieves commercial operations in the 24-36 month timeframe SpaceX projects, the launch segment transitions from a loss-generating R&D operation to a high-margin commercial platform, representing a potential $200-300 billion upward revision to enterprise value in most analyst models.

- Scarcity Premium and Unprecedented Public Market Access

SpaceX has operated as a private company throughout its entire growth trajectory, with equity available only through restricted secondary markets at prices inaccessible to most institutional and virtually all retail investors, creating years of accumulated demand among potential shareholders who had no direct access. The IPO creates, for the first time, broad public access to a company that has already navigated its highest-risk development phases — early-stage technology validation, market establishment, and competitive moat construction — and moved into large-scale commercial operations generating real cash flows. Secondary market pricing of $622-661 per share across major platforms before the IPO, combined with Polymarket's 98% probability assigned to the $1 trillion-plus market cap scenario, reflects the magnitude of pent-up demand waiting for public access. With 21 bulge-bracket underwriting institutions participating — including Morgan Stanley, Goldman Sachs, and JPMorgan — the IPO has the full distribution infrastructure of the world's largest banks behind it, and the brand equity associated with SpaceX creates a retail investor base analogous to Tesla's, where long-term holder conviction provides structural price support that purely valuation-driven investment positions do not. The long-term holder base that typically forms around founder-driven, mission-oriented companies like SpaceX also tends to reduce panic-driven selling during market downturns, creating a more stable shareholder register than most newly public companies enjoy in their first years of trading.

- Multi-Segment Synergy Potential at Unprecedented Scale

SpaceX's structure — combining orbital launch, global satellite internet, and AI infrastructure in a single corporate entity — creates potential synergies that have no historical precedent in global corporate history, making conventional single-segment valuation frameworks insufficient to capture the full optionality of the combination. Lower launch costs enable cheaper Starlink satellite deployment, expanding the constellation at lower incremental cost; a larger and more capable Starlink network creates a global low-latency communications backbone that has legitimate potential applications as distributed AI computing infrastructure; and the proposed orbital data center concept filed with the FCC would, if validated, produce a category of infrastructure that terrestrial data center operators cannot replicate regardless of capital deployed. Anthropic's monthly compute contract with xAI, valued at $1.25 billion, demonstrates that the AI compute infrastructure being built has tangible value to external AI developers, not only to internal xAI products, and establishes a precedent for third-party monetization of SpaceX's infrastructure investments. The vertical integration structure — controlling the launch economics, the orbital network, and the AI compute layer simultaneously — represents a business model that no single competitor is positioned to challenge across all three dimensions, creating a strategic optionality that justifies some premium above what any single segment would warrant in isolation. The scale required to build and sustain this vertically integrated space-internet-AI platform creates compounding barriers to competitive entry that grow rather than diminish over time, meaning the strategic value of the combination increases as the technology matures and competitors face an ever-larger gap to close.

Concerns

- xAI's Uncapped Cash Burn and Unvalidated Revenue Model

xAI's operating losses expanded from $1.56 billion in 2024 to $6.4 billion in 2025 — a fourfold increase in a single year — with Q1 2026 AI capital expenditure of $7.7 billion annualizing to $30.8 billion, a spending velocity that exceeds SpaceX's entire 2025 annual revenue across all business segments and has no clear ceiling established in the S-1. Cash balances declined from $24.7 billion to $15.9 billion in a single quarter, representing $8.8 billion of net consumption, and if this pace is maintained, even the $75 billion IPO raise provides finite runway rather than indefinite financial security. Grok's enterprise penetration — two users per 1,000 in commercial markets, three federal agency deployments versus OpenAI's 234 — provides no current evidence supporting the capital deployment thesis at anywhere near the current spending rate, and the six-to-one pricing advantage Grok carries over OpenAI products has not translated into measurable adoption gains. The standard counter-argument that AWS and Google Cloud also sustained large losses in their early years fails on a critical dimension: AWS invested in infrastructure against validated, growing enterprise demand that already existed at the point of investment, while xAI is building data center capacity before establishing that demand exists at any comparable scale. S&P Global has publicly flagged the probability that SpaceX will need to return to capital markets within a few years at the current consumption rate, making dilution of post-IPO shareholders a structural rather than merely theoretical risk.

