Meta Dropped $145 Billion on AI and Now Wants to Sell You the Leftovers — This Isn't a Strategy, It's a Confession

Summary

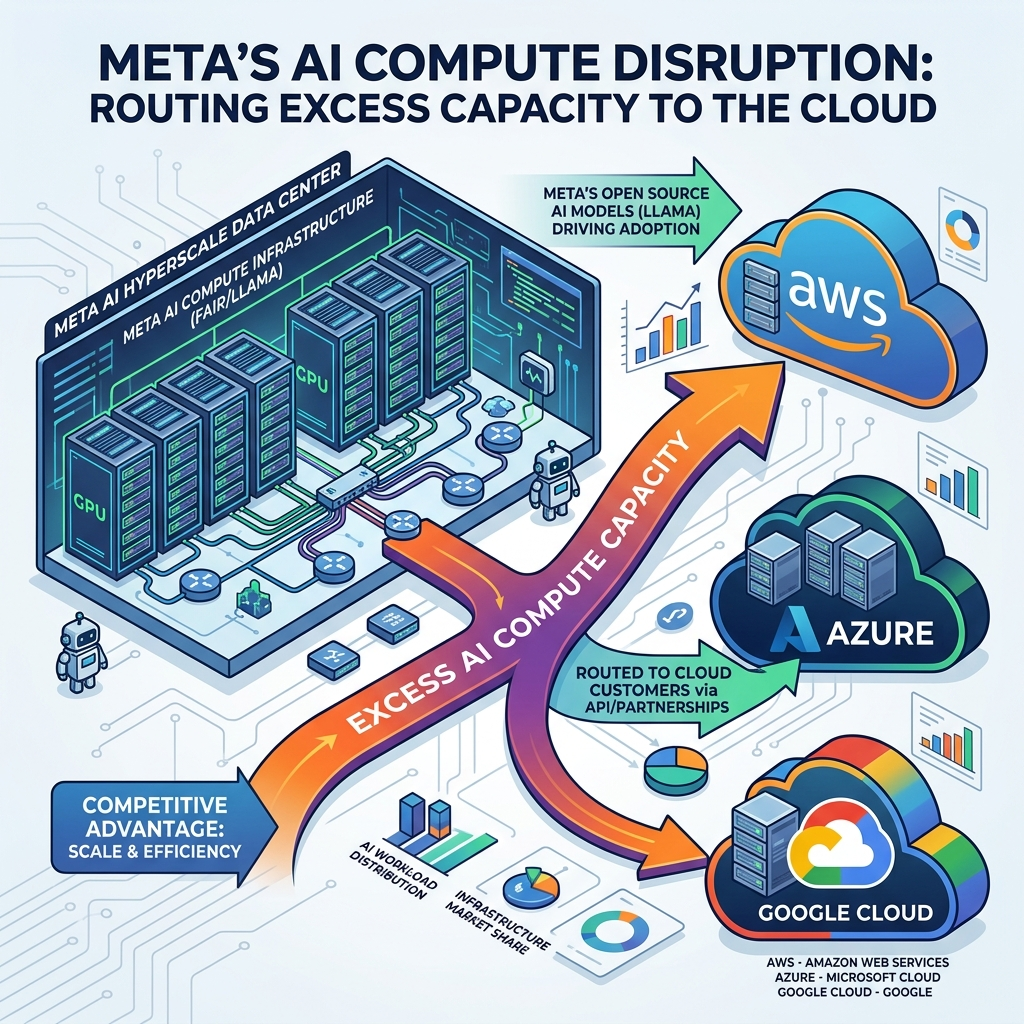

Meta Platforms has jolted Wall Street with the announcement of Meta Compute, a cloud services venture built on leasing out surplus GPU capacity from its AI infrastructure — a $125–$145 billion capital expenditure commitment for 2026 alone, nearly double the prior year's $72.2 billion. Bloomberg broke the story on July 1, 2026, and Meta's stock surged 9% on the day before giving back 5% two days later, a whipsaw that perfectly captured the market's conflicted feelings about whether the plan is actually executable. The venture would see Meta enter a cloud market controlled by AWS, Azure, and Google Cloud — three hyperscalers that collectively account for more than 65% of an $800 billion industry — by leasing GPU racks directly and offering API access to Meta's Muse Spark AI model. JPMorgan estimated that monetizing even 1GW of cloud capacity could generate $20 billion in annual revenue, a figure that convinced 43 of 55 covering analysts to maintain Strong Buy ratings with price targets raised to $825–$880. Whether Meta Compute proves to be a brilliant monetization of deliberate overbuilding or an inadvertent public admission that AI capital spending has spiraled beyond what internal demand can justify will be the defining investment question of the second half of 2026.

