It Wasn't Smart AI That Took the Jobs. It Was a Clumsy Robot That Keeps Calling in Sick.

Summary

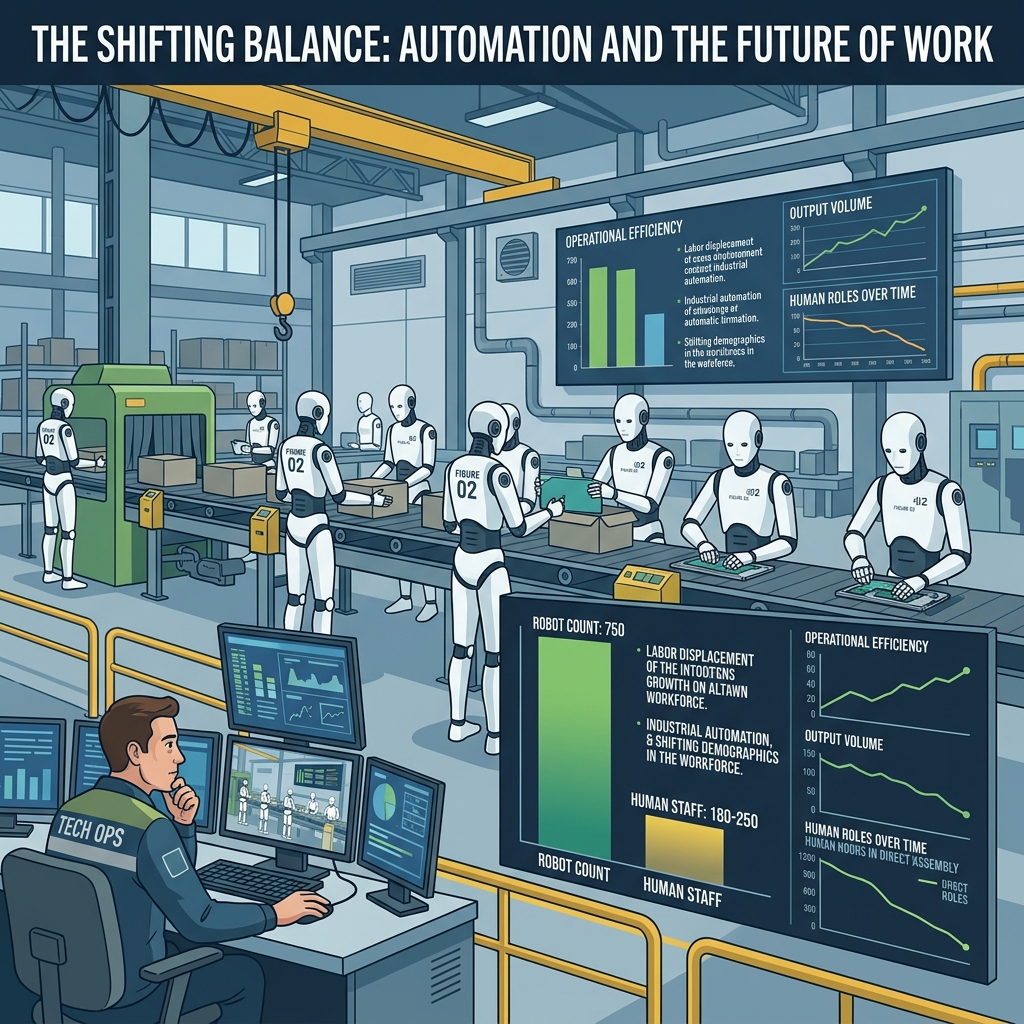

On June 20, 2026, a single chart posted by Figure AI CEO Brett Adcock showing 750 robots outnumbering an estimated 180 to 250 human employees for the first time was widely consumed as a symbolic turning point for the humanoid robotics industry. Yet half of that crossover stems not from an explosion in robot deployment but from four years of nearly flat human hiring, a purely arithmetic fact that reframes the entire narrative once it is stated plainly. Concurrent shop-floor reporting from Chinese factories describes humanoid robots operating at only 20 to 30 percent of human efficiency and suffering mass equipment "sick leave" after failing to adapt to factory environments, even as more than 30 billion yuan poured into this low-efficiency hardware category in the first quarter of 2026 alone. This contradiction indicates that the true trigger for labor substitution is not robotic competence but a cost structure built on round-the-clock operation, the absence of paid leave, and freedom from wage inflation, a pattern that carries far heavier implications when paired with Goldman Sachs data showing roughly 11,000 net U.S. job losses per month and a 3.3-percentage-point widening of the entry-level-to-experienced wage gap. Ultimately, the central issue is not the moment robots become as capable as humans, but the structural diagnosis that generative AI is already erasing the first rung of the white-collar ladder while physical AI simultaneously erases the first rung of the factory ladder, a two-bladed cut that has already begun on both ends of the labor market at once.

Key Points

Half of the "crossover" was built by absent humans, not present robots

The least-read line on Figure AI's chart isn't the blue one — it's the gray one. Robot count crossed 750 units in the second quarter of 2026, but human headcount sat nearly flat in the 180-to-250 range for the entire four-year stretch. A crossing point is simply where two lines meet, and when one line refuses to move, a crossover becomes dramatically easier to produce. That means half of the "robots overtook humans" narrative is actually an arithmetic artifact of hiring stagnation rather than robotic growth. Brett Adcock had already stated at Dreamforce in 2025 that "one of our goals is to have more humanoids in the office than humans," which means this milestone wasn't stumbled into — it was a KPI, set in advance and then hit on schedule. Packaging a self-selected target as a historic inflection point isn't proof of achievement; it's closer to circular reasoning dressed up as a headline.

Robots run at 20-30% human efficiency, yet $4 billion+ poured in anyway

