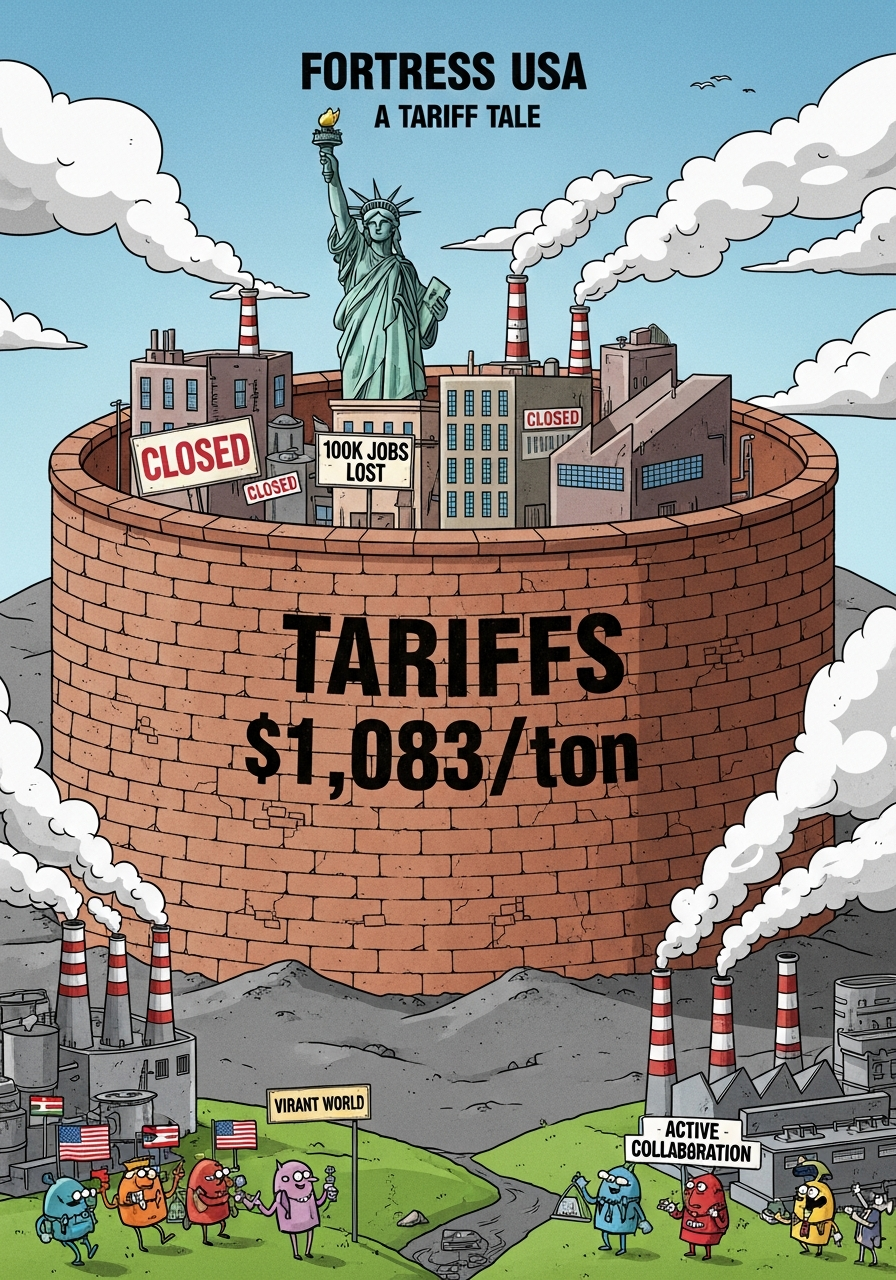

Trump Built a Great Wall of Tariffs — But It Was America Trapped Inside

Summary

America's reciprocal tariff policy has paradoxically accelerated a sweeping realignment of global trade. The EU-India FTA, uniting a $27 trillion market and two billion people, and the EU-MERCOSUR FTA have been finalized without American participation, shifting the center of gravity in the world economy. With U.S. hot-rolled steel prices hitting $1,000 per ton while the global benchmark sits at $472, and reshoring plans stalling at a 2% completion rate despite 81% of CEOs announcing them, the self-defeating nature of protectionism is laid bare.

