Let's Be Honest About SKHY — You're Not Betting on SK Hynix, You're Betting on Nvidia

Summary

SK Hynix's $26.5 billion SKHY Nasdaq listing on July 10, 2026, broke Alibaba's 12-year-old record to become the largest-ever U.S. IPO by a non-American company, and the 7x oversubscription and 13% first-day surge signal that institutional investors view HBM as a structural growth story. The central tension: SKHY derives 40%-plus of HBM revenue from the Nvidia ecosystem, making it less a bet on a Korean memory chipmaker and more a multi-variable wager on Nvidia's GPU monopoly, Samsung's and Micron's HBM4 ramp timelines, and the duration of the AI capex cycle. A structural comparison to the 2000 fiber-optic boom reveals both overcapacity risks and the places where that analogy breaks down, since HBM's 12-to-16-layer die stacking technology imposes supply-side barriers commodity fiber never had. This analysis traces short-, medium-, and long-term trajectories with specific bull, base, and bear scenarios and key triggers for each phase. This content is for informational purposes only and does not constitute investment advice.

Key Points

The Record That Broke Records: Why $26.5B Changes Everything

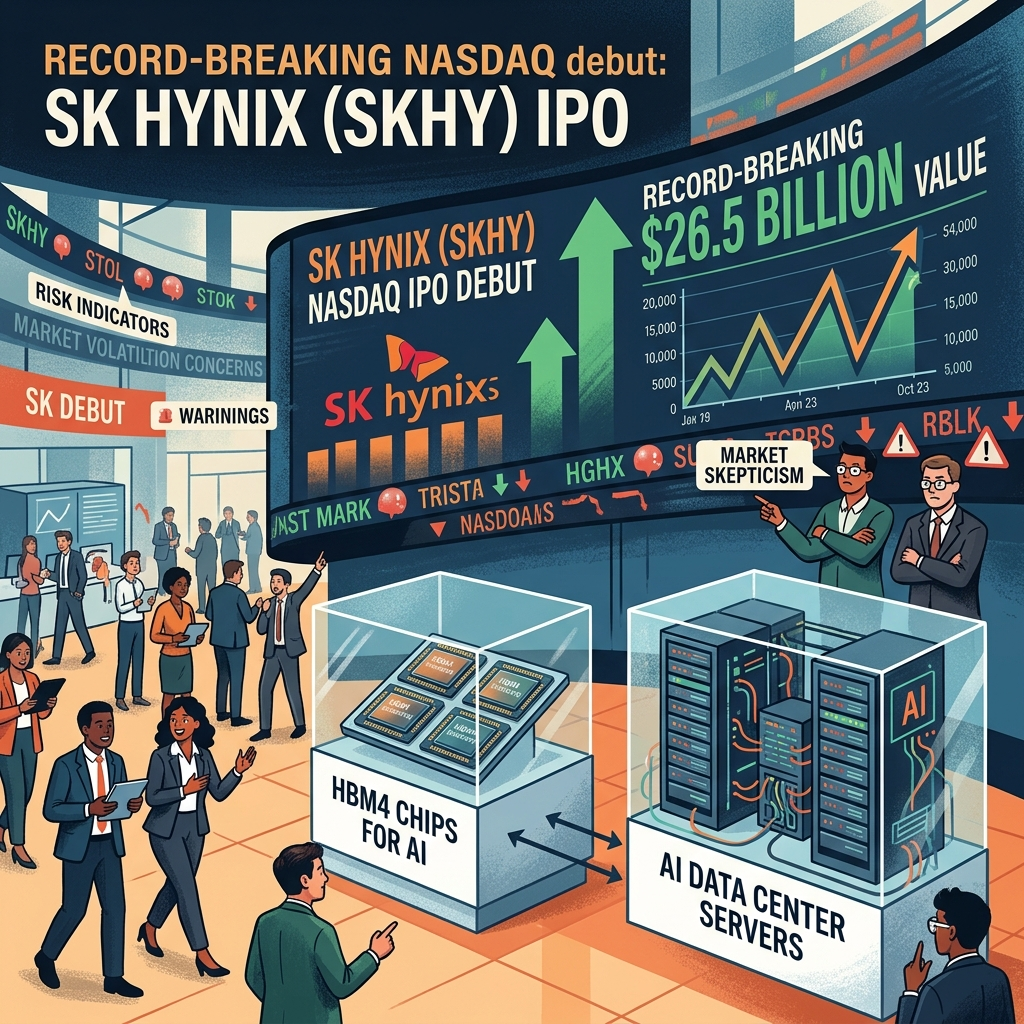

On July 10, 2026, SK Hynix's SKHY ticker debuted on the Nasdaq, raising $26.5 billion and shattering Alibaba's 2014 record of $25 billion — a record that had stood for over twelve years. The sheer scale is worth pausing on: this wasn't merely a large IPO, it was the largest-ever U.S. listing by any non-American company, full stop.

The mechanics of the listing revealed just how much institutional conviction existed going in. The offering was reportedly 7x oversubscribed, meaning demand for shares far exceeded supply, and the stock closed its first day up roughly 13% from the offer price. For a company of this market capitalization, that kind of first-day move reflects genuine momentum, not just retail enthusiasm.

What drives this conviction? SK Hynix controls an estimated 50%-plus market share in High Bandwidth Memory (HBM), the specialized chip architecture that Nvidia's H100, H200, and B200 GPUs depend on for the memory bandwidth needed in large-scale AI model training. HBM is not a commodity; it requires co-design partnerships, advanced packaging, and multi-year qualification cycles with customers.

The timing also matters. The listing comes as hyperscalers — Amazon, Microsoft, Google, Meta — are running multi-hundred-billion-dollar AI infrastructure buildouts that show no near-term sign of deceleration. SKHY is, in this framing, a direct financial claim on the AI capex supercycle.

The record-breaking size of this IPO is itself a signal: it reflects a market that believes the HBM growth story is structural and durable, not a passing wave. Whether that belief is warranted is the central question this analysis attempts to answer honestly.