A Chinese factory CEO quoted in reporting from June 2026 flatly reversed the conventional wisdom: current humanoid robots can only handle simple tasks like loading and unloading, running at just 20 to 30 percent of human work efficiency. Some units even fail to adapt to factory conditions and get hauled off to repair centers in batches — essentially mass "sick days" — which undercuts the assumption that robots simply run nonstop. UBTech's own internal estimate puts average productivity at 30 to 40 percent of a human worker, and battery life on leading Chinese models tops out at two to three hours per charge. Despite all of that, more than 30 billion yuan — over $4 billion — flowed into China's humanoid and smart-robot sector in the first quarter of 2026 alone, with a garment-equipment maker ordering 2,000 units and BYD announcing plans to deploy 20,000 of its own Yaoshunyi robots. This is not investors ignoring poor performance; it's investors doing the math and finding that poor performance still clears the bar when the alternative is chronic labor shortages driven by demographic decline and young workers avoiding factory floors entirely.

The substitution threshold is cost, not intelligence

Conventional wisdom says substitution should begin once robots become as capable as humans. Capital didn't wait for that milestone, and the reason lives entirely in the arithmetic. Even at 30 percent efficiency, a machine that runs three times the hours without shift changes, never demands a raise, generates no workers'-comp liability, and gets written off as a depreciating tax asset can already clear breakeven. IDTechEx has assessed that some high-throughput logistics roles already deliver payback within six months, and the International Federation of Robotics notes the cheapest torso-format commercial platforms have already fallen to roughly $28,000. That means substitution isn't a future event triggered by robots getting smarter — it's a present-tense event triggered by robots getting cheap enough. Years of anxiety were pointed at the distant threshold of artificial general intelligence, while the actual labor-market disruption came from cut-rate machines that can barely load a truck and occasionally break down. A low threshold for disruption isn't reassuring; it's a warning, because the lower the bar, the more companies clear it, and the faster they do.

The entry-level rung is being cut from both above and below at once

Looking only at physical labor tells half the story. Goldman Sachs' AI hiring tracker puts AI-driven net U.S. job losses at roughly 11,000 per month, totaling 136,000 over three years. Economist Elsie Peng's analysis found that a one-standard-deviation rise in AI displacement exposure widened the entry-level-to-experienced wage gap by about 3.3 percentage points, and the average 23 percent productivity boost generative AI delivers has flowed overwhelmingly to senior staff rather than juniors. A GMAC survey of 621 recruiters across 39 countries found 33 percent of employers overall, and 40 percent in tech specifically, are actively replacing entry-level roles with AI. In short, generative AI is severing the first rung of the office ladder while physical AI severs the first rung of the factory ladder at the same time, a structural signal considerably more dangerous than headline unemployment numbers.