Key Points

EU-India FTA — The Birth of the Largest Free Trade Zone in History

Finalized in January 2026, the EU-India FTA has created the world's largest free trade zone, encompassing a combined GDP of $27 trillion and a population of two billion people. The EU Trade Commissioner famously called it 'the mother of all deals,' and indeed it is: negotiations that had been deadlocked for nearly two decades suddenly accelerated once America's tariff wall gave both sides an urgent reason to close ranks. Under the agreement, EU exporters will see tariffs eliminated or reduced on 96.6% of goods, saving an estimated 4 billion euros annually in customs duties. India's automobile tariffs, currently at an effective rate of roughly 110%, will be phased down to 40% initially and eventually to 10% over a ten-year period, with a quota of 250,000 vehicles per year — a move that dramatically lowers the cost of entry for European automakers like BMW, Volkswagen, and Renault into one of the world's fastest-growing car markets. In return, India's IT services sector and generic pharmaceutical industry gain freer access to the EU's 450-million-consumer market, widening choices on both sides. The World Bank estimates that full implementation could add 0.1 to 0.2 percentage points to EU GDP and 0.6 to 1.0 percentage points to India's GDP by 2030 — modest individually, but collectively among the most significant bilateral trade impacts ever projected. Yet the true significance of this deal is geopolitical rather than purely economic: it is the first large-scale proof that the world can write its own trade rules in America's absence.

The Tariff Paradox — America Protected Costs, Not Competitiveness

U.S. hot-rolled steel now costs roughly $1,000 per ton, while the global export benchmark sits at $472 — meaning American manufacturers pay more than double what their overseas competitors pay for the same raw material. This gap widened sharply after Section 232 steel tariffs were raised from 25% to 50% on June 3, 2025, effectively pricing American industry out of global cost competitiveness. The steel premium cascades through every sector that uses it as an input: automobiles, construction, appliances, infrastructure. A single car now carries an estimated $1,500 to $2,000 in additional material costs attributable to tariffs alone. According to the Yale Budget Lab, the current tariff regime raises the average American household's annual consumer costs by $3,800 to $4,200 — a hidden tax that hits hardest at the bottom of the income ladder. For households in the lowest income decile, this burden represents roughly 6 to 8 percent of annual income, deepening inequality rather than relieving it. The deeper irony is that these inflated input costs are undermining the very export competitiveness that tariffs were supposed to restore. Products manufactured in America, built with tariff-inflated raw materials, increasingly cannot compete on price in global markets.

The Reshoring Myth Collapses — 81% Planned, 2% Delivered

A Boston Consulting Group survey of American CEOs reveals a stark gap between rhetoric and reality: 81% announced reshoring plans, but only 2% have actually completed them. In the meantime, U.S. manufacturing has shed over 100,000 jobs, and roughly 500,000 positions sit unfilled every month due to structural labor shortages. The obstacles are not abstract: land costs are prohibitive, environmental permits take years, and the average age of an American manufacturing worker has climbed past 44, with a quarter of the workforce over 55 and fewer than 8% under 25. Deloitte and the National Association of Manufacturers project that by 2033 the sector will need 3.8 million new workers, yet nearly 1.9 million of those positions risk going permanently unfilled. TSMC's Arizona fabrication plant, once held up as the flagship reshoring success story, initially experienced repeated schedule changes, though the company has recently accelerated its timeline, now targeting second-half 2027 for 3-nanometer production at its Phase 2 facility. The reshoring failure exposes a hard truth: the premise that tariffs alone could revive American manufacturing was always more political slogan than industrial strategy.

