Lithium's Throne Is Shaking — What Happens When Sodium-Ion Batteries Hit the Mass Market in 2026

Summary

Sodium-ion batteries are entering mass production in passenger cars in 2026, triggering a seismic shift in the lithium-dominated battery market and global energy supply chains.

Key Points

CATL and BYD Launch Mass Production of Sodium-Ion Batteries in Passenger Cars

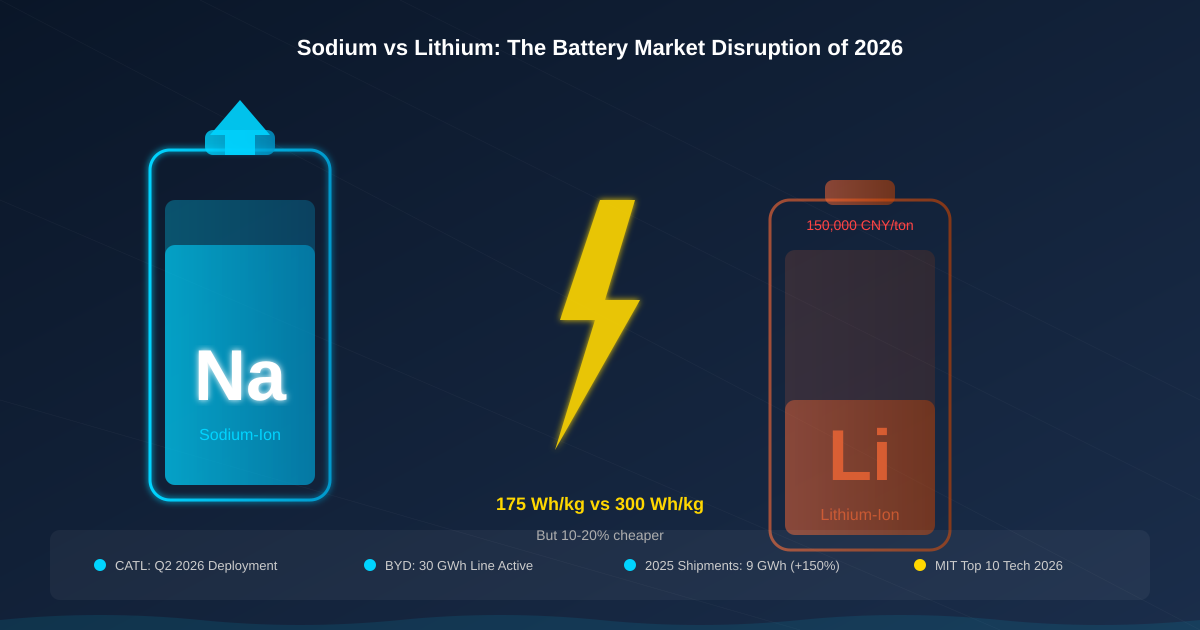

CATL will install sodium-ion batteries in GAC Aion Y Plus starting Q2, marking the first mass-production application in a passenger vehicle. BYD already has a 30 GWh production line running. Global sodium-ion battery shipments in 2025 reached approximately 9 GWh, up 150% year-over-year. MIT Technology Review named sodium-ion batteries one of the 10 Breakthrough Technologies of 2026. This simultaneous convergence signals that both technological maturity and commercial deployment have arrived at once.

Lithium Supply Chain Geopolitical Vulnerability Opens the Door for Sodium

Lithium carbonate prices blew past 150,000 yuan per ton in early 2026, pushing battery manufacturers to breaking point. Lithium reserves are concentrated in a handful of countries like Chile, Australia, and Argentina, while China monopolizes the refining process. This structure is eerily similar to OPEC's grip on the oil market. Sodium, by contrast, is the sixth most abundant element on Earth, extractable from seawater with virtually no geographic constraints. The dramatic reduction in raw material costs enables a fundamental restructuring of battery economics.

