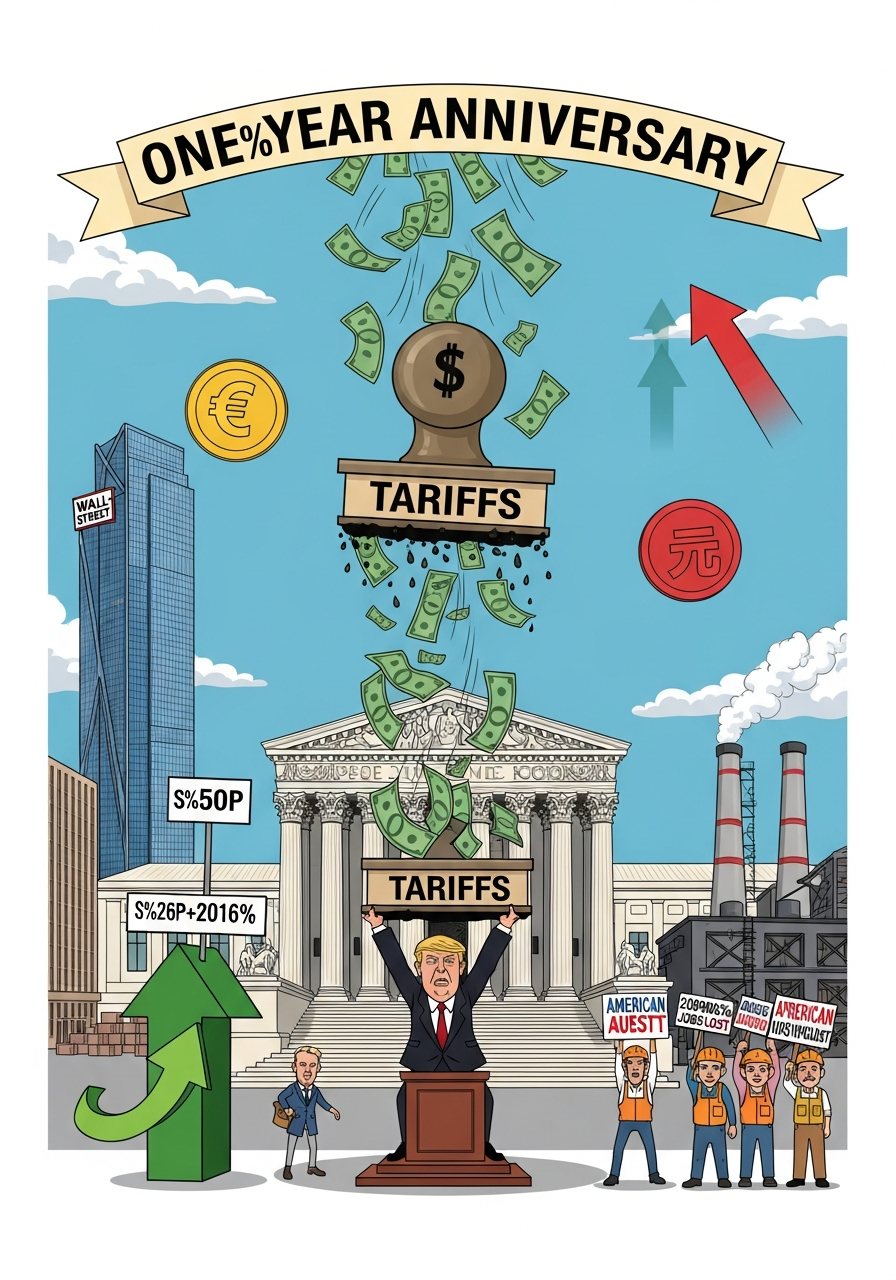

He Was Forced to Return $166 Billion, Then Pulled Out New Tariffs — A One-Year Report Card for Liberation Day