The Nvidia Dependency Problem: Concentration Risk or Moat?

Here is the uncomfortable arithmetic that every potential SKHY investor needs to confront directly: SK Hynix derives an estimated 40%-plus of its HBM revenue from the Nvidia supply chain. In practical terms, this means SKHY's financial trajectory is closely tied to a single customer's procurement decisions, product roadmap, and competitive position.

This is not unusual for a semiconductor supplier — Intel suppliers faced similar concentration for decades, and TSMC has significant Apple revenue concentration — but it does mean that buying SKHY is not simply buying a diversified memory chipmaker. You are making an implicit bet that Nvidia's GPU dominance persists, that its data center revenue continues to compound, and that no architectural shift (custom silicon, photonics, alternative accelerators) disrupts HBM demand before SK Hynix can diversify its customer base.

The bull case for this dependency is that it's actually a moat. Nvidia's qualification and co-design process for HBM is lengthy and technically demanding. Switching suppliers mid-cycle is disruptive and costly. This creates a kind of enforced loyalty that, paradoxically, makes the revenue more predictable than spot-market memory sales.

The bear case is straightforward: Nvidia itself faces competition from AMD's MI-series GPUs, custom silicon from Google (TPUs), Amazon (Trainium), and Microsoft (Maia), and potentially from Chinese alternatives if export controls shift. Any scenario that reduces Nvidia's GPU market share reduces HBM demand at SK Hynix.

The honest framing is this: SKHY is not a diversified memory bet. It is a leveraged play on the Nvidia-AI-data-center complex, with all the upside and all the downside that implies.

The Fiber-Optic Analogy: Where It Holds and Where It Breaks Down

The comparison to the 2000 fiber-optic boom has been circulating in analyst circles since the SKHY IPO was announced, and it deserves a careful examination rather than either reflexive dismissal or uncritical acceptance.

The parallel that holds: during the late 1990s fiber boom, genuine demand for bandwidth was real — the internet was growing exponentially, and fiber was the right technology. What went wrong was supply. Corning, JDS Uniphase, and dozens of competitors built capacity so far ahead of the demand curve that when the telecom buildout slowed, they faced catastrophic overcapacity, margin collapse, and years of inventory digestion. The warning for HBM investors is that AI capex cycles can also slow — not because AI itself fails, but because hyperscalers pause, digest existing infrastructure, or find architectural alternatives.

