The SEC and CFTC Just Dropped a 68-Page Rulebook — What It Really Means When 16 Cryptocurrencies Are Declared 'Not Securities'

Summary

The SEC and CFTC jointly drew a line on the decade-long 'security or commodity' debate. Sixteen tokens are now digital commodities, but an interpretive release without Congressional approval cannot guarantee crypto's future.

Key Points

Historic Token Taxonomy Release

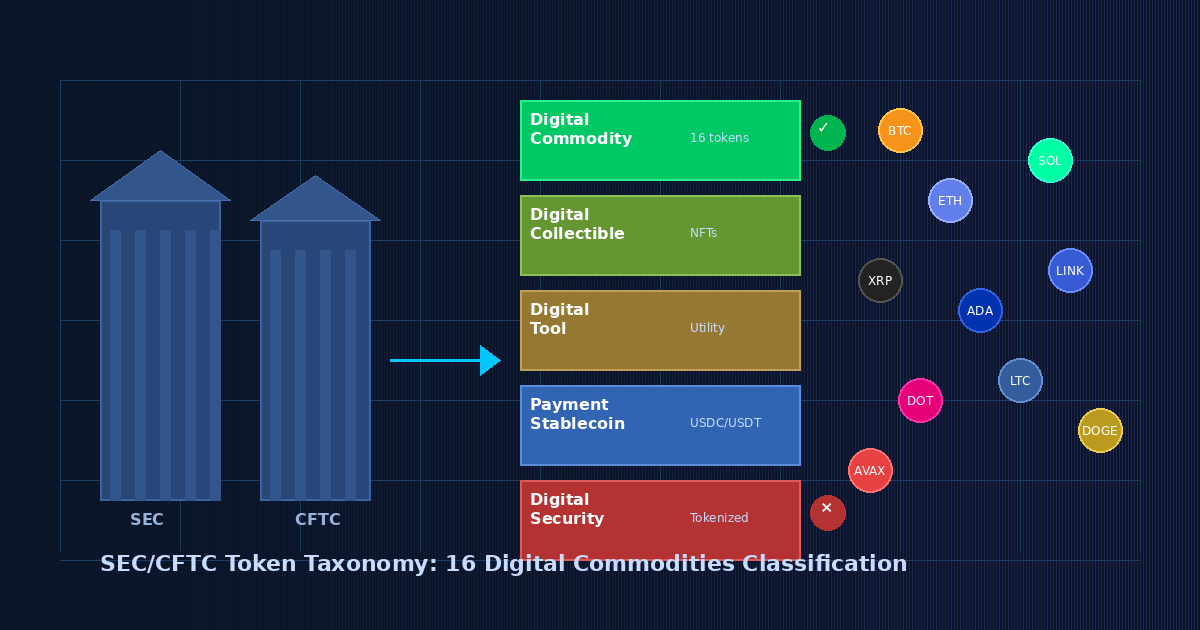

The SEC and CFTC published a 68-page joint interpretive release on March 17, 2026, classifying digital assets into five categories. Sixteen tokens including Bitcoin, Ethereum, Solana, and XRP were officially recognized as digital commodities, not securities. This provided the first official answer to a decade of regulatory uncertainty around the Howey Test. Protocol mining and staking were explicitly declared not to be securities transactions, providing legal comfort to the DeFi ecosystem. The 16 tokens now fall under CFTC jurisdiction, exempt from securities registration requirements.

From Gensler to Atkins — The SEC's Philosophical Shift

The SEC's regulatory philosophy fundamentally shifted from Gary Gensler's 'enforcement first, rules later' approach to Paul Atkins' 'rules first, enforcement only for fraud' approach. Under Gensler, fiscal year 2024 alone saw 583 enforcement actions and $8.2 billion in penalties, but after Atkins took office, formal investigative orders dropped 35% and no-action letters surged over 150%. Atkins publicly called his predecessor's approach 'a major missed opportunity' and introduced a principles-based approach requiring commission votes for all major enforcement actions.