EU-MERCOSUR FTA — A Transatlantic Trade Axis Born Without America

Encompassing 31 nations and over 700 million consumers — the EU's 27 member states plus MERCOSUR's four (Brazil, Argentina, Uruguay, Paraguay) — this free trade zone represents the conclusion of negotiations that had been stalled for a quarter century. The agreement was formally signed on January 17, 2026, after EU Council approval by a 21-to-5 vote on January 9. All four MERCOSUR members have since completed ratification — Argentina on February 26, Uruguay on February 27, Brazil on March 4, and Paraguay on March 17 — with provisional application set to begin on May 1, 2026. Brazilian and Argentine beef, soybeans, and corn will enter the EU market with drastically reduced barriers, directly threatening the market share previously held by American agricultural exports. The USDA estimates that U.S. agricultural exports to the EU run at roughly $15 billion annually, of which 20 to 30 percent could be at risk.

American Isolation's Irony — Protectionism Became the Catalyst for Multilateral Trade

There is a deep historical irony in the fact that American isolationism has produced the opposite of its intended effect, galvanizing the rest of the world into tighter commercial bonds. Global investors have begun reassessing 'American exceptionalism,' and the signals are converging: the dollar index is trending weaker, with MUFG diagnosing a 'post-peak USD world' and forecasting a roughly 5% annual decline to the low-to-mid 90s on the DXY by year-end 2026. Euro- and yuan-denominated trade settlement volumes are rising. Foreign holdings of U.S. Treasuries are being trimmed. This is the most significant trade policy backlash since the Smoot-Hawley Tariff Act of 1930, which triggered retaliatory duties that collapsed global trade by 65%. But the response this time is fundamentally different: rather than retaliating tariff-for-tariff, the world has opted for a more sophisticated structural answer — 'let us trade among ourselves and leave America out.' Goldman Sachs has explicitly recommended diversification away from concentrated U.S. equities toward European and emerging market stocks. Once formed, these structures are extraordinarily difficult to reverse. Even if Washington were to rescind every tariff tomorrow, the $27 trillion contract has already been signed.

Positive & Negative Analysis

Positive Aspects

- Healthy Multipolarization of Global Trade

A system in which a single nation dictates world trade rules was inherently fragile. The emergence of the EU-India FTA and the EU-MERCOSUR FTA is shifting the axis of commerce from a North American unipolar model to a multipolar structure spanning Europe, Asia, and South America. This diversification structurally reduces the systemic risk that any one country's policy swings pose to global trade. Diversified trade dependency also serves as a buffer against complete supply chain collapse during geopolitical crises — a lesson painfully learned during the COVID-19 pandemic.

- Expanded Consumer Choice and Industrial Competitiveness for Two Billion People

As EU-India FTA tariff reductions take hold — with Indian automobile duties phasing down from an effective 110% to as low as 10% over a decade — European car brands gain dramatically cheaper access to one of the world's fastest-growing markets. In return, India's IT services and generic pharmaceuticals flow more freely into the EU's 450-million-consumer market. The World Bank projects full implementation could add 0.1 to 0.2 percentage points to EU GDP and 0.6 to 1.0 percentage points to India's GDP by 2030, with annual customs savings of roughly 4 billion euros. Goldman Sachs forecasts an 8% total return for the STOXX 600 in 2026. Two-way market opening creates a virtuous cycle of competition that naturally drives down consumer prices while expanding variety.

- Supply Chain Diversification with Institutional Backing Beyond China Dependency

The post-COVID consensus that China dependency must be reduced was broadly shared but difficult to act on without institutional architecture. The EU-India FTA provides that architecture, formally establishing India as a viable new manufacturing hub. Companies can now construct a 'China-Plus-India-Plus-EU Triangle,' moving beyond the simple 'China Plus One' formula to build tripartite supply chains spanning semiconductors, pharmaceutical ingredients, battery materials, and rare earths. India's GDP growth rate could accelerate from the current 6.5% to 7.5 or even 8%. BlackRock has issued a structural overweight recommendation for India, citing favorable demographics and secular growth potential.