Summary

Trump's Liberation Day tariffs have reached their one-year mark. The Supreme Court struck down IEEPA tariffs in a 6-3 ruling, ordering approximately $166 billion in refunds to some 330,000 importers. Yet on the very anniversary, the administration announced 100% pharmaceutical tariffs and 25% metals derivative tariffs under Section 232 — a move legal scholars are calling 'legal basis shopping.' Over this year, US manufacturing shed 89,000 jobs while KOSPI surged 76.5% and Nikkei climbed 61.9%, both outpacing the S&P 500's 16.4% gain, and the Dollar Index fell 9%, accelerating de-dollarization discussions worldwide.

Key Points

The Largest Tariff Refund in History — The Weight of $166 Billion

On February 20, 2026, the US Supreme Court ruled 6-3 in Learning Resources v. Trump that IEEPA tariffs were unconstitutional. The majority held that while the International Emergency Economic Powers Act grants the President authority to 'regulate' imports during national emergencies, this does not clearly authorize tariff imposition. The ruling triggered refunds on over 53 million customs entries filed by approximately 330,000 importers, totaling roughly $166 billion. US Customs and Border Protection is building a new refund system called CAPE, which was 45-80% complete as of March 2026. The Penn Wharton Budget Model estimates total refunds including interest could reach $175 billion. This represents the largest tariff refund in US trade history and stands as a definitive judicial check on executive overreach in tariff authority.

Legal Basis Shopping on the Anniversary — From IEEPA to Section 232

When the Supreme Court struck down IEEPA tariffs, the Trump administration pivoted with remarkable speed. On the Liberation Day anniversary of April 2, 2026, the White House announced 100% tariffs on pharmaceuticals and 25% tariffs on steel and aluminum derivative products, this time under Section 232 of the Trade Expansion Act of 1962. Section 232 allows import restrictions for 'national security' reasons, but extending this to pharmaceuticals represents an unprecedented interpretation. Legal scholars have begun calling this 'legal basis shopping' — swapping one statutory authority for another to maintain tariffs regardless of court rulings. Pharmaceutical tariffs include 120-day grace periods for large companies and 180 days for smaller ones, with a 0% tariff through January 2029 for companies entering Most Favored Nation pricing agreements. A separate 15% tariff applies to pharmaceuticals from the EU, Japan, Korea, and Switzerland.

Wall Street Laughs While Main Street Cries — The Paradox of 89,000 Lost Jobs

The stated goal of tariffs was American manufacturing revival. The actual data tells the opposite story. According to BLS figures, US manufacturing lost 89,000 jobs between Liberation Day and February 2026, averaging roughly 9,000 jobs lost per month. Durable goods manufacturing — cars, appliances, electronics — took the heaviest hit. For the full year 2025, 108,000 manufacturing jobs disappeared, marking the third consecutive year of decline. Meanwhile, the S&P 500 rebounded from the Liberation Day shock to gain approximately 16.4%. FDI totaled $288.4 billion — over an order of magnitude smaller than Trump's claims and below the 10-year average of $320.7 billion. Tariffs became a textbook case of protecting capital markets while sacrificing labor markets.

The Global Market Reversal — What KOSPI's 76.5% and Nikkei's 61.9% Really Mean

The most dramatic change since Liberation Day is the reversal in global equity markets. In 2025, the MSCI All Country World ex-USA index rose 29.2%, significantly outpacing the S&P 500's 16.4%. South Korea's KOSPI surged 76.5% since Liberation Day, while Japan's Nikkei 225 delivered 61.9%. The Nasdaq 100 ranked only fourth among major indices at 47.2%. Brazil's Bovespa gained 33.4% and Hong Kong's Hang Seng rose 28.7%. This is not simple capital rotation but a fundamental market reassessment of American Exceptionalism. Global capital concentrated in US mega-cap tech has begun migrating toward undervalued opportunities in Europe and Asia, a trend difficult to reverse while tariff uncertainty persists.