Where the analogy breaks down: HBM is not fiber glass. The 12-to-16-layer die stacking, hybrid bonding, and thermal management engineering required to produce HBM4 and HBM4E are among the most technically demanding processes in semiconductor manufacturing. This creates genuine supply-side barriers. You cannot spin up an HBM fab in 18 months the way telecom companies leased dark fiber. Samsung and Micron are the only credible alternatives, and both are still behind SK Hynix on HBM3E and HBM4 yields.

The nuanced take: the risk is real but the timeline is slower than the fiber analogy suggests. An overcapacity scenario for HBM is more likely a 2028-2029 phenomenon — after Samsung and Micron complete their HBM4 ramps — than an imminent 2026 risk. Investors should monitor industry capacity announcements from both competitors as the primary leading indicator.

The honest conclusion: the fiber-optic analogy is a useful warning, not a definitive verdict. The supply barriers in HBM are structurally different, but the demand-concentration risk (one technology cycle, one dominant customer segment) rhymes uncomfortably with 1999.

Samsung and Micron's HBM4 Ramp: The Competitive Timeline

SK Hynix's current competitive advantage in HBM is real but time-limited. Samsung and Micron are both in active HBM4 qualification with major customers, and their ramp timelines will materially affect SK Hynix's pricing power and market share over the 2026-2029 window.

Samsung's trajectory is the more consequential variable. The company has the manufacturing scale, the DRAM expertise, and the customer relationships to mount a serious HBM challenge — but it has been plagued by yield issues on HBM3E that have delayed its competitive entry and forced Nvidia to qualify SK Hynix as a primary supplier. The key question is not whether Samsung will eventually match SK Hynix technically, but when. Current estimates suggest meaningful HBM4 volume from Samsung by late 2027, with market impact in 2028.

Micron is on a different trajectory — it has been more conservative about HBM capacity expansion, focusing on yield quality over volume. This makes Micron a less immediate competitive threat but also a potential beneficiary if the market encounters HBM supply disruptions that SK Hynix and Samsung cannot address.

For SKHY investors, the competitive timeline creates a specific window of analysis. The 2026-2027 period is likely characterized by continued SK Hynix pricing power and margin expansion as the dominant qualified HBM4 supplier. The 2028-2029 period is when Samsung's volume ramp creates genuine competitive pressure, potentially compressing SK Hynix's market share and ASP (average selling prices).

The implication for portfolio positioning: SKHY may be a stronger near-term (12-24 month) trade than a long-term (5-year) hold, depending on whether management successfully executes on customer diversification and next-generation technology development before Samsung narrows the gap.

Investment Scenarios: Bull, Base, and Bear Cases Through 2031

Rather than offering a single price target, the honest approach is to model the key variables across multiple scenarios and identify what each requires to be true.

Bull Case (2026-2031): The AI capex cycle extends longer than consensus expects, driven by agentic AI workloads, robotics, and autonomous systems that require continued GPU and HBM investment. SK Hynix successfully qualifies as a primary HBM4E supplier to Nvidia, AMD, and at least one hyperscaler custom silicon program. Samsung's HBM4 ramp encounters yield delays through 2028. SK Hynix diversifies beyond Nvidia to 60%-plus multi-customer HBM revenue. In this scenario, SKHY compounds at 15%-plus annually through 2031, and the IPO price looks like a bargain in retrospect.

Base Case (2026-2031): AI capex maintains current trajectory but faces a temporary deceleration in 2027-2028 as hyperscalers consolidate infrastructure spending. Samsung achieves competitive HBM4 yields by late 2027, gradually eroding SK Hynix's ASP premium. SK Hynix maintains 45%-50% HBM market share but sees margin compression from 40% to 30%-35% gross margins. The stock delivers moderate returns (7%-10% annually), roughly in line with a mature semiconductor cycle play.

Bear Case (2026-2031): A significant AI capex pause in 2027 (triggered by regulatory action, energy constraints, or a major LLM architectural shift reducing compute intensity) causes HBM demand to fall below supply capacity. Samsung and Micron complete their HBM4 ramps simultaneously, creating an overcapacity situation reminiscent of DRAM cycles past. SK Hynix's revenue concentration in Nvidia becomes a liability as Nvidia's own growth slows. In this scenario, SKHY underperforms the market by a significant margin, potentially revisiting IPO price levels by 2028-2029.