Key Points

Meta Compute's True Nature: An Unprecedented Monetization Experiment Born from Excess

Meta Compute is not a standard cloud market entry — it is an unprecedented public acknowledgment that $145 billion in AI infrastructure investment cannot be fully absorbed by internal demand, and that acknowledgment alone makes it historically significant regardless of the business outcome. Meta set its 2026 capital expenditure guidance at $125–$145 billion, up from $72.2 billion in 2025, making it the most aggressive single-year capex escalation among US Big Tech companies by a substantial margin. The fact that the company cannot fully utilize this infrastructure internally is precisely what created the business logic for Meta Compute in the first place — a company that had absorbed its own compute fully would have had no surplus to sell. Bloomberg's July 1 reporting revealed that Meta is structuring the offering around direct GPU rack leasing and API access to its proprietary Muse Spark AI model, targeting a market that is structurally different from the general-purpose compute sold by AWS or Azure. JPMorgan estimated $20 billion in annual revenue potential based on 1GW of cloud capacity, a figure that moved analyst consensus dramatically, with 43 of 55 covering analysts maintaining Strong Buy ratings at price targets of $825–$880. Whether this becomes a genuine revenue engine or primarily functions as a narrative shield for the capex criticism will be determined over the next 12–18 months of execution, and that gap represents the single largest source of uncertainty in the Meta investment thesis heading into 2027.

The Neo-Cloud Margin Crisis: Why CoreWeave Should Be More Worried Than AWS

The primary competitive threat from Meta Compute is almost certainly not aimed at AWS or Azure — it is aimed at AI-specialized neo-cloud providers like CoreWeave, Nebius, and Lambda Labs, whose entire business model is GPU leasing at a premium over general-purpose cloud rates. CoreWeave went public in 2025 at a market capitalization of $23 billion, built entirely on the premise that enterprises would pay a meaningful premium for AI-optimized GPU infrastructure delivered without the overhead of a general-purpose cloud provider. Meta's ability to cross-subsidize cloud pricing with advertising revenue exceeding $160 billion in 2025 gives it structural pricing power that neo-cloud competitors simply cannot match — when Meta offers GPU leasing at 20–30% below market rate while remaining profitable at the group level, companies like CoreWeave face a choice between unprofitable price matching and losing customers to a better-resourced competitor. The second-order effect compounds the pressure: Meta's entry into the GPU leasing market creates an informal secondary market that competes with NVIDIA's own DGX Cloud service, disrupting the premium pricing structure that neo-cloud providers have relied upon. This is the least-discussed but potentially most structurally significant consequence of the Meta Compute announcement — not the threat to AWS's market position, which is minimal, but the existential pressure on an entire cohort of publicly traded AI infrastructure companies that went public at premium valuations based on a business model Meta is now directly undercutting.

The Llama Ecosystem Moat: Why Meta's Cloud Entry Has a Card No Incumbent Can Copy

Meta's strongest competitive argument for Meta Compute is one that no incumbent cloud provider can easily replicate: the Llama open-source ecosystem that has accumulated the broadest developer community of any open-source AI model series, with tens of thousands of Llama-based applications deployed as of mid-2026. Developers who build on Llama and choose to host their applications on Meta Compute infrastructure gain native optimization advantages — lower latency, better fine-tuning efficiency, tighter integration with Meta's model serving stack — that AWS or Azure cannot easily provide for a competing model architecture. This creates a natural lock-in dynamic: once a Llama-native application is tuned and deployed on Meta Compute, migrating to a different cloud provider carries meaningful switching costs that did not exist when the code was first written. The flywheel logic is compelling: more Llama adoption drives more Meta Compute interest, which funds better Llama infrastructure, which makes Meta Compute more attractive for Llama workloads — a self-reinforcing cycle that gives Meta a customer acquisition channel priced near zero. However, the Llama ecosystem moat carries a structural paradox: the model's defining attribute is that it's open-source and designed to run anywhere, which simultaneously drives its explosive popularity and limits its ability to force users onto any particular infrastructure provider. Meta must offer meaningfully superior performance on its own cloud — not just availability — to convert Llama users into paying Meta Compute customers at sustainable margins.

