Samsung Just Threw $73 Billion at the AI Chip War — Can It Reclaim the HBM4 Throne While SK Hynix Holds 62% of the Market?

Summary

Samsung's record $73.3B semiconductor investment, the strategic HBM4 and foundry alliance with AMD, and the vertical integration gamble challenging the SK Hynix-Nvidia axis could reshape the semiconductor industry's power structure.

Key Points

Record $73.3B Investment — Outspending Even TSMC on AI Chips

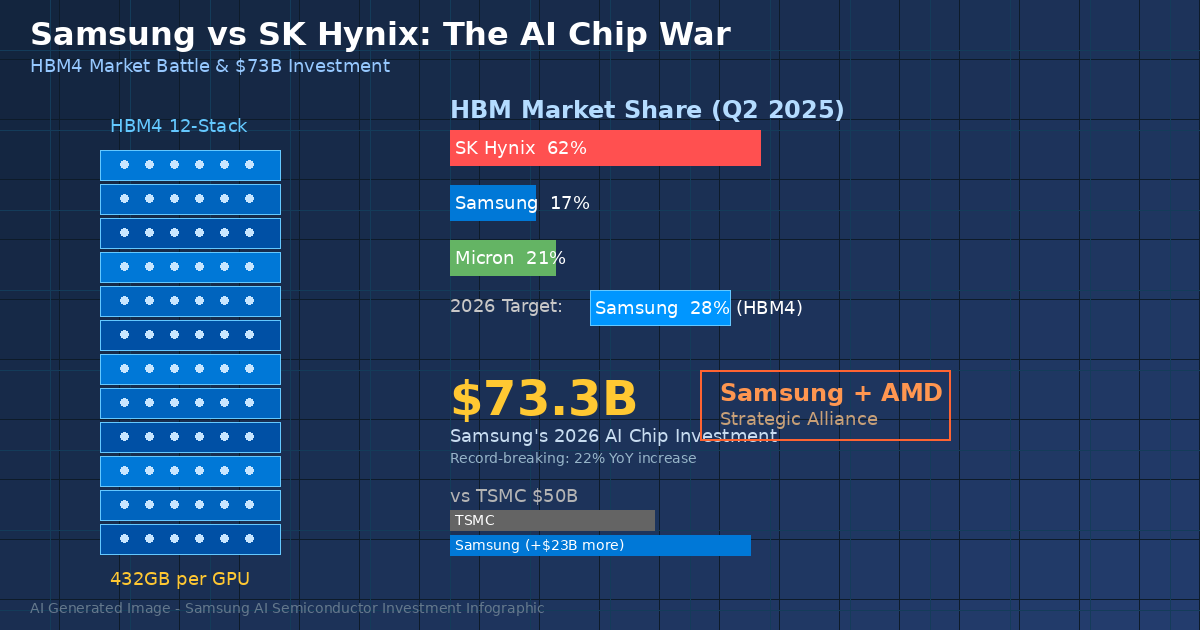

Samsung Electronics announced it will spend 110 trillion won ($73.3B) on semiconductor investment in 2026 alone. This is an all-time record, a 22% increase year-over-year, and exceeds TSMC's 2026 capital expenditure of approximately $50B by over $23B. The investment is concentrated on HBM4 mass production, next-generation 2nm process development, and the Pyeongtaek P5 fab construction. Samsung has prioritized market share recovery over short-term profitability, reflecting deep conviction in long-term AI semiconductor demand growth. Successful execution would lift the entire Korean semiconductor ecosystem through surging orders for equipment and materials suppliers.

Counterattack From 17% HBM Share — Challenging SK Hynix's 62% Dominance

As of Q2 2025, SK Hynix held 62% of the global HBM market, Micron 21%, and Samsung just 17%. The former undisputed king of memory semiconductors has been pushed to last place in AI's most critical component. Counterpoint Research projects Samsung's HBM4 market share to rebound to 28% in 2026, though that remains barely half of SK Hynix's projected 54%. SK Hynix is estimated to capture roughly 70% of Nvidia's Vera Rubin HBM4 demand. To close this gap, Samsung must secure both the AMD channel and a backup supplier position with Nvidia simultaneously.

Samsung-AMD Strategic Alliance — A New Front Against the TSMC-Nvidia Axis

On March 18, 2026, Samsung and AMD signed a Memorandum of Understanding for strategic collaboration on next-generation AI memory solutions. Samsung will exclusively supply HBM4 for AMD's MI455X, provide optimized DDR5 for EPYC processors, and the two companies are discussing Samsung manufacturing AMD chips at its 2nm foundry. The alliance's core value lies in the memory-plus-foundry package deal — a vertical integration card that neither SK Hynix nor Micron can replicate. AMD CEO Lisa Su personally visited Samsung's Pyeongtaek complex to sign the MOU, reflecting AMD's strategic intent to reduce TSMC dependency.

MI455X's 432GB HBM4 — Outgunning Nvidia Rubin's 288GB in Memory

AMD's next-generation AI accelerator MI455X will pack 432GB of HBM4, 50% more than Nvidia's Rubin GPU at 288GB. Samsung's 12-high HBM4 stacks using twelve 36GB modules make this possible. AMD has chosen to overwhelm Nvidia on memory capacity, and Samsung has become the linchpin of that strategy. However, more HBM capacity does not necessarily translate to proportionally better AI workload performance, so the real-world value of 432GB must be proven through actual benchmarks.

The Foundry Yield Achilles' Heel — Can Samsung Catch TSMC at 2nm?