Key monitoring triggers that determine which scenario plays out: Nvidia's quarterly data center revenue trajectory, Samsung's HBM yield rate disclosures, hyperscaler capital expenditure guidance, and any announcements about architectural alternatives to HBM in next-generation AI systems.

Positive & Negative Analysis

Positive Aspects

- Structural AI Infrastructure Demand — This Is a Megatrend, Not a Memory Cycle

The demand dynamics driving HBM growth are fundamentally different from every prior memory supercycle in the industry's history, and that distinction has real consequences for how long the current tailwind lasts. Previous DRAM cycles — the 2018 supercycle, the 2021 pandemic surge — were driven by consumer electronics replacement cadences with three-to-four-year reversion patterns built into the structure. AI data center build-out, by contrast, requires constructing entirely new computing infrastructure from the ground up, with hyperscalers committing to three-to-five-year supply agreements rather than quarterly spot purchases. Google, Microsoft, Amazon, and Meta collectively project $725 billion in data center capex for 2026, a 77% year-over-year increase, with HBM procurement tied to contracted GPU server deployments rather than discretionary budgets. Gartner estimates HBM bit demand will grow eightfold between 2022 and 2027, from 123 million GB to 972 million GB, and SK Hynix's Q1 2026 result — revenue up 198% year-over-year at a 72% operating margin — is not a one-quarter aberration but the early expression of a structural demand inflection. The CEO's public statement that HBM supply is completely sold out for 2026 and that 2027 will be the worst supply shortage in the industry's history provides forward visibility that commodity DRAM cycles have never offered.

- HBM Technology Leadership and a Physical Manufacturing Moat

SK Hynix's position atop the HBM market is not the result of being first to file a patent — it is the accumulation of thousands of failed production runs, process refinements, and co-development cycles with TSMC's CoWoS packaging line that competitors cannot shortcut on any timeline that matters to near-term investors. HBM4 demands 12-to-16-layer die stacking, hybrid bonding at sub-micron precision, and thermal management that pushes the physical limits of 3D packaging, requiring tacit manufacturing knowledge that does not transfer through engineering hires or reverse-engineering programs. Samsung has been in serious HBM production for years and still trailed SK Hynix by six to 12 months on HBM4 yield entering 2026, and that gap is not cosmetic. The supply-chain ecosystem compounds this advantage: TSMC's CoWoS capacity expansion has been co-engineered around SK Hynix's memory die dimensions, meaning that a technically capable competitor faces an integration challenge that extends far beyond mere fabrication capability. UBS estimates SK Hynix will retain roughly 70% of the HBM4 allocation for Nvidia's Vera Rubin platform even after Samsung's ramp, implying that the world's leading chip buyer views SK Hynix's execution reliability as worth a significant supply concentration premium.

- The Nasdaq Listing Attacks the Korea Discount Directly

The Korea Discount — the persistent 20% to 30% P/E gap between equivalent Korean and U.S.-listed companies — has been one of the most discussed structural inefficiencies in emerging-market equity investing for decades, and the SKHY Nasdaq listing is the most direct assault on it that any Korean company has mounted. On the KRX, SK Hynix traded at a meaningful discount to Micron on identical earnings metrics, a reflection not of inferior fundamentals but of structural constraints including chaebol governance concerns, low dividend payout ratios, and limited accessibility for global passive capital. A Nasdaq listing changes the accessibility equation immediately, opening the door to Nasdaq 100 index inclusion, ETF passive flows, and the daily trading universe of every dollar-denominated portfolio in the world. All 37 analysts covering the stock at launch rated it a buy or hold, with 35 buy ratings and zero sells, and the average price target for KRX-listed shares implies nearly 50% upside — numbers that suggest the re-rating process has significant room to run. If SKHY establishes a successful track record over the next four to eight quarters, it becomes the reference case for potential ADR listings by Samsung Electronics, Hyundai Motor, and LG Energy Solution, potentially catalyzing broader Korea Discount compression across the entire market.