The Psychology of a 9% Gap Up: What the Stock Surge Actually Revealed About Market Sentiment

The 9% single-session surge in Meta's stock on July 1, 2026 was not primarily a bet on cloud revenue projections — it was a relief trade on narrative resolution, and understanding that distinction is essential for investors evaluating the stock today. For months, the most persistent bear argument on Meta has been a version of: "This company is spending $145 billion on AI infrastructure in 2026 and there is no credible story for how that capital earns an acceptable return." Meta Compute, whatever its ultimate execution quality, is the first concrete and specific answer to that question — and the mere existence of an answer shifted market psychology in real time, which explains why a 9% move happened on an announcement with zero disclosed revenue, zero disclosed customers, and zero disclosed timeline. The 5% retracement that arrived two days later reflected harder questions resurfacing in analyst notes and investor conversations: Does Meta have the enterprise DNA to win cloud contracts against incumbents with decades of SLA track record? Will corporate CISOs allow sensitive operational data to be hosted by the company that generated the Cambridge Analytica scandal? That two-act market script — gap up on narrative, partial retracement on execution doubt — will almost certainly repeat itself on every major Meta Compute update over the next 12–18 months, making the announcement cadence and specificity as strategically important to the stock as the actual revenue numbers themselves.

The Training-to-Inference Inflection: The Technical Clock That Will Make or Break Meta Compute

The most consequential technical variable for Meta Compute's long-term success is one that rarely appears in financial media coverage but underpins the entire investment thesis: the timing of the AI industry's transition from training-dominated compute demand to inference-dominated compute demand. Today, the overwhelming majority of AI infrastructure investment — including the bulk of Meta's $145 billion capex program — is optimized for training, the massively parallel GPU workloads required to build and iterate on large language models from scratch. As these models mature and are deployed at scale for commercial applications, inference — running a trained model to generate real-time outputs for millions or billions of end users — becomes the dominant compute workload on a per-unit-time basis. The crossover point, when global AI inference demand exceeds training demand, likely arrives around mid-2027 based on current deployment trajectories, according to my analysis of current model deployment curves. Before that crossover, Meta's surplus GPUs are well-suited to the AI startups training their own models, providing a natural initial customer base. After it, Meta needs to demonstrate that its data center infrastructure can efficiently handle inference workloads at scale, which typically requires meaningfully different hardware configurations and software optimization than training cluster management. If Meta's infrastructure proves to be training-optimized and inference-inefficient, the surplus GPU narrative becomes structurally complicated at precisely the moment when the addressable cloud market is largest, most profitable, and most strategically important.

Positive & Negative Analysis

Positive Aspects

- Maximizing Utilization of the World's Largest Private AI Infrastructure

Meta is constructing what will be the world's largest privately owned AI infrastructure at $145 billion, and monetizing idle capacity from that buildout is rational capital management regardless of whether the broader cloud strategy ultimately succeeds. Data center fixed costs — power infrastructure, cooling systems, network connectivity, hardware depreciation — accrue whether or not the racks are running paying customer jobs, which means that idle compute is not a neutral outcome but a direct financial drag on capital returns. Leasing idle GPU time to external customers converts sunk fixed costs into incremental revenue with minimal additional capital expenditure, creating a financial structure that is difficult to argue against on pure accounting grounds even if the strategic vision of becoming the fourth hyperscaler proves optimistic. JPMorgan's estimate of $20 billion in annual revenue potential from 1GW of capacity sets the ceiling scenario, but even a fraction of that — say $4–$6 billion — would materially improve Meta's return on invested capital relative to the current scenario of running expensive infrastructure at below-optimal utilization rates. Beyond the direct revenue benefit, operating a public cloud offering at commercial scale forces internal discipline: it incentivizes Meta's infrastructure teams to improve the reliability, uptime, and efficiency metrics that benefit Meta's own internal AI workloads just as much as external customers.

