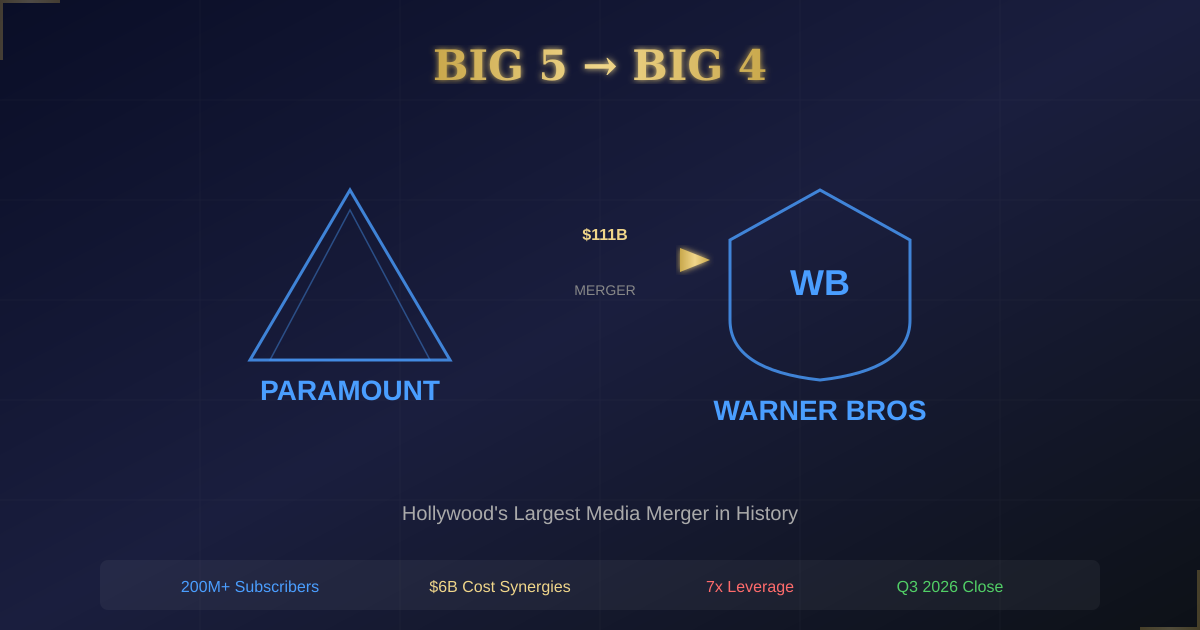

The Era of Hollywood's 'Big Five' Is Over — What the $111B Paramount-Warner Merger Actually Changes

Summary

Hollywood's Big Five studio system is shrinking to four for the first time in nearly a century. David Ellison's Paramount Skydance is acquiring Warner Bros Discovery for $111B in the largest media merger in history, and behind the blueprint of combining HBO Max with Paramount+, releasing 30 theatrical films annually, and cutting $6B in costs lies the fate of tens of thousands of jobs and the entire mid-budget film ecosystem.

Key Points

Birth of the Largest Media Merger in History

David Ellison's Paramount Skydance agreed to acquire Warner Bros Discovery for $31 per share, totaling $111B. This figure combines Warner's enterprise value of roughly $77B with its debt load, making it the largest leveraged buyout in history. The deal is expected to close in Q3 2026, with the combined entity operating in over 200 countries. Netflix itself attempted to acquire Warner but lost to Paramount, walking away with a $2.8B termination fee. Silicon Valley capital has now seized the most iconic studio in Hollywood.

Big 5 to Big 4 — A Once-in-a-Century Structural Shift

The number of major studios has been declining from eight in the 1930s. Disney's acquisition of Fox in 2019 reduced the count from six to five, and this merger now shrinks it from five to four. Fortune called it a transition not seen in nearly a century. Given that Disney controlled nearly 40% of the US box office after the Fox merger, the Paramount-Warner combination's market influence will be even more formidable. The Writers Guild of America formally opposed the merger, stating it would reduce the number of major buyers of scripted content and depress wages.