- The Bridge Loan Structure and Pre-Committed IPO Proceeds

SpaceX executed a $20 billion bridge credit facility in March 2026, arranged by Goldman Sachs, Bank of America, Citi, JPMorgan, and Morgan Stanley — the same institutions underwriting the IPO — containing a provision requiring repayment within six months of the listing using public offering proceeds, meaning a significant portion of the $75 billion raised may flow immediately to debt retirement rather than corporate investment. This creates a structural dynamic where investors contributing capital to what they understand as growth financing may in effect be providing liquidity to retire short-term debt incurred by the company before the IPO, reducing the actual deployment of proceeds into business-building activities. Total debt grew from $22.05 billion at end-2024 to approximately $29.1 billion by March 2026 including additional financing obligations, carrying annual interest expense of roughly $900 million, and the bank syndicate that arranged the bridge has a financial incentive to complete the IPO at maximum price regardless of whether the valuation serves incoming investors' interests. If cash burn rates remain at the Q1 2026 pace after the bridge is repaid, SpaceX could require capital market access again within 18-24 months of listing, with dilution implications for early shareholders who assumed the IPO would provide multi-year financial stability. The opacity of how IPO proceeds will actually be allocated — given the bridge repayment obligation, ongoing xAI capex requirements, and accumulated debt service costs — makes it genuinely difficult for incoming investors to determine what fraction of their contributed capital will fund future value creation versus retiring financial obligations already incurred before they joined as shareholders.

- Starlink ARPU Compression as a Structural Revenue Risk

Monthly average revenue per Starlink subscriber has declined consistently and significantly: from $99 in 2023 to $91 in 2024, $81 in 2025, and $66 in Q1 2026, a 23% year-over-year deterioration that the S-1 acknowledges explicitly while framing it as currently offset by subscriber volume growth. That framing contains a critical embedded assumption — that subscriber growth can continue to compensate for declining per-unit economics indefinitely — which may not hold as developed-market penetration approaches saturation and emerging-market additions carry structurally lower revenue per account. Amazon Kuiper's entry into commercial service and China's Qianfan project targeting 15,000 satellites will introduce pricing competition into markets where Starlink currently operates without meaningful rivalry, threatening to accelerate ARPU compression at precisely the moment subscriber velocity may be decelerating due to market maturity dynamics. At a 94x revenue multiple, a business where the primary revenue driver's per-unit economics are deteriorating at 23% annually requires an extraordinary subscriber growth rate to maintain the valuation arithmetic, and there is no established precedent for any consumer subscription business sustaining that compensatory dynamic indefinitely in the face of competitive entry. The structural risk — ARPU declines while subscriber growth slows simultaneously — is a core scenario the bull case must address, not a tail risk that can be dismissed as unlikely.

- Governance Architecture Systematically Eliminates Shareholder Recourse

The 85.1% voting concentration is extreme by any historical benchmark for public companies at this scale, but SpaceX has added three complementary protective mechanisms that eliminate the remaining accountability channels available to shareholders in other public companies. Controlled-company status removes majority-independent board requirements, compensation committee independence, and nominating committee independence in a single election, meaning no board mechanism exists with the independence to challenge management decisions on strategic direction, capital allocation, or executive compensation. Mandatory arbitration clauses foreclose both class action lawsuits and direct federal court access simultaneously, eliminating the most effective legal remedies historically available to public investors when management acts contrary to shareholder interests at scale. The 3% derivative suit threshold requires ownership of more than 3% of all outstanding shares to file a lawsuit on behalf of the company — a bar practically only Musk himself can clear — while SpaceX's reincorporation sequence to Texas raises additional procedural barriers to proxy contests and shareholder proposals that institutional investors have traditionally used as governance pressure tools. Harvard Law School Forum research documents that companies with dual-class share structures underperform on both governance and financial metrics over time compared to single-class peers, and the specific precedent cases — Snap, Groupon, GoPro — all experienced significant post-IPO value destruction following super-voting structures where management judgment diverged from investor interest without accountability mechanisms to course-correct.

- xAI Founding Team Exodus and Technology Competitive Uncertainty

Of xAI's 12 original founding team members, two remained as of April 2026, representing an 83% departure rate among the people who conceived the original technical vision, product architecture, and competitive strategy for the AI business that is consuming $30 billion in annualized capital expenditure. An AI company that has lost its founding intellectual core while simultaneously justifying the largest AI infrastructure investment program by any single entity presents a risk profile for which there is limited historical precedent: the people who designed the original strategy are largely gone while the infrastructure built to execute that strategy is expanding at maximum velocity. Grok's 117 million monthly active users sounds significant in isolation, but this user base is almost entirely derived from the existing X platform ecosystem rather than independent AI product adoption — representing a captive distribution channel, not enterprise AI deployment at scale. The Anthropic compute contract at $1.25 billion monthly carries a 90-day termination clause, classifying it as a transitional bridge revenue arrangement rather than a durable contracted revenue stream that justifies infrastructure investment at the current scale. The combination of founding team exodus, limited enterprise adoption outside the X ecosystem, heavily contingent near-term revenue, and a competitive landscape dominated by OpenAI, Anthropic, and Google DeepMind — each with larger enterprise footprints and more stable research organizations — creates a risk profile for the xAI segment that the S-1's $26.5 trillion TAM framing does not adequately capture.