- Natural Customer Conversion Through the Llama Open-Source Flywheel

The Llama model series has built the most extensive developer community of any open-source AI model family in 2026, and that community represents Meta Compute's lowest-cost customer acquisition channel — one that AWS, Azure, and Google Cloud cannot replicate without comparable open-source model ecosystems of their own. Developers already building applications on Llama 3 or Llama 4 are naturally inclined to evaluate Meta's native infrastructure first because the expected optimization benefits are real: tighter model integration, more efficient fine-tuning pipelines, and lower inference latency on hardware tuned for the model's architecture. This is structurally different from how the established hyperscalers grew their initial customer bases through aggressive pricing and broad service breadth, and it gives Meta a targeted wedge into the AI developer market that does not require head-to-head competition for traditional enterprise workloads. The flywheel dynamic is self-reinforcing in a way that compound advantages tend to be: more Llama adoption drives more Meta Compute interest, which funds better Llama infrastructure, which makes Meta Compute more attractive for Llama workloads, which drives more Llama adoption. Even if Meta Compute never wins a single Fortune 500 enterprise contract in the traditional cloud sense, the Llama-native developer market alone represents a meaningful, growing, and defensible revenue base.

- Founder-CEO Governance: The Long-Term Patience That Cloud Bets Require to Pay Off

Mark Zuckerberg's status as both founder and controlling shareholder gives Meta a structural advantage in executing a multi-year cloud strategy that virtually no other mega-cap technology company possesses in today's market. A professionally managed CEO facing quarterly earnings pressure from institutional shareholders would find it extremely difficult to sustain a cloud investment that produces below-average margins for two to three years while the customer base and enterprise trust are built from scratch. Zuckerberg can sustain that investment, because his dual-class share structure insulates long-term strategy from the quarterly pressure that drives most public company decision-making. His demonstrated willingness to accept sustained financial losses in the service of long-term strategic positioning is not hypothetical — he committed more than $36 billion to Reality Labs over several years when virtually every Wall Street analyst was recommending he abandon the metaverse investment program. The Reality Labs bet has underdelivered on its original vision, but the governance point is structural and independent of any single investment outcome: Meta is one of the few companies at this scale that can genuinely afford to play a five-year game in a market that rewards patience over quarterly optimization.

- Cross-Subsidy Firepower: Using Advertising Cash Flow as a Competitive Pricing Weapon

Meta's advertising business generated more than $90 billion in operating cash flow in 2025, and that capital base provides a cross-subsidy capability in cloud pricing that no pure-play cloud competitor — and arguably no neo-cloud competitor — can match on a sustained basis. When Meta can offer GPU leasing at 20–30% below market rate while remaining profitable at the group level because the shortfall is absorbed by advertising margins, competitors whose entire business model is GPU leasing face a structural problem they cannot price their way out of without destroying their own economics. This mirrors the strategy Amazon used to build AWS dominance in the early years — absorbing near-term losses in cloud services in exchange for market share that proved enormously and durably valuable over the subsequent decade. The crucial difference is that Meta's cash flow machine is proportionally even larger relative to its cloud ambitions than Amazon's e-commerce business was relative to its AWS investment in 2006, giving Meta more runway to sustain below-cost pricing before it needs cloud revenue to stand on its own. Even in the scenario where Meta Compute generates only $2–$3 billion in early revenue against $5–$8 billion in associated operating costs, the shortfall is easily absorbed without any dilutive capital raise, giving Meta the patience advantage that historically separates cloud market winners from early entrants who couldn't afford to wait.

Concerns

- Zero Enterprise DNA and the Cultural Mismatch That Capital Alone Cannot Fix

Meta has operated for twenty years as a consumer-facing social media and advertising company, and it has never had to earn enterprise trust in the rigorous, relationship-driven, compliance-intensive way that cloud infrastructure contracts demand. Enterprise cloud customers expect 99.99% uptime SLAs, 24/7 dedicated technical support, SOC 2 Type II, HIPAA, and FedRAMP security certifications, and a transparent audit trail for every interaction with their data — requirements that AWS has spent eighteen years building systems to satisfy and that Meta must construct from scratch. Beyond the operational infrastructure, the organizational culture required to maintain these standards is the opposite of Meta's foundational "move fast and break things" engineering ethos: enterprise cloud is methodical, process-driven, and reliability-obsessed by necessity, because downtime for a Fortune 500 customer is not a growth hack, it is a lawsuit. Building a genuine enterprise cloud capability from zero typically takes three to five years at minimum, and any large enterprise that makes a long-term infrastructure commitment to Meta Compute before that capability is proven is taking on operational risk that most corporate IT departments are specifically paid to avoid. AWS, Azure, and Google Cloud have not simply accumulated technical advantages over Meta — they have accumulated institutional credibility and contractual relationships that cannot be copied by an engineering team, however talented, starting from a standing start in 2026.