HBO Max + Paramount+ = 200 Million Subscriber Unified Platform

Paramount announced plans to merge HBO Max and Paramount+ into a single streaming service after deal completion. The combined platform would command roughly 200 million subscribers, instantly creating the world's second-largest streaming platform behind Netflix's 300+ million. Ellison stated HBO should stay HBO and promised to preserve Casey Bloys' independent operation. However, the execution complexity of integrating two premium networks, merging tech stacks, and aligning content strategies is enormous.

Behind the $6B Cost Savings — The Shadow of Mass Layoffs

Ellison declared $6B in cost savings while claiming most would come from non-labor areas such as vendor contract renegotiations and cloud infrastructure consolidation. Yet one Warner Bros executive told The Hollywood Reporter bluntly: We don't believe him. The Disney-Fox merger resulted in up to 4,000 layoffs, and the Teamsters union formally asked the DOJ to block the merger without enforceable job protection safeguards. With leverage at 7x EBITDA, achieving $6B in savings without significant workforce reductions is virtually impossible.

Death of Mid-Budget Films and Rise of A24/Neon

The merged mega-studio is expected to abandon the $20M-$50M mid-budget range in favor of nine-figure tentpoles. Hypebeast termed this the Blockbuster Bottleneck. Yet this void creates opportunities for boutique distributors like A24 and Neon. A24 already commands a $3.5B valuation, and Warner Bros itself launched a new contemporary film label staffed by Neon alumni. As mega-studios deepen franchise dependency, the indie space's creative freedom and market value paradoxically rise.

Positive & Negative Analysis

Positive Aspects

- Massive Streaming Competitiveness Boost

Combining HBO Max and Paramount+ creates the only competitor with the scale to challenge Netflix, with approximately 200 million subscribers. The combined IP portfolio including Game of Thrones, Mission Impossible, Harry Potter, Top Gun, and DC Universe creates unprecedented content diversity and subscription appeal on a single platform.

- Cost Efficiency and Economies of Scale

Consolidating duplicate tech infrastructure, vendor contracts, and cloud services enables $6B in cost savings. Integrating global distribution networks across 200+ countries can dramatically reduce marketing and distribution costs. Shared production facilities and post-production infrastructure further reduce production costs.

- HBO Brand Independence Promise

Ellison's commitment that HBO should stay HBO and his pledge to preserve Casey Bloys' independent operation is positive for maintaining premium content quality. HBO has written TV history from The Sopranos to Game of Thrones, and protecting this legacy would make it the combined platform's core differentiator.

- Global Local Content Production Expansion

The merged entity will operate a global network spanning cable, broadcast, and streaming across 200+ countries. This enables greater investment in local content production in each region, with potential to expand storytelling diversity globally. Combining Paramount's international channel network with WBD's Discovery brand strengthens non-English market strategies.

Concerns

- Mass Layoffs and Creative Ecosystem Contraction

The Disney-Fox merger precedent saw 4,000 layoffs, and workforce reductions are inevitable in a merger carrying $111B in debt. The Teamsters union asked the DOJ to block the merger, and The American Prospect called it a Hollywood Jobs Apocalypse. The WGA formally opposed it, stating that reducing major content buyers would depress wages and narrow creative opportunities.

- Leverage Ratio Risk

The leverage ratio stands at 7x EBITDA, with Netflix itself calling it the largest leveraged buyout in history. The $84B debt burden seriously threatens financial stability during economic downturns or subscriber churn. High debt servicing costs are likely to cannibalize content investment, creating a vicious cycle of quality decline.

- Mid-Budget Film and Diversity Crisis

The merged mega-studio's focus on tentpole blockbusters threatens to eliminate $20M-$50M theatrical mid-budget films. This reduces consistent theatrical content, shrinks opportunities for emerging directors and actors, and homogenizes audience taste. Fox 2000 Pictures was shut down entirely after the Disney-Fox merger.