The Dollar's Quiet Retreat — A 9% DXY Drop and Accelerating De-dollarization

The Dollar Index (DXY) fell 9.0% in 2025, its steepest annual drop since 2017. Major FX research houses including ABN AMRO and MUFG project an additional 5% decline in 2026, with EUR/USD forecasted to reach 1.24 by year-end. The OMFIF Global Public Investor 2025 survey shows global central bank reserve managers planning to increase euro allocations. While the dollar still holds 56.92% of global reserves maintaining its reserve currency status, the euro follows at 20.33% and the yuan's institutional rise is becoming visible. Trade uncertainty triggered by tariffs is shaking the dollar's safe-haven status, representing not short-term FX volatility but the beginning of a gradual yet structural transformation in the global reserve currency order.

Positive & Negative Analysis

Positive Aspects

- Forced Acceleration of Supply Chain Diversification

The most tangible positive effect of tariffs has been the forced diversification of global supply chains. The goal of reducing single-source dependency on China would not have been achieved this quickly without tariff pressure. Production shifts to Vietnam, India, and Mexico accelerated, and global semiconductor firms including Samsung and TSMC announced US factory construction. For pharmaceutical tariffs, the White House claims it has already secured $400 billion in domestic investment commitments. Reducing China concentration risk in supply chains can enhance long-term US economic resilience, and on this point alone, tariffs functioned as an effective policy tool.

- Establishing Trade Negotiation Leverage

Tariffs as a 'maximum pressure' tool have positioned the US favorably in trade negotiations. The MFN exemption provision for pharmaceutical tariffs is a prime example. Setting an extreme 100% tariff rate and offering exemption to companies that match Most Favored Nation drug pricing effectively uses tariffs as negotiation chips. The differentiated 15% rate for the EU and Japan reflects existing trade relationships. The negotiation leverage secured through tariffs still holds potential for genuine improvement in trade terms.

- Catalyzing Domestic Semiconductor and Advanced Manufacturing Investment

The combination of tariff pressure and the CHIPS Act has produced visible results in semiconductors. TSMC's Arizona fab, Samsung's Texas fab, and Intel's domestic investment expansion represent undeniable achievements in attracting advanced semiconductor manufacturing to the US. These investments carry strategic value beyond job creation, strengthening US technology sovereignty and national security capabilities. While tariffs alone did not drive these investment decisions, they clearly served as a catalyst forcing companies to seriously consider domestic production.

- Expansion of Emerging Market Investment Opportunities

The paradoxical beneficiaries of tariff uncertainty are emerging market investors. Returns of 76.5% for KOSPI, 61.9% for Nikkei, 33.4% for Bovespa, and 28.7% for Hang Seng served as a wake-up call for global investors overly concentrated in US-centric portfolios. As global capital migrates from US mega-caps toward undervalued Asian and European assets, a virtuous cycle of improving liquidity and valuations is forming in emerging markets. While an unintended consequence of tariffs, this effectively corrects the excessive US concentration in global capital markets.

Concerns

- Manufacturing Job Losses — The Opposite of What Was Promised

The primary justification for tariff policy — manufacturing job creation — has completely failed. The BLS-documented 89,000 job losses are not just numbers but represent tens of thousands of families facing economic instability. The full year 2025 saw 108,000 job losses, marking the third consecutive year of manufacturing employment decline. Durable goods manufacturing, particularly automotive and appliance sectors, suffered the greatest impact. The irony is that tariff-driven raw material cost increases actually weakened domestic manufacturers' competitiveness. A brief 5,000 job gain in January 2026 was immediately reversed by a 12,000 decline in February.

- Consumer Price Burden Pass-Through

Tariffs are fundamentally taxes on imported goods, with costs ultimately passed to consumers. Analysis suggests that 100% pharmaceutical tariffs could raise US drug prices by 30-50%. Since these tariffs target patented rather than generic drugs, patients dependent on irreplaceable medications face the greatest harm. The 25% tariff on steel and aluminum derivative products will inevitably increase prices for automobiles, appliances, and construction materials. According to the Progressive Policy Institute, tariff-related additional annual costs per household average $1,700 to $2,400.