- The Cambridge Analytica Shadow: Trust Deficits That Persist Stubbornly in Enterprise Procurement

The Facebook-Cambridge Analytica scandal left lasting damage to Meta's institutional reputation for data security and third-party data stewardship, and enterprise cloud procurement is an environment where that kind of trust deficit creates real, measurable commercial barriers that cannot simply be engineered away. Corporate buyers — particularly in regulated industries like financial services, healthcare, and government — routinely subject cloud vendors to rigorous third-party security audits, and Meta's documented history with unauthorized third-party data access will generate questions in those audits that AWS and Azure are not required to answer. Meta currently operates under a Federal Trade Commission consent decree related to its data practices, a regulatory shadow that adds meaningful legal risk for any enterprise considering whether to entrust sensitive operational data, customer records, or intellectual property to Meta's infrastructure. Seeking Alpha analysis described this trust gap as "the largest invisible cost in Meta Compute's business model" — it cannot be quantified on a quarterly earnings call, but it directly affects sales cycle duration, enterprise conversion rate, and the types of workloads that potential customers are willing to migrate to Meta's servers. Even if Meta's cloud infrastructure is technically flawless and security-certified from day one, the reputational overhang will slow enterprise adoption in a way that cannot be resolved by marketing spend or engineering excellence, because institutional memory in corporate IT departments is long and procurement risk aversion is structural.

- Margin Dilution and the Hidden Risk of Valuation Re-Rating

CNBC reported that Wall Street analysts are already circulating serious concerns about Meta Compute diluting Meta's overall margin profile, and this represents an underappreciated structural risk to the stock's premium earnings multiple that could punish investors even in an execution success scenario. Meta's advertising business operates at 35–40% operating margins, a level that justifies the premium multiple the stock commands relative to more diversified technology conglomerates. The cloud business is likely to land in the 10–15% operating margin range in its early years, and potentially below 10% if aggressive pricing is required to win initial market share from entrenched competitors. If Meta Compute grows to represent 10% or more of total revenue — a reasonable expectation within two to three years if the bull case is even partially correct — the blended margin profile degrades in ways that analytically justify a lower price-to-earnings multiple, even as absolute revenue and earnings dollars grow. This creates a potential "growth penalty" scenario: a company whose stock underperforms expectations despite improving business fundamentals because the market re-rates the quality of those fundamentals downward. The risk is compounded by Reality Labs' ongoing operating losses of more than $10 billion annually; investors who reluctantly accepted margin compression from one experimental business line may be structurally less patient with a second one compressing margins simultaneously, particularly if Meta Compute's revenue ramp is slower than the $20 billion JPMorgan ceiling implied.

- Structural Demand Risk: What Happens When the AI Investment Cycle Eventually Turns

Meta Compute's entire business model rests on the assumption that demand for AI compute will continue growing at the rates projected by the most bullish infrastructure forecasts, but this assumption is not guaranteed, and the historical pattern of technology investment cycles provides structural reasons for caution that the current market euphoria tends to suppress. The current AI infrastructure investment wave shares characteristics with previous technology capital expenditure cycles that ended in painful correction: massive coordinated capital commitment from multiple large companies simultaneously, demand projections based on extrapolating the steepest part of the adoption curve, and monetization timelines that keep shifting outward as each quarterly earnings cycle reveals that enterprise adoption is slower than the infrastructure buildout. If enterprise adoption of generative AI fails to deliver the productivity improvements that justify the current investment pace — if the "AI productivity revolution" proves more modest and slower-moving than the consensus narrative assumes — demand for GPU compute could contract substantially from 2027 onward, with consequences across the entire AI infrastructure stack. In that scenario, Meta's surplus GPU inventory becomes genuinely surplus in the worst sense: the external leasing market evaporates, the $145 billion capex program produces minimal financial return, and Meta Compute becomes a liability in the investment narrative rather than the shield it was designed to be. The probability of this outcome is not the highest in my scenario distribution, but it is meaningfully above zero, and investors who are not stress-testing their META positions against an AI demand slowdown are underweighting a risk that the market's initial 9% surge made psychologically easy to dismiss.