- SK Hynix Holds an Irreplaceable Position in the AI Chip Supply Chain

Every Nvidia H200, B200, and GB200 GPU that enters a data center does so with SK Hynix's HBM stacked directly beside the GPU die on a CoWoS interposer, and no substitute for HBM exists in high-performance AI inference or training workloads at scale. The bandwidth requirements of frontier AI models have grown at a pace that standard DDR5 DRAM cannot satisfy, and the physics of HBM's through-silicon via architecture — delivering terabytes per second of memory bandwidth at a fraction of the power per bit of conventional interfaces — make it structurally irreplaceable for the foreseeable GPU roadmap. This is not a niche product that a software workaround or architectural innovation can route around in the near term; it is the physical bottleneck that determines whether an AI chip achieves its rated throughput or sits partially idle. SK Hynix supplied 62% of global HBM shipments as of Q2 2025, a share that gives it genuine pricing authority in contract negotiations with the world's most valuable technology customers. HBM4 average selling prices run at five to eight times the equivalent DDR5 DRAM, and those premiums have held firm through a period of simultaneous multi-competitor production ramps — a strong signal about the depth of the demand advantage and the durability of the market position.

- Q1 2026 Fundamentals Are Extraordinary, Not Narrative-Driven

In a market crowded with AI-adjacent stocks trading on narrative and expectation, SK Hynix is one of the rare companies whose financials actually match — and arguably exceed — the premium the market has assigned. The Q1 2026 operating margin of 72% on 52.58 trillion won in revenue reflects the simultaneous tailwinds of HBM's 5x to 8x ASP premium over commodity DRAM, a supply-demand balance still tilted heavily in the seller's favor, and a production mix that has shifted rapidly toward high-value-add products. Management guidance for Q2 2026 implies operating profit of 60 trillion to 70 trillion won — a sequential increase that would mark the third consecutive record-breaking quarter if realized. SK Hynix also dethroned Samsung as the global DRAM market leader for the first time in 26 years, not by flooding the market with cheap commodity product but by capturing the highest-margin product tier and defending it with yield and technology advantages. The company's strategic choice to prioritize DDR5 general-purpose DRAM profitability alongside HBM means that even if HBM pricing faces temporary headwinds, earnings are supported by a second high-margin product line that provides a floor that a pure-play HBM bet would lack.

Concerns

- Single-Ecosystem Revenue Dependency — 40%-Plus of HBM Revenue Tied to One Ecosystem

There is no framing that makes a 40%-plus revenue dependency on a single customer ecosystem acceptable without a risk premium baked into the valuation, and investors who ignore this are accepting an asymmetric downside that their upside math does not account for. SK Hynix's HBM sales are disproportionately channeled through the Nvidia supply chain, meaning that any scenario in which Nvidia loses AI chip market share — whether to AMD, Google TPU, Amazon Trainium, or a future rival — creates a revenue impact that cannot be immediately redirected to alternative customers at equivalent pricing. Morgan Stanley estimates that Nvidia's share of SK Hynix's HBM procurement could decline from above 85% to 50% to 60% over time, which in absolute terms represents diversification, but the transition period is precisely where earnings surprises happen. If Nvidia's roadmap slips, if a platform transition creates a gap quarter, or if Nvidia begins internalizing memory design to reduce supplier dependency the way Apple internalized chipmaking, SK Hynix faces simultaneous volume and pricing pressure with limited short-term alternatives. Q1 2026 data shows a new non-Nvidia hyperscaler customer surpassing 10% of revenue for the first time — likely a custom ASIC program at Microsoft or Google — but that diversification is still in its early innings and cannot serve as a meaningful hedge against an acute Nvidia shock in the near term.