- Enhanced Trade Access and Economic Self-Reliance for Developing Nations

Through the MERCOSUR FTA, Brazil, Argentina, and their partners gain tariff-free access to a market of 450 million EU consumers. All four MERCOSUR nations have completed ratification with provisional application set for May 1, 2026. Export diversification reduces South American dependence on the U.S. market, structurally strengthening economic self-reliance. This may prove to be a historic turning point in amplifying the economic voice of the Global South.

- New Trade Norms and Global Standards Elevation Through the 'Brussels Effect'

The EU has long maintained the world's most stringent regulatory standards in environmental protection, labor rights, and digital governance. Through these FTAs, those standards are being exported to India and MERCOSUR — the so-called 'Brussels Effect' — with the EU stepping into the role of de facto global trade norm-setter in America's absence. The linkage between the Carbon Border Adjustment Mechanism and trade norms could make a tangible contribution to reducing global carbon emissions. The inclusion of Amazon rainforest protection provisions in the EU-MERCOSUR FTA stands as a symbolic example of this next-generation approach.

Concerns

- Direct and Regressive Cost Burden on American Consumers and Businesses

The Yale Budget Lab estimates that if the current tariff regime persists, the average American household will face $3,800 to $4,200 in additional annual consumer costs. Steel alone carries a $600-per-ton premium, translating into $1,500 to $2,000 in extra costs per automobile. This functions as an invisible tax — one that is sharply regressive, weighing most heavily on lower-income households. For the bottom quintile, the burden amounts to roughly 6 to 8 percent of annual income, deepening domestic inequality.

- Inter-Bloc Technology Standards Fragmentation and the Risk of 'Tech Balkanization'

As the EU's GDPR and AI Act, China's indigenous technology standards, and India's data localization policies each evolve within their respective trade blocs, global companies face mounting compliance costs from maintaining parallel regulatory frameworks. Trade may liberalize within blocs even as technical friction between blocs intensifies — a paradoxical outcome. Technology standards fragmentation slows the pace of international research collaboration and innovation.

- Long-Term Structural Erosion of the Dollar's Reserve Currency Status

The U.S. dollar currently accounts for approximately 57.8% of global foreign exchange reserves — a share that has already slipped to 56.3% as of Q2 2025. The EU-India FTA includes active discussions on a euro-rupee direct settlement mechanism. Combined with BRICS alternative payment systems and the internationalization of the digital yuan, these developments could accelerate de-dollarization. MUFG projects the DXY falling to the low-to-mid 90s by end of 2026, representing roughly a 5% annual decline. Should the dollar's reserve share slide toward 45 to 48% by 2028, the cost of U.S. Treasury issuance rises and fiscal flexibility narrows.

- Prolonged Reshoring Failure and the Risk of a Stagflationary Trap

Tariffs raise the price of imported goods, but they do not automatically expand domestic production capacity. The stark reality of 81% of CEOs planning reshoring while only 2% have delivered demonstrates that American manufacturing infrastructure and labor markets are structurally unprepared. Prices rise while output stagnates: the textbook definition of a stagflationary trap. The 500,000 monthly unfilled manufacturing positions reflect a fundamental skilled-labor deficit. By 2033, the sector will need 3.8 million new workers, but nearly 1.9 million positions risk going permanently vacant.

- Weakened Security Alliances and Structural Escalation of Geopolitical Instability

Economic interdependence has traditionally served as a core mechanism for deterring interstate conflict. When America voluntarily severs its economic ties with major trading partners, its diplomatic leverage in times of crisis diminishes sharply. Retaliatory tariff disputes between the U.S. and EU are already cooling the broader diplomatic relationship, and the chill is beginning to seep into NATO burden-sharing discussions and security cooperation frameworks. This represents potentially the worst kind of own goal — paradoxically undermining the very national security that protectionism claimed to enhance.