- Self-Inflicted Damage to Dollar Hegemony

The 9% DXY decline is not mere exchange rate fluctuation but a symptom of eroding confidence in the dollar-centric financial system. Weaponizing tariffs, overusing economic sanctions, and repurposing IEEPA for tariffs have transformed the dollar from a safe-haven asset into one carrying political risk. The OMFIF survey showing central banks planning to increase euro allocations provides data backing these concerns. Reserve currency status, once shaken, is extremely difficult to restore — as the British pound's precedent shows, it erodes over decades. That tariff policy is gnawing away at dollar hegemony, America's greatest structural privilege, rather than reviving domestic manufacturing represents the most serious long-term risk.

- Retaliatory Tariffs and Global Trade Fragmentation Risk

Unilateral tariff imposition triggers retaliatory tariff spirals. Major trading partners including China, the EU, and Canada have launched or are reviewing retaliatory tariffs on American agricultural products, energy, and services. These countermeasures fragment global trade into blocs and undermine the WTO-centered multilateral trading order. Pharmaceutical tariffs are particularly concerning as they use national health as a tariff policy tool, giving other countries justification to impose retaliatory tariffs on American pharmaceuticals and medical devices using similar logic. Global trade fragmentation raises costs and reduces efficiency for all participants — a negative-sum game.

- Chronic Legal Uncertainty

The pattern of swapping legal bases from IEEPA to Section 232 to Section 122 chronically entrenches legal uncertainty in US trade policy. Businesses face an unpredictable landscape where any tariff could face constitutional challenge tomorrow and new tariffs could appear under yet another statutory authority. This legal uncertainty delays long-term investment decisions and causes companies to reconsider US market entry. According to Reason.com's analysis, tariffs imposed without congressional vote are fundamentally lacking legitimacy, and legal challenges to Section 232 are merely a matter of time. Legal basis shopping maintains tariffs short-term but erodes trust in the US trade legal framework itself long-term.

Outlook

Let me start with what will happen in the next few months. The most urgent issue is the implementation timeline for the 100% pharmaceutical tariffs. Large companies have a 120-day grace period and smaller ones get 180 days, meaning tariffs on major firms could kick in as early as August 2026. The critical question is how many pharmaceutical companies can finalize MFN pricing agreements within those 120 days, and frankly, I am skeptical. Getting global pharma companies to lower US drug prices to European or Japanese levels is a challenge that has defeated policymakers for decades, and it will not be solved in 120 days. Consider the numbers: the average US brand-name drug price is roughly 2.5 to 3.4 times higher than comparable prices in the EU or Japan. Closing that gap requires restructuring entire pricing models, renegotiating pharmacy benefit manager contracts, and navigating a labyrinth of regulatory approvals that simply cannot be compressed into four months.

If the 100% tariff takes effect without MFN agreements, the consequences could be severe. US drug prices could surge 30-80% depending on the medication. Patients relying on irreplaceable patented drugs for cancer, rare diseases, and autoimmune conditions would bear the brunt. Insurance cost pressures would intensify, with premium hikes becoming visible during the 2027 renewal season. The Congressional Budget Office has not yet scored the full impact, but private actuarial estimates suggest employer-sponsored health insurance premiums could rise 8-15% above baseline trends. This becomes the defining political variable for the November 2026 midterm elections, because voters feeling price increases at the pharmacy carry far more political force than abstract trade statistics.