Kraken's Fed Master Account — A Signal of TradFi-Crypto Convergence

On March 4, 2026, Kraken Financial became the first-ever digital asset bank to receive a Federal Reserve master account. This gives Kraken direct access to the Fedwire interbank payment network — processing trillions of dollars daily — without routing through intermediary banks. The Kansas City Fed approved an initial one-year limited account, and Kraken cannot earn interest on deposits or access Fed emergency lending. This approval is the culmination of Kraken's five-year application process and serves as a stepping stone for business expansion including a potential IPO.

Limits of Interpretation Without Law — CLARITY Act Risk

The Token Taxonomy is interpretive guidance, not legislation enacted by Congress. A future administration could reverse this interpretation, so the CLARITY Act must pass for legal permanence. The bill passed the House 294-134 but is deadlocked in the Senate over stablecoin yield disagreements. A Senate Banking Committee hearing is scheduled for late April, but whether it passes this year is uncertain. Democrats have raised concerns about DeFi's vulnerability to illicit actors.

Limited Market Response Amid Macro Headwinds

Despite the Token Taxonomy announcement, Bitcoin failed to breach $75,000 and the immediate market reaction was muted. The Iran war pushed Brent crude to $106 per barrel, the Fed held rates at 3.5-3.75%, and February PPI surged 0.7% — more than double the 0.3% estimate. The Strait of Hormuz closure stranded 3,000 ships, and the probability of no rate cut by year-end climbed to 41.5%. Regulatory tailwinds alone cannot overcome these macroeconomic headwinds.

Positive & Negative Analysis

Positive Aspects

- Dramatic lowering of institutional investment barriers

The digital commodity classification of 16 tokens eliminates legal risk for pension funds, insurance companies, and asset managers, vastly expanding the range of tokens eligible for portfolio inclusion. BlackRock's Ethereum ETF recording $15.5 million in day-one volume is the first signal. Applications for Solana, Cardano, and other altcoin ETFs are expected to follow.

- Fundamental transformation of the exchange industry

With 16 tokens exempt from securities registration requirements, they can trade freely on regulated platforms. This catalyzes development of new derivatives, custody services, futures, and options. Kraken's Fed master account symbolizes this trend.

- Legal reassurance for the DeFi ecosystem

Explicit confirmation that protocol mining, staking, airdrops, and wrapped tokens are not securities transactions substantially resolves legal uncertainty for DeFi developers. Previously, simply offering staking rewards could have constituted a securities law violation.

- U.S. reclaiming global crypto regulatory leadership

A signal that the U.S. is reasserting leadership in the regulatory competition against EU MiCA, Singapore, and Dubai. The clarity could attract back crypto capital and talent that fled overseas. The five-category classification system is likely to become the de facto global standard.

Concerns

- Limits of administrative interpretation without law

The Token Taxonomy is merely SEC/CFTC interpretive guidance, not Congressional legislation. It can be reversed by a future administration if the CLARITY Act does not pass. The bill is deadlocked in the Senate over stablecoin yield issues. Regulatory clarity without legal permanence is a castle built on sand.

- Inequality between 16 named tokens and the rest

The 16 explicitly named tokens enjoy a digital commodity premium while thousands of remaining tokens remain in a regulatory gray zone. Concerns about market polarization alongside lack of transparency in the inclusion/exclusion criteria.

- Weakened investor protection concerns

A 35% drop in enforcement actions and 150% surge in no-action letters could be negative for investor protection in a crypto market rife with fraud and manipulation. The focus only on genuine harm policy has unclear boundaries and may signal regulatory capture.

- Coincidence with macroeconomic headwinds

Iran war-driven oil surge (Brent $106), stagflation fears, and the Fed's hawkish stance are suppressing the market impact of regulatory tailwinds. Strait of Hormuz closure, PPI 0.7% surprise, and 41.5% probability of no rate cuts compound pressure on risk assets including crypto.

- Contradiction with decentralization philosophy

A paradox emerges where projects depend on central authority classification to receive digital commodity certification. Unclear timelines and criteria for new token projects to gain certification could lead the decentralization-born ecosystem to become subordinate to centralized certification systems.