Outlook

Let me start with what is likely to unfold over the next several months. In Q2 2026, detailed implementation negotiations for the EU-India FTA will intensify. The core agenda items are tariff reduction schedules for automobiles, pharmaceuticals, and digital services, along with mutual recognition of technical standards. There is a strong likelihood that the roadmap for phasing India's automobile tariffs from the current effective rate of roughly 110% down to 40% initially — and eventually to 10% over a decade, with annual quotas of 250,000 vehicles — will be formally agreed upon. The moment those details become public, European automakers' share prices will react. Expect a cascade of announcements from BMW, Volkswagen, and Renault as they fundamentally overhaul their India market strategies. The deal eliminates or reduces tariffs on 96.6% of EU export goods, with estimated annual customs savings of 4 billion euros, making this one of the most commercially significant FTAs ever negotiated.

Simultaneously, the risk of additional U.S. tariff escalation remains very much alive. The Trump administration has yet to issue a formal response to the EU-India FTA, but reports indicate that retaliatory measures against 'trade blocs that exclude America' are under active review. If the U.S. raises tariffs on EU goods from the current 20% to 30% or higher, the EU will impose countervailing duties on American agricultural products and energy — escalating the transatlantic trade conflict by another full notch. I put the probability of this scenario at 40 to 50 percent. Meanwhile, Section 232 steel tariffs were already doubled from 25% to 50% as of June 3, 2025, which is the primary driver behind U.S. hot-rolled steel prices hovering near $1,000 per ton against a global export benchmark of $472.

On the MERCOSUR side, the ratification picture is now nearly complete and remarkably concrete. All four MERCOSUR member states — Argentina (February 26), Uruguay (February 27), Brazil (March 4), and Paraguay (March 17) — have completed ratification, with provisional application set to begin on May 1, 2026. What had been a 25-year stalemate shattered in months, propelled by the shared external catalyst of American tariffs.

Looking six months to two years ahead, a much larger picture emerges. As the EU-India FTA's phased tariff reductions begin taking effect, a visible reconfiguration of global supply chains will materialize. The key development to watch is the emergence of what goes beyond the 'China Plus One' strategy — a 'China-Plus-India-Plus-EU Triangle' in which global manufacturers reduce China dependency by adopting India as a new production base while leveraging the EU for advanced technology and consumer markets. India's GDP growth rate could accelerate from 6.5% to 7.5 or even 8% during this period. BlackRock has issued a structural overweight recommendation for India, citing favorable demographics and secular growth potential that extends well beyond the AI narrative.

American domestic politics will reach a decisive inflection point during this window. As the November 2026 midterm elections approach, the real costs of tariff policy will become viscerally tangible to voters. According to Pew Research polling from February 2026, only 37% of Americans approve of tariff increases while 60% oppose them — a figure confirmed by ABC/Washington Post/Ipsos polling at 34% approval and 64% disapproval.

Financial markets will undergo a medium-term repricing of the 'American premium.' The S&P 500's forward price-to-earnings ratio currently stands at approximately 21 times, compared with roughly 15 times for European equities and about 20 times for India's Nifty 50. Goldman Sachs is forecasting an 8% total return for the STOXX 600 in 2026 and has explicitly recommended diversification away from expensive, highly concentrated U.S. equities.

Over the longer two-to-five-year horizon, this trade realignment is likely to be recorded as the structural turning point in the U.S.-centric global economic order that was built after Bretton Woods following World War II. The most fundamental long-term shift is the diversification of trade settlement currencies. With euro-rupee settlement mechanisms included in the EU-India FTA and BRICS nations developing their own payment systems, the dollar's share of global foreign exchange reserves — currently at 57.8% and already slipping to 56.3% as of Q2 2025 — could decline further toward 45 to 48% by 2028. MUFG has diagnosed a 'post-peak USD world,' projecting the DXY to fall to the low-to-mid 90s by end of 2026, representing roughly a 5% annual decline.

The fragmentation of global technology standards will also play out over the long term. As the EU's GDPR and AI Act, India's Digital Personal Data Protection Act, and China's data localization policies each become entrenched as standards within their respective trade blocs, 'Tech Balkanization' becomes reality.