The $166 billion refund process is another critical near-term variable. CBP's CAPE system is expected to be completed by late April with the refund plan submitted, but processing 53 million refund entries across 330,000 importers is an unprecedented administrative challenge. For context, the largest previous customs refund program processed fewer than 2 million entries. The logistical complexity here is staggering — each entry must be individually verified against the original tariff payment, interest calculated from the date of collection, and the refund routed through the correct financial channels. Once refunds begin, corporate liquidity will improve, but whether that capital flows into US domestic investment or into offshore hedging positions is an entirely different question. My assessment is that most importers will channel refund capital toward supply chain diversification outside the US rather than domestic reinvestment. The very unpredictability of tariff policy may paradoxically accelerate investment outside America. Companies that just received refunds for unconstitutional tariffs have every rational incentive to reduce their future exposure to US import-dependent business models.

Looking at the medium-term horizon of six months to two years, an era of sustained legal warfare will unfold. Applying Section 232 to pharmaceuticals rests on legally fragile reasoning. Import restrictions based on 'national security' have traditionally been confined to defense-related materials like steel and aluminum. Extending this to pharmaceuticals effectively means any import could fall under Section 232, a scope that courts are unlikely to accept. The Commerce Department's Section 232 investigation into pharmaceuticals took less than 90 days — a pace that raises serious questions about procedural rigor when previous 232 investigations into steel and aluminum each took over a year. By mid-2027, legal challenges to Section 232 pharmaceutical tariffs will very likely reach federal courts, and if they reach the Supreme Court, the IEEPA ruling's logic could be applied expansively. The six justices who struck down IEEPA tariffs articulated a clear principle: statutory authorities cannot be stretched beyond their original legislative intent to grant the executive unlimited tariff power.

During this same period, global trade realignment will accelerate further. RCEP member countries already see intra-regional trade exceeding 45% of their total trade, and unilateral US tariff policy is pushing this trend harder. The EU may reopen investment agreements with China, and ASEAN nations will refine their dual-track strategies between the US and China. South Korea's KOSPI surge of 76.5% reflects not just strong semiconductor exports but the structural flow of global capital away from the US. Samsung Electronics alone saw foreign investor inflows of approximately $12 billion in the second half of 2025, reversing years of outflows. If this flow persists through the medium term, KOSPI breaking the 4,000 level is entirely plausible. Japan's Nikkei, buoyed by corporate governance reforms under the Tokyo Stock Exchange's 'Corporate Value Improvement' initiative, has attracted over $45 billion in foreign capital since Liberation Day, with many institutional investors explicitly citing US tariff uncertainty as the catalyst for their allocation shift.

Dollar weakness is likely to deepen over the medium term. If ABN AMRO's forecast materializes with DXY falling another 5% by end-2026 and EUR/USD reaching 1.24, this would represent a return to 2017-2018 levels. The crucial difference is context: in 2017, dollar weakness reflected natural global recovery dynamics, but today it reflects a 'distrust discount' on US policy uncertainty. This type of currency weakness does not easily reverse with rate hikes alone. The Federal Reserve faces a painful dilemma — raising rates to defend the dollar risks tipping an already fragile manufacturing sector into deeper contraction, while holding rates steady allows the dollar slide to continue. For the yuan, Chinese authorities will likely tolerate gradual appreciation while maintaining a strategic balance between export competitiveness and internationalization. The People's Bank of China has quietly expanded yuan-denominated trade settlement agreements with 23 additional countries since April 2025, a development that receives far less attention than it deserves.

Moving to the two-to-five-year long-term outlook, I believe we are entering the most significant period of global trade order restructuring since the Bretton Woods system. I acknowledge this is a bold claim, but the data points in this direction. The IEEPA unconstitutionality ruling is not merely a legal judgment but a fundamental reset of presidential unilateral trade authority. The long-term impact may manifest as Congress reclaiming trade policy leadership from the executive branch. New York's Attorney General is already urging Congress to legislate tariff refunds, potentially signaling the beginning of a broader congressional trade authority restoration movement. Several bipartisan bills have been introduced in both chambers aiming to require congressional approval for tariffs exceeding 10%, and while none have passed yet, the political momentum is building as the economic costs of executive tariff authority become impossible to ignore.