- Regulatory Uncertainty and Global Antitrust Risk

While the DOJ cleared the HSR Act waiting period, a comprehensive antitrust investigation could extend into 2027. Multiple stakeholders including Teamsters, state attorneys general, and the WGA are opposing the deal. Senator Bernie Sanders issued an oligarchy warning. Regulatory delays or conditional approvals could postpone synergy realization.

- Integration Complexity and Culture Clash

Integrating two premium networks (HBO and Showtime), merging HBO Max and Paramount+ tech stacks, and coordinating 200-country distribution networks present massive execution challenges. A Warner Bros executive's assessment that Ellison didn't read the room reveals culture clashes have already begun. Historically, mega-media mergers from AOL-Time Warner to AT&T-WarnerMedia have frequently failed due to cultural incompatibility.

Outlook

Breaking down the aftermath of this merger into short-term, mid-term, and long-term horizons reveals dramatically different pictures at each stage. I believe this merger will reshape the entire entertainment industry's landscape, but I want to be equally clear that the process will be anything but smooth.

Short-term outlook (H2 2026 through H1 2027): If the merger closes on schedule in Q3 2026, the first thing that happens is organizational integration and workforce restructuring. Drawing from the Disney-Fox merger playbook, the first major round of layoffs will likely be announced within six months of deal closure. I estimate initial headcount reductions in the range of 5,000 to 8,000. The technical integration of HBO Max and Paramount+ will take a minimum of 12 to 18 months. I project 5% to 8% subscriber churn during the integration window, roughly 10 to 16 million users, with gradual recovery by late 2027.

Mid-term outlook (2027-2028): Once the unified platform stabilizes, a genuine duopoly with Netflix will emerge. By late 2027, I project the combined platform at 210 to 230 million subscribers versus Netflix's 350 to 380 million. The critical variable is ad-supported tier (AVOD) performance. A tiered pricing model combining HBO premium content with Paramount mass-market IP has potential to set ARPU 10-15% higher than Netflix. The most significant mid-term shift will be content production paradigm changes, with mid-budget theatrical films virtually vanishing from the major studio system. A24's valuation could surpass $5B by 2028.

Long-term outlook (2029-2031) splits into three scenarios. Bull Case (20-25% probability): Synergies materialize as planned, unified platform surpasses 250 million subscribers, streaming revenue exceeds $10B annually, leverage drops below 4x EBITDA, market cap reaches $200B-plus. Base Case (50-55% probability): Synergies partially materialize, subscribers plateau at 200-220 million, leverage hovers at 5-6x EBITDA, 15,000-20,000 jobs eliminated total, market cap lands at $120B-$150B. Bear Case (20-25% probability): Culture clashes and talent exodus prevent synergy realization, repeating AOL-Time Warner and AT&T-WarnerMedia precedents, market cap declines to $70B-$90B range.

Three key variables cut across all scenarios: AI penetration speed in entertainment, global regulatory environment evolution, and shifting consumer behavior including subscription fatigue. Ultimately, this merger is not simply a corporate transaction but a fork in the road for Hollywood's future, streaming's future, and the future of creative work itself.

Sources / References

- Paramount-Warner Bros Merger: Hollywood Wonders How Combo Will Pull Off 30 Theatrical Films A Year — Deadline

- How Paramount Beat Out Netflix, Won Warner Bros. and Will Change Hollywood Forever — Variety

- The Blockbuster Bottleneck: What the Paramount-Warner Bros. Merger Means for Hollywood Future — Hypebeast

- Paramount-Warner Would Create a Hollywood Jobs Apocalypse — The American Prospect

- Paramount to combine HBO Max and Paramount+ into one streaming service — CNBC

- Teamsters Union Says DOJ Must Block Paramount Warner Bros. Takeover — Variety

- Warner/Paramount sets up Hollywood to shrink from Big 5 to Big 4 — Fortune

- Paramount Victory Sparks Optimism and Concern From Global Players — Variety