Skepticism about capability and skepticism about trajectory are different questions

Rodney Brooks calls video-based dexterity learning "magical thinking of the first order," pointing out that current technology can't replicate the roughly 17,000 mechanoreceptors in a human hand, and predicts "a huge hype phase followed by a trough of disappointment." Boston Dynamics CEO Robert Playter concedes these robots "aren't autonomous enough" to skip active management, training, and maintenance, and prediction market Kalshi prices genuine mass-market humanoid sales in 2026 at just 21 percent. That skepticism holds up well against current capability. It does not hold up against deployment speed: Figure AI pushed its BotQ facility from roughly 60 units a month to 240 in sixty days, a 24-fold throughput jump in 120 days, while Morgan Stanley more than tripled its China shipment forecast within half a year. Capability is disappointing and trajectory is alarming, and both statements are simultaneously true. Treating those as one single question instead of two separate ones is exactly how forecasters end up either dismissing a real disruption or overhyping a technology that still can't reliably load a truck.

Data-center construction jobs are the painkiller masking the real trend

Goldman Sachs' tracker showing AI-driven monthly net job losses "slowing" from 16,000 to 11,000 was widely read as reassuring, but the composition of that cushion tells a different story. The offset comes largely from data-center construction employment, up 212,000 since 2022, of which only 69,700 positions are permanent — the rest vanish once buildings are complete. That means jobs erased by AI are being temporarily papered over by jobs built around constructing AI's physical infrastructure, a structure that cannot last by definition. April 2026 alone saw 21,900 layoffs, the highest single month since tracking began in 2023, pushing the three-year AI-linked total to 136,000. Once the construction boom peaks around 2027, the curve currently read as "slowing" is likely to steepen again, and mistaking a fading painkiller for genuine improvement risks missing the response window entirely.

Positive & Negative Analysis

Positive Aspects

- Pilot-to-standard-deployment evidence is now real, not staged

BMW's Figure 02 pilot at its Spartanburg plant ran for eleven months inserting sheet-metal parts and prepping weld sites on the body shop floor, supporting production of more than 30,000 BMW X3 units in that window. On June 25, 2026, BMW Group formally announced it was expanding follow-on model Figure 03 into logistics sequencing work. This is qualitatively different from a choreographed demo reel, because the decision to move from pilot to standard deployment only happens after a German automaker's production-planning department has reviewed the actual numbers. BMW's VP of production and logistics, Ulrich Wieland, described Spartanburg as the birthplace of humanoid robotics inside BMW's everyday manufacturing operations. The gap between marketing rhetoric and a genuine procurement decision sits exactly here, and it's a gap most other publicized "deployments" in this industry still haven't closed. Very few humanoid robotics vendors can point to eleven consecutive months of real production support on a line building tens of thousands of vehicles, which is precisely what makes this case different from a trade-show demo.

- The price curve is structurally accelerating adoption

IDTechEx projects average humanoid robot prices will fall as much as 68 percent, from roughly $35,000 in 2025 to a $17,000-to-$37,000 range by 2030. UBTech has already cut its Walker series production cost 25 percent versus 2024 and set 300,000 yuan as its internal commercial-viability line. Per the International Federation of Robotics, purchasable or leasable commercial humanoid platforms grew from three in 2024 and five in early 2025 to twelve in 2026, spanning a price range from $28,000 to $245,000. Platform diversification and price decline happening simultaneously is a signal of industry-wide maturation, not one company's marketing push. The assessment that some high-throughput logistics roles already deliver payback within six months confirms this curve is a real-world calculation, not a theoretical projection.

- Machines can absorb dangerous and physically punishing labor

Boston Dynamics CEO Robert Playter, in a 60 Minutes interview, summarized the industry's most honest value proposition: genuinely repetitive, back-breaking labor will eventually be handled by robots. It's no coincidence that the overwhelming majority of confirmed deployments to date — loading and unloading, sheet-metal insertion, logistics sorting — cluster exactly around the tasks associated with musculoskeletal injury and workplace accidents. In China specifically, demographic decline combined with younger workers avoiding factory jobs has created a structural labor shortage, and even a robot running at 20 to 30 percent efficiency carries its own independent economic logic under those conditions. In other words, this technology doesn't spread only by displacing workers who are already there — it also fills positions nobody was willing to take in the first place. That distinction matters for how this trend gets framed politically, because "the robot took a job nobody wanted" and "the robot took a job someone needed" are very different stories, and both are happening in different factories at the same time.