The most consequential long-term change concerns the dollar's status. I assign roughly 45% probability to the dollar's share of global foreign exchange reserves falling below 50% by 2030, from its current 56.92%. The British pound's loss of reserve currency status unfolded over approximately 57 years from the start of World War I in 1914 to the Nixon Shock in 1971. For the dollar, taking the 2018 US-China trade war as the starting point means only 8 years have passed, but given the pace of technological advancement, the transition could proceed far faster than the pound's precedent. Digital yuan, BRICS Pay, euro-based payment infrastructure, and growing cryptocurrency markets are all emerging as dollar alternatives. The IMF's latest COFER data shows the dollar's reserve share declining at an average rate of 0.7 percentage points per year since 2020 — if this pace continues, the 50% threshold is reached by 2030. If the pace accelerates due to continued tariff weaponization, it could arrive sooner. Gold reserves, meanwhile, have surged to record levels at central banks worldwide, with net purchases exceeding 1,000 tonnes annually for three consecutive years — a clear hedge against dollar uncertainty.

Let me run through three scenarios. The bull case looks like this: MFN negotiations succeed with most global pharma companies agreeing to lower US prices, domestic production facility investments materialize creating over 100,000 high-quality manufacturing jobs in pharmaceuticals alone by 2028, and Section 232 tariffs withstand legal challenges while actually reviving domestic metals industries and fully domesticating automotive and defense supply chains. In this scenario, tariffs would be judged as a strategic success worth the short-term pain. The DXY stabilizes around 95, manufacturing employment reverses its decline, and the US trade deficit narrows by 15-20%. I put this at roughly 15% probability.

The base case, which I consider most likely at approximately 55% probability, sees MFN agreements reached with only some major pharmaceutical companies, resulting in partial tariff implementation. Drug prices rise 10-20% but remain politically manageable. Manufacturing jobs decline further before bottoming in mid-2027 and gradually stabilizing around 12.2 million — still below the pre-Liberation Day level of 12.8 million. The dollar finds a new equilibrium around DXY 85-90, maintaining reserve currency status but shifting from absolute dominance to relative primacy. KOSPI and Nikkei outperformance persists through 2027 before the gap narrows as global capital flows find a new balance. The US trade deficit remains stubbornly wide despite tariffs, as domestic production capacity simply cannot replace imports quickly enough.

The bear case carries roughly 30% probability and cannot be dismissed. Section 232 pharmaceutical tariffs take full effect as MFN negotiations fail, causing US healthcare costs to spiral and insurance company distress to expand into a systemic healthcare crisis. Hospital systems already operating on thin margins — the median US hospital operating margin was just 1.5% in 2025 — face drug cost increases they cannot absorb, leading to service cuts, closures in rural areas, and a potential wave of hospital bankruptcies. Simultaneously, the EU and China impose aggressive retaliatory tariffs on American agricultural products and services, contracting global trade volumes 15-20% below 2019 levels. DXY plunges below 80, reigniting import price inflation, trapping the Fed between rate hikes and recession. In this scenario, a 2028-2029 recession becomes almost certain, with the S&P 500 potentially falling 25-30% from current levels and unemployment rising above 6%.

One additional dimension worth highlighting is the cascading effects of tariff policy. The first-order effect is higher import prices, but second-order effects include global supply chain restructuring, and third-order effects involve shifts in the global reserve currency order. The speed of this domino chain has been faster than expected, and that is perhaps the most important lesson from this first year. Almost nobody predicted a year ago that KOSPI would reverse past the S&P 500 by this magnitude. Similarly, the changes we will witness two to three years from now may be far more dramatic than current consensus suggests. The fourth-order effect — which very few analysts are discussing — is the potential restructuring of global pharmaceutical supply chains in ways that could permanently alter which countries control essential medicine production. If pharmaceutical tariffs persist, the EU, India, and China have strong incentives to build entirely self-sufficient drug manufacturing ecosystems that bypass the US market entirely, reducing American leverage in future negotiations.