Sodium-Ion Positions Itself as Lithium's Complement, Not Replacement

By 2026, roughly 70% of sodium-ion batteries are projected for grid-scale energy storage, with EVs accounting for just 18%. Lithium-ion will continue to dominate long-range, high-performance EVs, but sodium-ion will rapidly carve out territory in urban micro-EVs, commercial vehicles, energy storage, and battery-swap systems. Energy density of 175 Wh/kg supporting 500 km range is more than enough for urban commuters. This realistic positioning actually increases sodium-ion's probability of success.

Sodium-Ion Dominates Lithium in Safety and Cold-Weather Performance

In nail penetration tests, thermal runaway does not occur, and performance remains stable under overcharge, short-circuit, and compression scenarios. Given that lithium-ion thermal runaway has been a leading cause of EV fires, this difference carries enormous implications. The batteries have already passed China's latest national safety standards, likely leading to lower insurance costs and regulatory relaxation. Superior cold-temperature performance translates to a significant competitive edge in Northern Europe and Canada.

Democratization of Battery Raw Materials Is Rewriting Geopolitics

Because sodium can be extracted from seawater, countries like Indonesia, India, and African nations can build their own battery industries. This was impossible in the lithium era. When energy storage raw materials are liberated from geographic constraints, developing nations' grid modernization accelerates dramatically. Geopolitical pressure on the lithium triangle weakens, and scenarios like Australian supply disruptions can no longer shake the global battery market. This is sodium-ion's most underestimated revolutionary potential.

Positive & Negative Analysis

Positive Aspects

- 10-20% Manufacturing Cost Reduction Enables Sub-$20,000 EVs

Sodium-ion batteries can achieve manufacturing costs 10-20% lower than lithium-ion, directly translating to lower consumer EV prices. If CATL's Aion Y Plus deployment succeeds, urban EVs priced below $20,000 become realistic. This could be the key to solving the last remaining barrier to mass EV adoption: price. The fundamental reduction in raw material costs ensures price reductions are sustainable.

- Elimination of Thermal Runaway Addresses EV Fire Anxiety

In nail penetration tests, thermal runaway does not occur, and performance remains stable under overcharge, short-circuit, and compression. The batteries have already passed China's latest EV battery safety standards. Consumer anxiety about EV fires can be significantly reduced, likely leading to lower insurance costs and regulatory relaxation. Safety is particularly crucial for accelerating adoption in commercial vehicles and public transit.

- Seawater-Extractable Raw Materials Dramatically Reduce Supply Chain Risk

Sodium is the sixth most abundant element on Earth and extractable from seawater. This can dramatically reduce dependence on any specific country or region for raw materials. Geopolitical pressure on the lithium triangle weakens and developing nations can build their own energy storage industries.

- Superior Cold-Weather Performance Expands EV Geographic Market

In cold-climate regions like Canada, Northern Europe, and Russia, the biggest obstacle to EV adoption has been winter battery performance degradation. Sodium-ion structurally solves this problem. This effectively expands the geographic market for EVs, opening markets where lithium-ion has been weak.

- Dual Cost-Safety Advantage in Energy Storage Systems

In grid-scale energy storage, cost and safety matter more than weight or volume, and sodium-ion has advantages in both. This is why 70% of sodium-ion batteries are projected for energy storage in 2026. The combination of cheap sodium-ion storage with renewable energy generation could fundamentally transform how power grids operate.

Concerns

- Energy Density Gap Prevents Entry into Premium EV Market

Sodium-ion's best energy density of 175 Wh/kg trails lithium-ion's 250-300 Wh/kg significantly. Competition in the long-range premium EV market is impossible. The odds of a Tesla Model S or Mercedes EQS switching to sodium-ion are zero for the foreseeable future.

- Cycle Life at Half of LFP Increases Total Cost of Ownership

Sodium-ion's 4,000-6,000 cycle life versus LFP's 12,000+ cycles has significant implications for TCO in applications like energy storage that cycle daily. If the lifespan is half, battery replacement costs double — simple but devastating arithmetic.

- Economic Shock to Lithium-Dependent Nations

Countries like Chile, Australia, and the DRC that depend on lithium mining could face economic damage from declining demand. Chile's Atacama Desert region relies on lithium mining as an economic pillar, yet no transition plan has been prepared.