- Aggregate employment models still project net job gains

The World Economic Forum forecasts that AI and related technologies will create roughly 170 million new jobs globally by 2030 while eliminating about 92 million existing ones, for a net gain of 78 million. Research compiled by Goldman Sachs shows generative AI delivering an average 23 percent productivity increase, and 19.5 percent of U.S. businesses are already using AI in regular operations, a figure expected to climb to 22.7 percent within six months. Data-center construction employment alone has added 212,000 jobs since 2022. Every prior wave of automation since the Industrial Revolution has failed to produce net job destruction at the aggregate level historically, and this wave is likely no exception on paper. That said, this optimism holds only at the aggregate level and does not hold at the individual level, a caveat that must always travel alongside the headline number.

- New skilled-labor job categories are genuinely emerging

The least-quoted but most important part of Playter's comment is the admission that these robots aren't autonomous enough to run without oversight — they have to be built, trained, and maintained. That creates real demand for roles like robot fleet operators, remote-intervention technicians, training-data curators, and field maintenance engineers. China has filed 7,705 humanoid-robot-related patents over five years, five times the U.S. total, and its National Development and Reform Commission has formally designated embodied intelligence a new growth engine under its 15th Five-Year Plan, backing workforce development with policy. As Sabrina White noted in the GMAC survey, employers are still investing in people who exercise judgment, solve problems, and help organizations manage change, and that category looks likely to anchor future demand.

Concerns

- Entry-level pathways are vanishing from both directions simultaneously

The most serious problem isn't the unemployment rate — it's the disappearance of the pathway itself. In the GMAC survey, 33 percent of employers overall, and 40 percent in tech, said they're replacing entry-level roles with AI, and Goldman Sachs found the entry-level-to-experienced wage gap widened by 3.3 percentage points for every one-standard-deviation rise in AI displacement exposure. Offices are losing data entry, customer support, and junior coding; factories are losing loading, sorting, and repetitive assembly — and both happen to be the first rung of their respective ladders. Whoever manages, trains, and maintains robots twenty years from now should be someone starting on that same factory floor today, and once that starting point disappears, the entire pipeline that produces future skilled labor breaks with it. Because this kind of loss doesn't show up immediately in statistics, policy response is almost guaranteed to arrive late.

- Company-reported figures and independent field reporting flatly contradict each other

UBTech has publicly claimed its Walker S1 units deployed at a BYD facility improved efficiency by 100 percent and stability by 30 percent, and that it has secured letters of intent for more than 500 units from automakers. Yet independent, third-party reporting from the same period quotes a Chinese factory CEO stating robot work efficiency runs at just 20 to 30 percent of human levels, with units failing to adapt and being hauled off to repair centers en masse. Two numbers this far apart, from the same industry in the same period, tell you company-reported metrics can't be taken at face value. Morgan Stanley itself has warned that most demos "should be viewed with caution," and prediction market Kalshi prices genuine mass-market sales in 2026 at just 21 percent. Capital stacking up on top of unverified performance claims is itself a structural risk worth naming directly.

- Battery life and cost remain unresolved physical bottlenecks

The entire economic case for robotic substitution depends on round-the-clock operation, yet leading Chinese models currently run only two to three hours per charge. A machine that needs recharging every three hours isn't a 24-hour machine — it's a shift worker running at roughly 30 percent efficiency, which undercuts the basic assumption behind the breakeven math. On cost, a wide gap still separates the 300,000-yuan commercial-viability threshold from the several-million-yuan price tags on current research-grade models. As Rodney Brooks points out, until technology can replicate the roughly 17,000 mechanoreceptors in a human hand, expansion into precision work remains a distant prospect, and he predicts robots succeeding within the next fifteen years will more likely abandon humanoid form altogether in favor of wheels and multiple arms. Hardware limitations simply don't improve threefold in six months the way software sometimes does.