My recommendation to readers is to seriously consider geographic diversification in their portfolios. US-centric portfolios were the optimal strategy for the past 15 years, but maintaining this approach in the face of structural changes like tariff uncertainty and dollar weakness carries substantial risk. Asian market structural undervaluation offers particularly attractive medium-term opportunities. The returns demonstrated by KOSPI and Nikkei may not be short-term anomalies but reflections of a structural shift in global capital flows. Specifically, I would suggest gradually increasing non-US equity allocation from the typical 20-30% to 35-45% over the next 12-18 months, with particular attention to Korean semiconductors, Japanese corporate reform beneficiaries, and Indian infrastructure plays. However, do not forget that currency risk management is essential when the dollar is weakening — a 50% hedge ratio on non-dollar exposure is a sensible baseline.

Ultimately, the future of tariff policy will likely be decided at the November 2026 midterm elections. How voters who directly feel tariff costs at the pharmacy and grocery store cast their ballots could significantly alter trade policy direction from 2027 onward. If the triple burden of rising drug prices, manufacturing job losses, and consumer price pressures is reflected at the ballot box, substantial tariff policy revision becomes inevitable. Current polling shows healthcare costs rising as the number-two concern among likely midterm voters, up from fifth place a year ago. Conversely, if supply chain domestication produces visible results, the mandate for continuing current policy strengthens. Either way, what Liberation Day's one-year anniversary has demonstrated is clear: tariffs are no longer simple trade policy but have become geopolitical weapons reshaping the global economic order. The question is no longer whether this reshaping will happen, but how far and how fast it will go.

Sources / References

- Liberty Justice Center Marks One Year Since 'Liberation Day' Tariffs with Supreme Court Victory and $166 Billion in Refunds — Liberty Justice Center

- Liberation Day Was One Year Ago: Did the President's Tariff Promises Happen? — Tax Foundation

- Supreme Court Tariff Ruling: IEEPA Revenue and Potential Refunds — Penn Wharton Budget Model

- Fact Sheet: President Trump Bolsters National Security and Strengthens US Supply Chains by Imposing Tariffs on Patented Pharmaceutical Products — The White House

- Manufacturing Employment Data Confirm the Concentrated Benefits and Dispersed Costs of Trump's Tariffs — Cato Institute

- US Stocks Had a Remarkable 2025, But International Markets Did Much Better — CNN Business

- FX Outlook 2026: More Dollar Weakness Ahead — ABN AMRO

- A Year After 'Liberation Day,' Trump's Tariffs Will Never Be Legitimate Without a Vote in Congress — Reason

- Learning Resources, Inc. v. Trump — Opinion of the Court (24-1287) — Supreme Court of the United States

- Supreme Court Strikes Down Tariffs — SCOTUSblog

- Brookings Experts on the Supreme Court's Tariff Decision — Brookings Institution

- Employment Situation Summary — 2026 M02 Results — US Bureau of Labor Statistics

- State of Tariffs: February 21, 2026 — Yale Budget Lab

- FX Focus: G10 FX 2026 Outlook — In a Post-Peak USD World — MUFG Research

- Global Public Investor 2025 — OMFIF

- Currency Composition of Official Foreign Exchange Reserves (COFER) — Q3 2025 — International Monetary Fund

- KOSPI Tops Global Markets with World's Strongest Gains in 2025 — The Korea Herald

- Trump Administration Prepares 100% Tariffs on Some Imported Drugs — STAT News

- CBP's Tariff Refund Process Will Take Up to 45 Days to Deliver Returns — Supply Chain Dive

- A Year After 'Liberation Day,' Experts Review the Costs of Trump's Tariffs — Council on Foreign Relations

- Summary: Supreme Court Decision on IEEPA Tariffs — K&L Gates