- Chinese Company Dominance Risks New Technology Monopoly

CATL and BYD leading sodium-ion commercialization risks deepening China dependency in next-generation battery technology. Trying to solve the Chinese monopoly in lithium refining could create a new problem: Chinese monopoly in sodium-ion manufacturing.

- Absence of Recycling Infrastructure Creates Waste Battery Challenge

Lithium-ion batteries have decades of recycling technology development, but dedicated sodium-ion recycling systems have not reached early stages. Once large-scale commercialization begins, the waste battery problem will surface rapidly.

- Counterattack from Solid-State Lithium and Other Competing Technologies

Next-generation lithium-based technologies like solid-state batteries and lithium-sulfur batteries are in development. If they reach commercial scale, sodium-ion's cost advantage could be neutralized. Technology competition is never one-directional.

Outlook

In the short term, the second half of 2026 will be the most important six months in sodium-ion battery history. If CATL's Aion Y Plus deployment succeeds, it becomes the litmus test proving that sodium-ion batteries work in real consumer products. I believe this first mass-production application will be the trigger that shatters the industry's wait-and-see attitude. By the end of 2026, I expect at least 3-5 additional vehicle models to announce sodium-ion battery options. In the energy storage market, sodium-ion penetration is already accelerating, and we should start seeing bids 15-20% lower than lithium-ion for grid-scale projects.

Looking at the medium term of 2027-2028, the sodium-ion battery market is likely to surpass 50 GWh annually. Three key changes deserve attention during this period. First, sodium-ion battery manufacturing facilities will start appearing outside China. Europe's Northvolt or American startups could add sodium-ion lines. Second, as energy density improves beyond 200 Wh/kg, the range of applicable EVs will expand from urban micro-cars to mid-size sedans. Third, sodium-ion-based affordable EVs will see explosive growth in India and Southeast Asian markets. These regions are extremely price-sensitive, making sodium-ion's cost advantage most powerful precisely there.

Looking at the long term of 2029-2030, I project sodium-ion batteries will capture 15-25% of the total battery market. A scenario where sodium replaces lithium entirely is not realistic, but sodium-ion will become the dominant technology in four key segments: energy storage, affordable EVs, commercial vehicles, and cold-climate markets. Lithium will concentrate on premium EVs and applications requiring high energy density, transforming today's lithium monopoly into a lithium-sodium duopoly.

In a bull case scenario, sodium-ion energy density reaches 220 Wh/kg by 2028, and lithium prices soar past 200,000 yuan per ton, driving sodium-ion's market share to 30%. Lithium mining company stocks could drop 30-40% in this scenario. In the base case, sodium-ion grows steadily in energy storage and affordable EV markets, reaching 15-20% market share by 2030. Lithium prices stabilize around 100,000-120,000 yuan per ton due to sodium-ion's competitive pressure. In a bear case, early commercialization of solid-state lithium batteries dramatically improves lithium-ion's price and performance, erasing sodium-ion's cost advantage. Sodium-ion would remain confined to the energy storage niche, with market share of just 5-8%.

The most intriguing long-term prospect is that sodium-ion batteries could revolutionize energy access in developing nations. If affordable sodium-ion energy storage systems can be deployed in regions across sub-Saharan Africa, South Asia, and Southeast Asia where grid infrastructure is lacking, the solar plus sodium-ion combination could completely replace diesel generators. I believe this is sodium-ion's most underestimated potential — battery technology becoming not just a tool for moving rich countries' EVs, but a weapon against energy poverty.

Sources / References

- CATL Supplier Conference - Multi-sector large-scale sodium-ion battery deployment confirmed — CATL

- Sodium-ion batteries: 10 Breakthrough Technologies 2026 — MIT Technology Review

- CATL CTO Gao Huan interview - Q2 passenger car deployment confirmed — China Securities Journal

- EV battery leader CATL is gearing up for sodium-ion batteries in 2026 — Electrek

- CATL, BYD fast-track sodium-ion battery shift as lithium prices soar — CarNewsChina

- CATL Plans Major Sodium-Ion Battery Expansion and Performance Upgrade by 2026 — ChemAnalyst

- CATL confirms significant upgrade to sodium-ion battery product range — Energy Storage News