- Institutional forecasts diverge by up to sixfold, making planning nearly impossible

Look just at 2026 China humanoid-robot shipment forecasts: UBS says 30,000, the China Center for Information Industry Development says 38,000, Morgan Stanley says 50,000, and Zhejiang Humanoid Robot Innovation Center chief scientist Xiong Rong throws out 100,000 to 200,000. A sixfold spread in forecasts for the same year, same country, and same product category means this market doesn't yet have a demand function anyone can rely on. Morgan Stanley itself raised its own forecast twice within months, from 14,000 units in early 2026 to 50,000 by June, and while that kind of upward revision is evidence of acceleration, it's equally evidence of how poor the original estimate was. Under this level of uncertainty, companies can't plan capital expenditure, governments can't design workforce policy, and workers can't plan careers, and the fact that 30 billion yuan in capital has already flowed in ahead of that clarity signals a shakeout could begin at any time. When even the analysts closest to the data can't agree within a factor of six, treating any single number in this space as gospel is itself a forecasting error.

- Net-gain optimism conceals individual-level devastation

The World Economic Forum's net gain of 78 million jobs is the single most dangerously misused statistic in this entire debate. The WEF's own report states plainly that the people losing jobs and the people benefiting from new ones are, overwhelmingly, different people, and "net gain" is a concept that only holds together on a balance sheet. A worker inserting sheet metal in Spartanburg doesn't become a prompt engineer next month, and a 23-year-old loading trucks in a Guangzhou factory needs two to three years of training — plus income to survive that training — to become a robot maintenance technician, income that was supposed to come from the very job that just disappeared. That's exactly why the WEF separately flagged roughly 120 million people as facing serious automation-driven displacement risk within three to five years. Using aggregate optimism as a reason to delay policy response amounts to building a social safety net on top of a statistical illusion.

Outlook

Looking six months out, into the back half of 2026, I feel fairly confident about one specific thing: the noise surrounding the numbers is going to get louder before the numbers themselves get any clearer. The evidence is right there in how wildly institutional forecasts for 2026 China humanoid-robot shipments already diverge. UBS says 30,000 units and draws a hard line that "real mass production starts in 2027." The China Center for Information Industry Development says 38,000. Morgan Stanley says 50,000. Meanwhile Xiong Rong, chief scientist at the Zhejiang Humanoid Robot Innovation Center, throws out a figure of 100,000 to 200,000. The low and high ends of that range differ by more than sixfold. When forecasts for the same year, same country, and same product category diverge sixfold, that tells you this market doesn't yet have a demand function anyone can trust. My own read is that when year-end numbers land, whatever they are, they'll probably fall into that ambiguous 40,000-to-60,000 band where both the bulls and the bears will claim vindication.

There's a second signal I expect to be far more reliably observable over the same stretch: the type of deployment. Break down every success story that's surfaced so far and one pattern jumps out immediately. BMW's Figure 02 in Spartanburg did sheet-metal insertion and weld prep. Figure 03 is moving into logistics sequencing. In Chinese factories, robots are loading and unloading. Every single one of these tasks is "moving something heavy, from a fixed spot, repeatedly." These are jobs that call for strength and stamina, not dexterity. I expect more than 80 percent of newly announced deployments in the second half of 2026 to stay squarely within that category. If cases outside that category start appearing — precision assembly or handling of irregular objects, showing up simultaneously across multiple automakers or electronics manufacturers — that should be read as the first real sign that Brooks's skepticism is starting to crack. If the second half of the year keeps producing nothing but loading and logistics sequencing, that means the trough of disappointment is arriving right on schedule.

The medium term, 2027 through 2028, is where I think the real contest gets decided, and I'd narrow it down to exactly two variables: cost and battery. IDTechEx projects the average price of a humanoid robot will fall by as much as 68 percent from roughly $35,000 in 2025 to a $17,000-to-$37,000 range by 2030. UBTech has already cut the production cost of its Walker series by 25 percent versus 2024 and has set 300,000 yuan as its internal commercial-viability threshold. I honestly think the cost side is largely a matter of time. Once component standardization and volume kick in, prices fall almost by definition, and the fact that the International Federation of Robotics counted commercial humanoid platforms rising from three in 2024 to twelve by 2026 is itself evidence that the supply chain is already forming underneath this industry.