Outlook

Looking at the short term — the next one to six months — the Token Taxonomy's impact will be gradual but structural. The most immediate change will be an expansion of institutional investment products. Bitcoin and Ethereum ETFs already exist, but we can expect a wave of ETF applications for Solana, Cardano, Polkadot, and others. New derivatives under CFTC jurisdiction — futures, options, swaps — could also be approved more easily. BlackRock's Ethereum ETF already recorded $15.5 million in day-one volume, and other asset managers will competitively launch products.

But the short-term price outlook is complicated. Bitcoin breaking $72,000 but failing to breach $75,000 shows that regulatory tailwinds alone can't overcome macroeconomic headwinds. The Iran war has pushed Brent crude to $106, the Fed expects just one rate cut this year, and 3,000 ships are stranded by the Strait of Hormuz closure. With the probability of no rate cut by year-end climbing to 41.5%, the crypto market will be caught in a tug-of-war between regulatory optimism and macroeconomic pessimism.

In the bull case, if the CLARITY Act passes this year, the Iran war concludes quickly, and the Fed cuts rates in the second half, this Token Taxonomy could trigger the largest crypto capital inflow since the 2017 ICO boom. The expansion of institutional investment in 16 tokens, the spread of digital asset banks like Kraken, and DeFi protocols returning to the U.S. mainland could combine to re-establish America as the undisputed center of the global crypto ecosystem. In this scenario, Bitcoin could break $100,000 by year-end.

In the base case — the most likely path — the taxonomy gradually transforms market structure while dramatic price rallies are constrained by macroeconomic conditions. The CLARITY Act may make partial progress but likely won't fully pass this year. Institutional investment products will expand, but the Iran war and stagflation fears will suppress risk appetite broadly. Bitcoin would trade in the $65,000-$85,000 range, while the altcoin market would experience polarization between the 16 taxonomy-premium tokens and the rest.

In the bear case, the CLARITY Act could die in the Senate, and a new administration in 2027 or 2028 could reverse the entire taxonomy. If Democrats win the next presidential election and revert to Gensler-era regulatory philosophy, the current interpretive guidance could become worthless. If the Iran war drags on and oil surpasses $150, all risk assets including crypto could face massive selloffs amid stagflation fears. In this scenario, Bitcoin could retreat below $50,000.

Over the medium term — six months to two years — the most important door this Token Taxonomy has opened is the full-scale convergence of traditional finance and crypto. Kraken receiving a Fed master account is just the beginning. Within two years, more crypto banks will gain Fed access, and traditional banks will begin offering digital commodity trading and custody services in earnest. Wall Street giants like Goldman Sachs and JPMorgan are already expanding their crypto trading desks, and this taxonomy will significantly accelerate that momentum.

In the long term — two to five years out — the deepest impact of this taxonomy will be on the formation of global crypto regulatory standards. The U.S. five-category classification system will likely become the de facto global standard. Europe's MiCA, South Korea's digital asset laws, and Japan's payment services regulations will converge toward the American framework. This will facilitate regulatory harmonization for cross-border crypto asset movements and elevate the maturity of the global crypto market.

However, the gap between "the named" and "the unnamed" created by the Token Taxonomy could become a structural problem for the crypto market in the long term. How long innovative new token projects must wait to receive "digital commodity" certification, and what criteria they must meet, remains unclear. If this ambiguity is not resolved, the crypto ecosystem — born from the spirit of decentralization — could paradoxically fall into a new form of centralization dependent on certification from central authorities.

Sources / References

- SEC Clarifies the Application of Federal Securities Laws to Crypto Assets — SEC

- CFTC Joins SEC to Clarify the Application of Federal Securities Laws to Crypto Assets — CFTC

- U.S SEC issues first-ever definitions for what crypto assets are securities — CoinDesk

- Kraken becomes first digital asset bank to receive a Federal Reserve master account — Kraken Blog

- Crypto Clarity Act may be cleared to move after senators agree on stablecoin yield — CoinDesk

- Why the Iran War and Higher Oil Prices Are Reviving US Stagflation Fears — Bloomberg

- Beyond Enforcement: The SEC's Shifting Playbook on Crypto Regulation — Georgetown Law