Outlook

Let me lay out where I see this heading across three time horizons — short, medium, and long-term — with bull, base, and bear scenarios for each. The goal here isn't to predict a stock price. It's to map the structural variables that will determine whether this deal serves public investors over time or extracts value from them.

The short-term window runs from the June 2026 listing through the end of the year. On the bull side, the initial market reception is likely to be spectacular by almost any historical measure. SpaceX shares have been changing hands in secondary markets at $622 to $661 per share on major platforms, and Polymarket pre-listing probability markets placed the $1 trillion-plus market cap scenario at 98% probability and the $2 trillion-plus scenario at 72%. With 21 bulge-bracket underwriting banks — Morgan Stanley, Goldman Sachs, JPMorgan, and 18 others — organized behind the distribution, institutional allocation demand will absorb a significant portion of the float. When shares of a company that has been inaccessible to ordinary investors throughout its most transformative years finally enter public markets, scarcity premium drives buying well above fundamental valuation. I see a credible scenario where SpaceX opens at or above $2 trillion on day one, propelled by years of pent-up institutional and retail demand that has had no direct access to this equity.

The short-term bear scenario, however, centers on cash mechanics that the headline numbers obscure. SpaceX executed the $20 billion bridge credit facility in March 2026 with a provision requiring repayment within six months of the IPO using public offering proceeds. This means $20 billion or more of the $75 billion raised may flow immediately to debt retirement rather than into the business. If Q2 2026 earnings confirm that xAI's capital expenditure maintained or exceeded the Q1 pace of $7.7 billion per quarter, and Grok's enterprise adoption metrics remain in the single digits, the AI narrative that underpins the premium multiple will deflate rapidly. S&P Global has already flagged the possibility that SpaceX may need to return to capital markets within a few years at current consumption rates. The cash balance — $15.9 billion at end of Q1 2026 — does not represent unlimited runway at the current burn rate. The first post-listing earnings call may be the single most important near-term catalyst for price discovery in either direction.

The medium-term picture — six months to approximately two years, through mid-2027 — hinges on two variables I believe will separate bull and bear outcomes more definitively than any others. The first is Starlink's subscriber trajectory paired with ARPU defense. If Starlink reaches 20 million subscribers by mid-2027 while holding ARPU at $70 or above, the revenue arithmetic becomes genuinely compelling: 20 million users at $70 monthly produces $16.8 billion in annual run-rate revenue, a 47% increase from 2025 levels, and at a 63% EBITDA margin that generates roughly $10.6 billion in EBITDA — sufficient to absorb meaningful xAI losses while still producing positive consolidated cash generation. The medium-term bull case layers onto this Starship beginning to generate commercial payload revenue and Grok securing 50 or more federal contracts, pushing xAI's revenue toward $8-10 billion annually with losses narrowing. Under that combination, a $2.5 trillion sustained market capitalization through 2027 is defensible. Damodaran's $1.22 trillion fair value likely acts as a structural floor in most scenarios short of a major negative revelation.

The second decisive medium-term variable is competitive pressure in the satellite internet market. Amazon Kuiper was actively deploying satellites as of early 2026 — approximately 300 in orbit with a target of 7,774 — and Amazon's logistics and capital infrastructure enable rapid constellation buildout. China's Qianfan project is targeting 15,000 satellites. Starlink's 90% market share almost certainly represents a historical peak; I model 65-75% as a realistic medium-term equilibrium once Kuiper achieves commercial viability at scale. Simultaneously, if xAI's annualized capex remains above $250 billion and ARPU continues its downward trajectory, SpaceX's cash position will require either additional equity issuance or debt financing within 18-24 months of the IPO. The medium-term bear scenario lands SpaceX in a PitchBook floor range of $1.1 trillion, with dilution risk materializing for post-IPO shareholders.