Battery life is the harder problem. Leading Chinese models currently run only two to three hours per charge. That matters enormously because the entire economic case for robotic substitution rests on round-the-clock operation. A machine that needs recharging every three hours isn't a 24-hour machine — it's a shift worker, and a shift worker running at 30 percent of human efficiency at that. I think whether the industry achieves a meaningful breakthrough in battery chemistry or hot-swap systems between 2027 and 2028 is the single largest fork in the road determining whether this technology stays confined to niche use cases or scales into mass deployment. Cost falls with economies of scale almost by default. Energy density does not fall the same way, because chemistry doesn't double in performance every year the way semiconductors do.

Whatever happens in employment over that same window will be far less dramatic and far more brutal, in my view. Plenty of people read the news that Goldman Sachs' AI-driven job-loss tracker "slowed" from 16,000 to 11,000 net jobs a month as a reassuring signal. I read it the opposite way. Look at what's actually been cushioning that number: data-center construction employment, which has added 212,000 jobs since 2022, of which only 69,700 are permanent positions. The rest disappear the moment the building is finished. In other words, jobs erased by AI are being temporarily papered over by jobs building the physical infrastructure AI runs on, and buildings, eventually, get finished. I expect that once the data-center construction boom peaks sometime in 2027, the curve that currently looks like it's "slowing" will steepen again. When that happens, people will describe it as things suddenly getting worse, when really, the painkiller just wore off.

Looking further out, across the 2028-to-2031 window, I'd assign probabilities across three distinct scenarios. Start with the bullish one. The fact that Morgan Stanley more than tripled its China shipment forecast within half a year, and is now talking about a $5 trillion ecosystem by 2050, signals that the entire consensus is being repriced in real time. If robot productivity climbs from UBTech's current 30-to-40 percent toward its own targeted 80 percent by early 2027, if IDTechEx's projected 68 percent price decline materializes on schedule, and if BMW's pilot-to-standard-deployment path gets copied across other automakers and logistics operators, the current twelve-platform commercial ecosystem tracked by the International Federation of Robotics moves quickly toward standardization. For context, that platform count was three in 2024 and five in early 2025 — a fourfold jump in two years. If this path plays out, we'd be looking at something like a "smartphone moment" for robotics before 2030. I'd put roughly 25 percent odds on this outcome.

The base case is far duller, and precisely because of that, far more plausible. Goldman Sachs' own baseline projects over 250,000 unit shipments by 2030 and a $38 billion market by 2035. $38 billion sounds like a lot until you realize that's smaller than a single semiconductor company's annual revenue. In other words, even Goldman Sachs is framing this as a specialty-equipment market, not an industrial revolution. UBS's assessment that "real mass production starts in 2027" points in the same direction.

Under this path, humanoid robots settle into a narrow niche — logistics sorting, loading, repetitive assembly assistance — and get quietly better within that lane. The employment shock shows up not as a dramatic collapse but as slow erosion. That's essentially the picture the World Economic Forum has painted: 92 million jobs eliminated by 2030, 170 million created, for a net gain of 78 million. The aggregate is positive. I'd assign this scenario 50 percent odds.

But I think that "net 78 million" figure is the single most dangerous statistic in this entire debate. The World Economic Forum's own report states plainly that the people losing jobs and the people benefiting from newly created jobs are, overwhelmingly, different people. "Net gain" is a concept that only works on a balance sheet. The worker inserting sheet metal in Spartanburg does not become a prompt engineer next month. A 23-year-old loading trucks in a Guangzhou factory would need two to three years of training — and income to survive that training — to become a robot maintenance technician, and that income was supposed to come from the very job that just disappeared. That's exactly why the WEF separately flagged roughly 120 million people as facing serious displacement risk within the next three to five years. Aggregate optimism and individual-level pessimism aren't contradictory; they're two faces of the same coin. I expect the core political fault line of the next five years to form right along that gap.