- Samsung and Micron's Technology Catch-Up Is a Ticking Margin Clock

SK Hynix's extraordinary HBM margins exist precisely because meaningful competition is limited, and that limitation has an expiration date that every informed investor should have marked on their calendar. Samsung began official HBM4 shipments to Nvidia in February 2026, ramped to full-scale supply in June 2026, and is projecting a 50% increase in HBM production capacity within the year, while Micron — having already overtaken Samsung in HBM market share for the first time — is targeting high-volume HBM4 production in 2026 and HBM4E by 2027 to 2028. The historical pattern in memory semiconductors is as reliable as it is brutal: once three suppliers achieve commercial-scale yields on the same product generation, average selling prices compress faster than annual analyst consensus models anticipate. Goldman Sachs explicitly flagged 2028 as the first year of material HBM ASP deceleration risk, and Bank of America, despite its Top Pick designation, included a 2028 pricing caution in its own research on the stock. The analog from Micron's post-dot-com experience is instructive: revenue fell from $7.3 billion to $4.0 billion to $2.6 billion over two fiscal years after the cycle turned, illustrating how quickly a memory company's earnings can compress once supply overcomes demand.

- The Memory Semiconductor Cycle Is Not Dead — It Has a Longer Wavelength, Not Zero Amplitude

The phrase "this time is different" has appeared in analyst research during every memory supercycle in the past 30 years, and it has been wrong every time — not because the demand was fake, but because the supply response eventually overwhelmed it. The 2018 DRAM supercycle drove SK Hynix's operating margin above 50%, then 2019 brought a greater-than-40% DRAM price collapse and margins compressed to single digits within a single year. The 2021 pandemic surge was met with simultaneous capacity expansions by all three major suppliers, and the 2022 to 2023 inventory correction was one of the worst pricing environments in the industry's history. SK Hynix, Samsung, and Micron are all investing aggressively in new HBM capacity: the M15X fab, Pyeongtaek P5 expansion, and Idaho and New York facilities are all slated to reach production scale between 2027 and 2029. The view that AI has permanently broken the memory cycle is an optimistic structural argument that has not been tested against a scenario where hyperscaler AI ROI disappoints and capex budgets reset at a lower level — and the more defensible position is that AI has extended the cycle's wavelength and raised its structural floor, not abolished the cycle itself.

- Geopolitical Risk and the U.S.-China Technology War Create Structural Tail Risk

SK Hynix is a South Korean company with significant production exposure at its Wuxi, China fab, and it operates in the most geopolitically contested sector of the global economy. U.S. export controls on advanced semiconductor manufacturing equipment and memory technology have tightened in consecutive rounds since 2022, and each escalation creates incremental risk to the production economics and supply-chain integrity of the Wuxi operations. A further tightening targeted at specific DRAM standards or at the CoWoS packaging ecosystem involving TSMC's Taiwan facilities could force production curtailments on timelines that management cannot plan around with the precision shareholders expect. The Taiwan Strait scenario is also structurally relevant: TSMC's CoWoS packaging lines, which are essential to assembling HBM alongside Nvidia's GPU dies, are concentrated in Taiwan, and any disruption there would freeze SK Hynix's HBM shipment capability regardless of what its Korean fabs produce. U.S. Commerce Secretary Howard Lutnick publicly pressed SK Hynix to commit to new U.S. fab construction as a condition of bilateral goodwill, illustrating how thoroughly this company's business decisions are entangled with policy-level geopolitics that no financial model can adequately price.

- $26.5B IPO Scale Creates a Lockup Expiration Overhang That Will Test Secondary-Market Liquidity

The flip side of the largest-ever foreign IPO in U.S. history is that the market has absorbed the largest-ever block of new Korean equity paper denominated in dollars, and the lockup expiration will test whether secondary liquidity can absorb what the primary market accepted with enthusiasm. SK Group's complex ownership structure — involving SK Telecom, SK Square, SK Inc., and various cross-holdings — means the pool of shareholders with potential motivation to monetize at lockup expiration is both large and somewhat opaque in its collective timing decisions. A stock with a three-to-six-month lockup that expires during risk-off conditions, or when an earnings miss generates momentum-based selling, can see declines that have nothing to do with the underlying business and everything to do with supply-demand imbalances in the trading market. SKHY is also a new ADR, meaning its institutional trading infrastructure — liquidity ecosystems, options market depth, ETF inclusion mechanics — is still being established, creating a period of elevated mechanical volatility. GraniteShares' 2x leveraged SKHY bull and bear vehicles launched simultaneously on July 13, 2026, and while they add trading volume, they also amplify intraday price swings in ways that can trigger stop-losses and margin calls during volatility episodes.