The long-term horizon — two to five years, spanning 2028 through 2031 — is where the company's fate diverges most sharply depending on variables that cannot be modeled with confidence today. The bull case requires three simultaneous realizations: Starship achieving full reusability and generating commercial payload revenue at scale, Starlink evolving into a planetary communication backbone serving 50-100 million subscribers, and xAI emerging as a genuine revenue-generating AI platform. If Starship's full reusability drives payload costs below $100 per kilogram to orbit, the economics of constellation deployment transform fundamentally — SpaceX could expand Starlink from 9,600 to the FCC-approved 15,000, and ultimately toward the 42,000-satellite plan, at a fraction of current build cost. Global satellite internet penetration reaching 200 million subscribers by 2030 is a published research projection; if Starlink captures half that base at an ARPU of $50, annual satellite revenue alone exceeds $60 billion, more than triple SpaceX's 2025 total. That is the scenario where a $3-5 trillion long-term valuation becomes mathematically grounded rather than aspirational. ARK Invest's 2030 target of $2.5 trillion could be reached in the medium term under this scenario.

The long-term bear case is less catastrophic in absolute terms but more humbling for investors who entered at $1.75 trillion. In this scenario, xAI fails to establish the competitive standing its capital investment implies — the founding team exodus, combined with OpenAI's 234-to-3 federal adoption advantage, proves structurally difficult to close — and xAI is eventually spun off or reorganized. SpaceX reverts to its core identity: a launch company and satellite internet provider operating at high margins in a more competitive but still profitable market. Starlink's standalone fair value under this scenario remains genuinely significant — credible estimates range from $600 billion to $800 billion — but insufficient to justify the $1.75 trillion IPO price, meaning investors who entered at listing could face a 5-10 year timeline to principal recovery, particularly if a secondary offering dilutes their position.

Beyond the financial scenarios, there is a governance precedent dimension to this IPO that I think deserves explicit attention. If SpaceX successfully completes the largest IPO in history while maintaining 85.1% voting concentration, eliminating class action access through mandatory arbitration, and setting a 3% derivative suit threshold, it establishes a template for other founder-controlled companies. Harvard Law School Forum research documents that dual-class control companies underperform on governance and financial metrics over time; Snap, Groupon, GoPro, and WeWork all experienced post-IPO deterioration following super-voting structures. Whether SpaceX breaks that historical pattern or confirms it will be one of the defining case studies in capital markets governance for the next decade, with implications extending well beyond this single company.

I want to close with an honest acknowledgment: I could be wrong about xAI and Grok. Musk's execution track record is historically documented across situations where conventional analysis said the venture was impossible — Tesla's profitability, Falcon 9's reusability, and SpaceX's survival through near-bankruptcy in 2008 are all part of that record. If Grok achieves 10-15% enterprise market share by 2028 and the orbital data center concept proves technically and economically viable, the current skepticism will join a long list of "wrong pessimism" about Musk ventures. I estimate that probability at roughly 15-20%. It is not zero, and the upside if it materializes is 2-3x the current price — a meaningful expected value argument. But investing here means accepting that you are funding an AI wager on behalf of someone who controls 85.1% of the votes, with no mechanism to redirect that capital if the wager deteriorates, and no institutional pathway for recourse if management decisions prove contrary to shareholder interests. Whether that is an investment or an act of faith in a single individual is a distinction worth drawing with full awareness before committing capital.

Sources / References

- SpaceX S-1 Official Financial Data: Starlink $11.387B Revenue, xAI $6.355B Operating Loss — Yahoo Finance / SEC S-1

- SpaceX S-1 Full Prospectus: Class B 10-to-1 Voting Rights, 85.1% Voting Control, Controlled-Company Election, Mandatory Arbitration Clause — SEC EDGAR

- SpaceX Shareholder Rights Concerns: CalPERS and New York Pension Fund Objections, Joseph Lucoski Expert Commentary — Fortune

- Damodaran DCF Fair Value Analysis: $1.22 Trillion (30% Below IPO Target) — The Motley Fool

- Bull/Base/Bear Scenario Analysis, Starlink ARPU Decline from $99 to $66, Polymarket Probability Data, xAI Founding Team Departures — TechMarketBriefs

- Dual-Class Share Structures: Governance Risks and Company Performance Research — Harvard Law School Forum on Corporate Governance

- Grok Federal Government AI Adoption: 3 Deployments vs. OpenAI's 234 — CryptoBriefing

- Common Control Accounting Under ASC 805-50: xAI Merger Transaction Analysis — DevelopmentCorporate

- SpaceX $20 Billion Bridge Loan With Six-Month IPO Repayment Clause — U.S. News / Reuters

- SpaceX vs. History's Largest IPOs: Saudi Aramco $29.4 Billion Record Comparison — Euronews