The reshaping of energy trade is another long-term variable that should not be overlooked. The United States is currently the world's largest LNG exporter, and the EU has leaned heavily on American LNG to replace Russian gas. But as trade friction deepens, the EU has growing incentives to diversify its LNG imports toward Qatar, Australia, and Mozambique while simultaneously accelerating its renewable energy transition. Between 2028 and 2030, the EU's dependence on American LNG could fall from the current 45% to 25-30%.

The agricultural sector will also experience cascading effects. As the EU-MERCOSUR FTA allows Brazilian and Argentine beef, soybeans, and corn to enter the EU market with dramatically reduced barriers, the market share previously held by American agricultural products will be eroded. USDA estimates put annual U.S. agricultural exports to the EU at roughly $15 billion; 20 to 30 percent of that figure could be at risk.

Let me lay out the scenario framework. In the most optimistic bull scenario, the U.S. modifies its tariff policy following the 2026 midterm elections and belatedly seeks to join existing FTA frameworks. I assign this scenario a 25% probability.

In the base scenario, the current tariff regime persists for two or more years, and trade bloc fragmentation becomes entrenched. Global GDP growth falls 0.3 to 0.5 percentage points below current forecasts of 3.2%, with U.S. growth facing an additional 0.5 to 0.8 percentage point downward pressure. I assign this scenario a 50% probability.

In the worst-case bear scenario, the U.S. retaliates against the EU-India FTA by raising EU tariffs to 30% or above, and the EU counters with duties on American LNG and agricultural products, triggering a full-scale transatlantic trade war. This scenario brings global recession, a 15 to 20 percent DXY crash, and gold prices breaking through $3,500. I put the probability at 25%, but the impact if realized would rival the 2008 financial crisis.

Across all three scenarios, one common thread stands out: whether America maintains or withdraws its tariffs, the multipolar realignment already underway is extraordinarily difficult to reverse. The EU-India FTA — a $27 trillion contract — has been signed. The world has experienced what it looks like to function without America at the center.

Here are the specific indicators that readers should monitor closely. First, whether the Dollar Index (DXY) breaks below the 95 level. Second, whether the U.S. 10-year Treasury yield breaches 5%. Third, the number of countries ratifying the EU-India FTA. Fourth, tariff policy approval ratings — with Pew's latest reading at just 37% and falling. If three or more of these indicators move simultaneously, the door to the bear scenario swings open.

Sources / References

- EU-India Free Trade Agreement: Official Announcement — European Commission

- Mother of All Deals: How the India-EU Trade Deal Creates a $27 Trillion Market — Al Jazeera

- EU-MERCOSUR: Council Greenlights Signature of Trade Agreement — European Council

- Where We Stand: Fiscal, Economic, and Distributional Effects of All U.S. Tariffs — Yale Budget Lab

- CEO Survey: Reshoring Plans vs. Reality — 81% Planned, 2% Completed — Boston Consulting Group

- India-EU 'Mother of All Trade Deals': What to Know — World Economic Forum

- Americans Largely Disapprove of Trump's Tariff Increases — Pew Research Center

- Economic Growth Is Forecast to Drive a Modest Rise in European Equities — Goldman Sachs

- 2026 Global Macro Outlook: Beyond AI and Into Structural Growth — BlackRock

- Dollar Dominance Monitor: Tracking the Reserve Currency's Global Share — Atlantic Council

- G10 FX 2026 Outlook: In a Post-Peak USD World — MUFG Research

- U.S. Manufacturing Workforce: 3.8 Million Workers Needed by 2033 — Deloitte

- Global Steel Prices Rise in March 2026, Led by Europe and U.S. — IndexBox

- Steel Price Analysis: Understanding Current Market Dynamics and Section 232 Impact — Steel Industry News

- India-EU FTA: Some Challenges Ahead, But the Strategic Signal Is Clear — The Diplomat

- EU-MERCOSUR Trade Agreement: Preliminary Analysis of Agricultural Impact — USDA Foreign Agricultural Service

- EU-India Comprehensive Trade Agreement: Joint Statement — Press Information Bureau, Government of India