Outlook

Let me lay out my five-year view on SKHY across short, medium, and long-term horizons, with specific price ranges and probability estimates for each scenario. A forecast without probability weighting is just an opinion dressed up as a framework, and this investment deserves the full analytical treatment.

The near-term window — second half of 2026 through mid-2027 — is likely the most favorable period that exists in the foreseeable future for SKHY, and the publicly available data supports that assessment clearly. SK Hynix's CEO stated publicly that HBM supply is completely sold out for 2026 and that 2027 will represent the worst supply shortage in the memory industry's history, with contracted customer demand exceeding production capacity through the end of the decade under current projections. Nvidia's Vera Rubin platform is scheduled for ramp in the second half of 2026, adding another demand leg on top of an already sold-out production schedule. Goldman Sachs projects HBM pricing will continue growing 40% to 44% year-over-year through 2027, with no material price deceleration expected before 2028 at the earliest.

The near-term scenario breakdown is as follows. The bull case (probability: 25%) assumes Nvidia's Vera Rubin platform ships on or ahead of schedule, HBM4 demand runs 20%-plus above current quarterly run rates, and SKHY reaches $230 to $250 — a level that would put its market cap above Micron's current valuation. The base case (probability: 55%) assumes current growth momentum sustains at a gradually normalizing rate, with Q2 and Q3 2026 results modestly exceeding elevated consensus expectations, driving SKHY toward $190 to $210. The bear case (probability: 20%) involves a macro risk-off event, an AI capex fatigue signal from a major hyperscaler, or a damaging lockup expiration overhang, which could push SKHY to $120 to $135 — a 10% to 15% discount to the offer price. The lockup expiration timing, which creates mechanical supply in the trading market regardless of business fundamentals, is the key variable distinguishing the near-term bear from a deeper investment-thesis failure.

The medium-term — second half of 2027 through end of 2028 — is where the investment case for SKHY faces its most significant structural test, and the two decisive variables are Samsung's HBM4 production yield at full commercial scale and Micron's HBM4 volume ramp timeline. Samsung began HBM4 shipments to Nvidia in February 2026 and moved to full-scale supply in June 2026, but achieving the yields required at its planned 50% capacity expansion is a materially different challenge from qualifying the first batches. Micron's high-volume HBM4 production is scheduled for 2026, with HBM4E following in 2027 to 2028. When three suppliers reach commercial-scale yields on the same product generation simultaneously — and that alignment looks likely for early 2028 — buyer negotiating power reverses rapidly and average selling prices compress faster than the prior year's analyst consensus anticipated.

The medium-term base scenario (probability: 50%) sees SK Hynix defending its HBM market share at 50% to 60%, with HBM pricing normalizing from peak but not collapsing, while DDR5 general-purpose DRAM provides earnings floor stability. Revenue growth decelerates from 198% year-over-year to 60% to 80% by end-2027, and SKHY trades in the $200 to $250 range by end-2028. The medium-term bull scenario (probability: 25%) assumes AI agent workloads and enterprise AI adoption drive inference memory demand well beyond current projections, with Edge AI and on-device AI creating new HBM demand vectors that extend the growth runway beyond data centers — in this scenario SKHY could reach $300 or above. The medium-term bear (probability: 25%) assumes Samsung's HBM4 ramp is faster than expected, Nvidia actively diversifies its supply base, and SK Hynix's market share falls from 60%-plus to below 40%, driving SKHY to $130 to $160.

The long-term view — 2029 through 2031 — is where forecasting specific prices becomes an exercise in false precision, so the right approach is to define the structural scenario conditions rather than point estimates. Three variables dominate the long-term outcome. First, does AI's end market expand beyond data centers into Edge AI, on-device AI, and robotics at a pace that creates new HBM demand vectors beyond the GPU server context? Second, does SK Hynix maintain technology leadership at the next product generation — CXL memory, processing-in-memory, HBM5 and beyond — or does the competitive field equalize at the technology layer? Third, do geopolitical dynamics resolve in ways that are favorable or unfavorable for SK Hynix's supply-chain geography?