Outlook

The next six months represent a genuinely decisive period for Meta's narrative trajectory. The Q2 earnings call, expected around July 30, is the first real opportunity for Zuckerberg to put hard numbers and timelines on the Meta Compute announcement. I expect him to announce that hundreds of companies are already in the pipeline for initial onboarding — and the critical question is whether those companies are Fortune 500 enterprises or AI startup co-tenants. That distinction matters enormously for how the market prices the update. If even three to five large enterprise names are disclosed as early customers — a tier-1 financial institution, a major healthcare company, a logistics conglomerate — Meta's stock has room to run another 10–15% from its current $580–$610 range. If the pipeline turns out to be populated primarily by AI startups and Llama-adjacent developers, the market will correctly conclude that Meta Compute is operating in the same competitive tier as CoreWeave rather than AWS, and a meaningful pullback is likely. The Q2 call is the catalyst most likely to break the current trading range decisively in one direction or the other, and positioning ahead of it should account for the full range of outcomes.

Beyond Meta's individual earnings, there's a broader macro signal embedded in this announcement that deserves careful monitoring. The moment Meta publicly acknowledged having surplus GPU capacity, it implicitly opened a door for other hyperscalers to make similar disclosures. If Google announces it's leasing out surplus TPU capacity, or if Amazon expands external access to its proprietary Trainium chips, the combined effect would be a clear industry-wide signal that AI infrastructure investment has overshot near-term demand. Conversely, if Microsoft, Google, and Amazon hold the line and continue projecting that their internal AI demand is capacity-constrained, Meta's surplus framing becomes an outlier rather than a harbinger. I expect at least one additional hyperscaler to make a surplus-capacity-adjacent announcement before Q3 ends, and when that happens it will accelerate the AI overbuild debate from a financial media storyline to a market-moving thesis. NVIDIA's GTC conference and the major developer events in H2 2026 are the key stages to watch — if the word "surplus" appears even once more across those events, market concern about AI infrastructure overcapacity will escalate quickly.

Looking out to 2027, I see three distinct scenarios with meaningfully different probability weightings. In the bull case, which I assign a 25% probability, Meta Compute achieves $10–$15 billion in annual revenue within 24 months, driven by a combination of Llama ecosystem developers, mid-market enterprise clients, and sovereign AI programs in markets where AWS and Azure have lighter footprints. This scenario requires Meta to secure at least three to five large enterprise anchor clients that lend credibility to the SLA story, and it requires Llama 4 and its successors to maintain competitive performance against GPT, Claude, and Gemini. If these conditions hold, Meta's valuation story re-rates from "high-margin advertising platform" to "advertising plus AI infrastructure conglomerate," opening a path to a $2 trillion market capitalization. The primary reason I'm not higher on this probability is that building enterprise trust from a cold start typically takes three to five years, not twelve months, and the clock started only in July 2026.

The base case, which I weight at 50%, sees Meta Compute generating $3–$5 billion in annual revenue by end of 2027 — modest in absolute terms but strategically significant in narrative terms. At this revenue level, Meta Compute is not the fourth hyperscaler. But it is proof-of-concept revenue that neutralizes the "$145 billion black hole" narrative. In this scenario, Meta focuses commercial efforts on the Llama ecosystem — AI startups, open-source developers, academic research institutions — rather than competing head-to-head with AWS for traditional enterprise workloads. The margin profile of this revenue will be materially lower than Meta's advertising margins, probably 15–20% versus the 35–40% the advertising business generates, creating a mild but real earnings quality drag that analytical bears will use persistently. However, the stock stabilizes in the $650–$720 range because the capex criticism is neutralized. In this base scenario, Meta Compute functions less as a standalone business and more as a strategic insurance policy — a card Zuckerberg can play in any quarter where advertising growth softens.

The bear scenario — which I weight at 25% — unfolds through one of three pathways: enterprise customer acquisition stalls due to Meta's data privacy reputation, the AI investment cycle cools faster than expected and GPU demand contracts, or a significant security incident involving Meta's cloud infrastructure poisons the well for enterprise adoption. In any of these pathways, Meta Compute becomes effectively dormant as a business driver within 18–24 months. If that happens, the $145 billion capex question returns to the foreground with no narrative shield, and analysts are forced to model Meta purely as an advertising company that massively overcapitalized. In that framing, the stock likely revisits the $450–$500 range. The bear scenario is not my base case, but it is a real possibility. The Cambridge Analytica scandal, while years old, left permanent scar tissue in enterprise procurement departments, and there is no quick technical fix for institutional memory. Investors who are not stress-testing their Meta positions against this scenario are underweighting a risk that the market's initial 9% surge made easy to dismiss.