The bearish scenario gets 25 percent from me. If Rodney Brooks's predicted "trough of disappointment following massive hype" arrives as forecast, here's roughly how the sequence plays out. Two or three humanoid robotics startups miss their promised shipment targets during 2027 earnings season. Batteries are still stuck at three hours. Efficiency still hasn't cleared 40 percent of human output. The 300,000-yuan commercial breakeven point is still a long way off. Kalshi's 21 percent probability for mass-market sales in 2026 gets rediscovered and re-cited everywhere. Morgan Stanley's own caveat — that most demos "should be viewed with caution" — starts getting quoted again, but this time as a warning that came true. Speculative capital, like the 30 billion yuan that piled in during the first quarter of 2026, starts getting pulled back out, a shakeout begins, and even UBS's conservative 30,000-unit forecast ends up missed.

And here's the part of this scenario that matters most, in my view: even here, the jobs don't come back. Capital exiting robotics doesn't automatically flow into entry-level hiring, because hiring was never the default state it's assumed to be. The reason Figure AI's gray line stayed flat for four years was never really about robots at all — it's because not hiring had already become a management virtue in its own right, one that survives regardless of whether the robots underperform or overperform. That's the uncomfortable thread that connects all three scenarios: the bull case, the base case, and the bear case each produce a different robot market, but none of them produce a return to the old hiring habits. Whichever version of 2028 arrives, the muscle for skipping entry-level hiring will already be fully built.

So let me close with one actionable takeaway. At the individual level, I think the old advice — "learn skills AI can't replace" — has become close to useless. If the real front line of substitution isn't dexterity or intelligence but cost structure, then your defense isn't measured by how capable you are; it's measured by how expensive it would be to cut you. There's a hint buried in something Sabrina White said in that GMAC survey: employers are still investing in people who can exercise judgment, define problems, and help organizations navigate change. What robots can't do isn't the loading part — it's the part right before it, deciding what should be loaded and why. And at the societal level, I believe that if we leave the first rung of the ladder entirely to market forces, that rung will disappear. Companies never hired entry-level workers out of charity; it was always an investment in future skilled labor. The moment a company realizes it can coast for three years on robots and senior staff without making that investment, nobody gets hired. And three years from now, when everyone suddenly notices there are no skilled workers left to hire, the first rung that would have produced them will already be gone. I think that's the real bill coming due over the next five years.

Sources / References

- Figure CEO: The Robots Have Officially Outnumbered the Humans — RoboHorizon

- BMW Group Advances the Use of Physical AI in Production with Figure 03 Project in Spartanburg — BMW Group

- More Robots Getting Factory Jobs in China: Frequent Unplanned Absences and Still No Match for Skilled Workers' Expertise — Asia Business Daily

- Yearender: China's Humanoid Robots Step From Spectacle Toward Scalable Industrial Reality — Xinhua

- 2026 Humanoid Robot Industry Outlook: 100,000-Unit Mass Production Approaching, Year of Commercialization Begins — Xinhua

- How Many Jobs Is AI Destroying? Goldman Sachs Says 11,000 Per Month — Fortune

- AI Is Cutting 16,000 U.S. Jobs a Month — and Gen Z Is Taking the Brunt — Fortune

- Gen Z's Hiring Hell: 1 in 3 Employers Admit They're Replacing Entry-Level Roles With AI — Fortune

- Four Ways AI and Talent Trends Could Reshape Jobs by 2030 — World Economic Forum

- Boston Dynamics AI-Powered Humanoid Robot Learning Factory Work (60 Minutes Transcript) — CBS News

- Famed Roboticist Says Humanoid Robot Bubble Is Doomed to Burst — TechCrunch

- Morgan Stanley Doubles China Humanoid Robot Shipment Forecast — CNBC

- IDTechEx: Humanoid Robot Price Falls 68% by 2030, Six-Month Payback Possible Now — TechTimes

- The Global Market for Humanoid Robots Could Reach $38 Billion by 2035 — Goldman Sachs

- UBS: China Humanoid Robot Demand Forecast at 30,000 Units in 2026, Real Mass Production Likely in 2027 — WallStreetCN

- UBTech Announces Walker S1 Performance Results at BYD Factory Deployment — Securities Times (STCN)

- "We're Building a New Species, Not Robots": Figure AI's Brett Adcock — Forbes India

- Global Robotics Statistics (12 Commercial Humanoid Platforms, 542,000 Industrial Robot Installations) — International Federation of Robotics