The long-term bull scenario envisions SK Hynix redefined from a memory supplier to an AI computing infrastructure provider, with product lines spanning HBM, CXL, and PIM architectures, and a diversified customer base across hyperscalers, edge OEMs, and automotive AI systems. In this scenario, SKHY reaches $400 to $500 — implying a fundamental reassessment of what memory semiconductor companies are worth when their products are integral to the most important technology platform of the decade. The long-term base scenario sees SK Hynix maintaining its cyclical leadership model — establishing a 12-to-18-month technology lead at each product generation, capturing the associated premium for that window, then ceding some margin as competitors close the gap before re-establishing the lead at the next generation — implying a SKHY range of $250 to $350 in 2029 to 2031.

The long-term bear scenario is the one that should focus risk-conscious investors. HBM overcapacity in the 2028 to 2030 window drives average selling prices down by 50% or more, SK Hynix's differentiation advantage is neutralized by Samsung and Micron at scale, and the company re-rates to a traditional commodity semiconductor multiple. In this scenario, SKHY could fall to $70 to $100 — below 70% of the IPO price. The analog from 2000 is instructive here: Corning's stock went from $113 to $1.10 — a 99% collapse driven not by fake demand but by overcapacity. In the early 2010s, TSMC's foundry dominance began its long compounding run as competitors essentially conceded the leading-edge race, giving TSMC 20 years of monopoly-like premium margins. SK Hynix's future almost certainly lies between these extremes. The technical entry barriers of HBM make a Corning-style collapse unlikely in the near term, while the presence of two well-funded, highly motivated competitors makes a TSMC-style permanent monopoly equally unrealistic. The most defensible long-term expectation is a series of leadership premium cycles, each lasting one to two product generations, with margin compression between them.

The second-order effects of this IPO on the broader Korean capital market ecosystem deserve a note. If SKHY delivers consistent quarterly results and builds a credible Nasdaq trading history over the next 12 to 18 months, it creates a reference case that directly lowers the perceived risk of ADR listings for other major Korean corporates. Samsung Electronics, Hyundai Motor, and LG Energy Solution — all of which have discussed or considered U.S. listing options — would have a concrete benchmark to point to in board discussions about the costs and benefits. Conversely, if SKHY underperforms expectations significantly in its first year of Nasdaq trading, it likely delays those conversations by years and reinforces the reluctance of Korean corporate boards to expose themselves to U.S. market scrutiny and shareholder activism.

My view on what could invalidate the base case needs to be stated explicitly. The most disruptive scenario is a sharp AI capex deceleration triggered by disappointing AI ROI metrics from the hyperscalers — if the major platforms conclude that revenue from AI infrastructure investments does not justify continued spending growth, capex budgets could reset within a single earnings cycle, and HBM demand could fall 20% to 30% in a quarter faster than any supplier can adjust production. The second invalidating scenario is Nvidia's potential move toward memory internalization — the way Apple's decision to design its own silicon cut Qualcomm's design win revenue by billions within two years. The third is a Chinese memory breakthrough from companies like CXMT, operating in a regulatory environment that prioritizes self-sufficiency in strategic semiconductors. Any of these scenarios would require fundamental reconsideration of the base-case thesis, which is exactly why tracking the Nvidia competitive landscape and the 2028 HBM ASP trajectory as primary monitoring signals — and setting 2028 as a formal portfolio review checkpoint — is the most practical guidance I can offer. This content is for informational purposes only and does not constitute investment advice.

Sources / References

- SK Hynix raises $26 billion in record US IPO on Nasdaq — Reuters

- SK Hynix IPO Becomes Largest Foreign Company Listing in U.S. History — Bloomberg

- SK Hynix's Nasdaq Debut Raises Questions About Nvidia Dependency — Wall Street Journal

- SK Hynix Bets on AI Memory Supercycle With Record Nasdaq IPO — Financial Times

- SK Hynix IPO: What HBM4 Competition Means for the Memory Market — TechCrunch

- HBM4 Market Share Analysis: SK Hynix Holds 50%+ Despite Samsung Ramp — Semiconductor Digest

- SK하이닉스 나스닥 상장 26.5조원 조달 성공, 외국기업 사상 최대 IPO — Korea Times