The most important technical variable governing Meta Compute's medium-term success is a question that receives almost no attention in financial media, but it underpins everything: when does global AI inference demand exceed AI training demand? Right now, the overwhelming majority of AI infrastructure investment — including the bulk of Meta's $145 billion program — is optimized for training, the massively parallel GPU workloads required to build and iterate on large language models from scratch. As these models mature and are deployed at scale for commercial applications, inference — running a trained model to generate real-time outputs for millions or billions of end users — becomes the dominant compute workload on a per-unit-time basis. The crossover point, when global AI inference demand exceeds training demand, likely arrives around mid-2027 based on current deployment trajectories, according to my analysis of current model deployment curves. Before that crossover, Meta's surplus GPUs are well-suited to the AI startups training their own models, providing a natural initial customer base. After it, Meta needs to demonstrate that its data center infrastructure can efficiently handle inference workloads at scale, which typically requires meaningfully different hardware configurations and software optimization than training cluster management. If Meta's infrastructure proves to be training-optimized and inference-inefficient, the surplus GPU narrative becomes structurally complicated at precisely the moment when the addressable cloud market is largest, most profitable, and most strategically important.

Looking as far as 2028–2030, I believe the cloud market bifurcates into general-purpose and AI-specialized segments, and Meta's best-case trajectory runs squarely through the second category. In the general-purpose segment, the AWS-Azure-Google Cloud oligopoly will be essentially unassailable — their distribution advantages, compliance ecosystems, and enterprise relationships are not replicable in a five-year window. But in AI-specialized cloud — inference infrastructure for large-scale generative AI applications — Meta and its Llama ecosystem have a credible path to 15–25% market share. If the global AI inference cloud market reaches $300–$500 billion by 2030, Meta's addressable share represents $45–$125 billion in annual revenue. That revenue base, layered on top of a still-dominant $160 billion-plus advertising business, puts a $3 trillion market capitalization in the realm of the plausible. This is the genuine long-term upside scenario, but it rests on three premises that are each uncertain: AI delivers the productivity transformation it has been promising since 2023; the regulatory environment in the US and EU remains permissive enough for Meta to operate integrated social-media-plus-cloud infrastructure; and NVIDIA's GPU dominance does not erode so fast that Meta's GPU-based compute fleet becomes competitively obsolete before the inference market matures.

The cascade effects from Meta Compute's market entry deserve tracking separately from Meta's own financial performance. The first-order effect is margin compression at neo-cloud providers — CoreWeave, Nebius, Lambda Labs — who cannot match Meta's cross-subsidy from advertising revenue. The second-order effect touches NVIDIA: Meta leasing out its GPUs creates an informal secondary market that competes with NVIDIA's own DGX Cloud service and direct enterprise GPU relationships. The third-order effect is actually positive for the broader AI startup ecosystem — if GPU leasing prices fall 20–30% as a result of Meta's entry, compute cost barriers for AI development decrease, enabling a new cohort of well-capitalized startups to build at scale without raising as much venture funding. For investors with existing exposure to Meta, a staged approach tied to three specific checkpoints makes more sense than binary positioning: the Q2 earnings disclosure of the Meta Compute launch timeline and initial customer pipeline; the first reported quarterly revenue from the cloud segment expected in Q4 2026; and the quality of enterprise clients disclosed by Q1 2027. Incrementally adjusting position size at each checkpoint — increasing if milestones are met, reducing if they disappoint — is more rational than either embracing the JPMorgan bull ceiling as the base case or dismissing the announcement as investor relations theater. This analysis is provided for informational purposes, and all investment decisions must reflect individual risk tolerance and financial circumstances.

Sources / References

- Bloomberg's First Report on Meta Compute's Internal Organization Launch — Bloomberg

- Meta's Stock Surges 9% on the Day of the Meta Compute Announcement — CNBC

- Wall Street Excitement Over Meta's Cloud Push Tempered by Margin Concerns — CNBC

- Zuckerberg's Long-Term Strategic Vision and the Meta Cloud Investment Case — Motley Fool

- Technical Assessment of Meta's GPU Leasing Business Model — Tom's Hardware

- Meta Compute as Evidence of AI Bubble Excess: A Contrarian Analysis — Seeking Alpha

- AWS, Azure, and Google Cloud Face a New Rival as Meta Enters Enterprise Cloud — 24/7 Wall Street