Samsung's foundry yield problems remain a chronic challenge, unresolved even at 3nm. While the AMD MOU includes foundry collaboration, an MOU is not a binding contract. Whether AMD will actually shift production volumes to Samsung's uncertain 2nm SF2P process, abandoning TSMC's proven yields, remains an open question. However, if Samsung demonstrates competitive 2nm yields and AMD shifts even a portion of its volumes, it would be a historic event — the first genuine crack in TSMC's monopoly over cutting-edge process nodes. Qualcomm, Google, and Microsoft could begin considering Samsung Foundry as a viable alternative.

Positive & Negative Analysis

Positive Aspects

- Record investment scale exceeding TSMC

$73.3B exceeds TSMC's 2026 capex of $50B by over $23B. If concentrated on HBM4 production and 2nm process development, Samsung can rapidly close the technology gap. The investment boosts Korea's entire semiconductor ecosystem through surging equipment and materials orders, carrying significance at the national industrial strategy level.

- Uniquely positioned vertical integration of memory and foundry

Samsung is the only company on Earth that can manufacture both HBM and logic chips. The ability to offer AMD a memory-plus-foundry package deal is a structural advantage that SK Hynix, Micron, and TSMC cannot replicate. If this vertical integration model works, Samsung offers customers a one-stop solution and secures a durable competitive moat.

- Strategic alliance with AMD, a growing challenger

As the AI accelerator market transitions from Nvidia monopoly to multi-player competition, AMD MI455X's 432GB HBM4 overwhelms Nvidia on memory capacity. Betting on AMD's growth gives Samsung stable HBM demand independent of Nvidia. As AMD's data center market share rises, Samsung's HBM shipments grow in lockstep.

- Projected HBM4 share rebound to 28%

Counterpoint Research projects Samsung's HBM4 market share at 28%, an 11-percentage-point jump from the current 17%. Samsung also unveiled its HBM4E roadmap at GTC 2026, signaling commitment to the Nvidia Vera Rubin platform. Vice Chairman Jun's statement that customers said Samsung is back suggests positive HBM4 performance validation.

- Structural AI infrastructure demand backstops the investment

Microsoft, Google, Meta, and Amazon continue investing hundreds of billions in AI data centers through 2026. Despite the Hormuz strait crisis and recession fears, AI infrastructure spending remains relatively resilient. This structural demand serves as a safety net ensuring Samsung's $73B investment does not become excess capacity.

Concerns

- The gap with SK Hynix runs deeper than numbers suggest

The 62% versus 17% market share gap reflects not just volume differences but years of technical optimization and validation accumulated through close Nvidia collaboration. SK Hynix is estimated to capture roughly 70% of Nvidia Vera Rubin HBM4 volumes. Filling this gap through the AMD channel alone is challenging. Rebuilding trust in HBM will take at minimum two to three years.

- Foundry yield problems remain a chronic challenge

Samsung failed to close the gap with TSMC at 3nm. Declaring victory at 2nm SF2P is premature. Signing an MOU and actually shifting production volumes are entirely different propositions. Whether AMD has sufficient incentive to risk Samsung's uncertain 2nm yields over TSMC's proven track record remains doubtful, and the risk of the MOU never materializing into actual foundry contracts is significant.

- Financial burden of $73B and semiconductor cyclical risk

Semiconductors are a cyclical industry where booms and busts alternate. If AI demand does not sustain its trajectory or HBM4 adoption stalls, $73B converts to excess capacity. The Hormuz crisis is driving up energy costs and inflation, raising equipment and materials procurement costs and potentially reducing the real purchasing power of the investment.

- Hormuz strait crisis and global supply chain instability

Oil prices surged to $126 per barrel, rattling global supply chains. The Dallas Fed estimates a Hormuz blockade could lower global GDP growth by 2.9 percentage points. Rising energy costs, commodity prices, and recession fears create simultaneous headwinds that could introduce unexpected variables into Samsung's massive investment execution.

- Rising Chinese competitor risk

CXMT and YMTC are waging price wars in mature process markets. While they cannot enter the advanced HBM market immediately, pricing pressure on commodity memory could squeeze Samsung's overall memory profitability. As the US-China semiconductor rivalry intensifies, Samsung faces the dual burden of competing on both fronts simultaneously.

Outlook

Looking at the next six months, the second half of 2026 serves as Samsung's first real test for its HBM4 strategy. Whether Samsung can break through 30% HBM market share as it begins mass production at Pyeongtaek P5 is the critical question. Achieving Counterpoint's 28% forecast requires stabilizing yields on the 12-high, 36GB HBM4 stacks for AMD MI455X, with an 80%+ yield rate as the minimum threshold given the technical difficulty involved.

This is also when Nvidia validation results for Samsung's HBM4E, unveiled at GTC 2026, should materialize. If Samsung can secure even a backup supplier position on the Vera Rubin platform, it becomes a pivotal moment for rebuilding market trust. Even if SK Hynix takes 70% of HBM4 volumes, whether Samsung or Micron captures the bulk of the remaining 30% is the critical variable for the second half of 2026.

The market reception of the AMD MI455X also demands close attention. If 432GB of HBM4 proves to be a genuine differentiator in real-world AI workloads, Samsung's AMD strategy gains full validation. However, in use cases where GPU compute performance rather than HBM capacity is the bottleneck, Nvidia Rubin's 288GB may prove sufficient. The resolution of this technical debate will determine the value of the Samsung-AMD alliance.

On a one-to-two-year horizon, 2027 is the real showdown. The central question is whether Samsung Foundry can begin contract manufacturing AMD chips on its 2nm SF2P process. Currently, all of AMD's AI accelerators are produced at TSMC on 4nm and 3nm. If Samsung cannot demonstrate yields equal to or better than TSMC at 2nm, the MOU remains just words on paper.

However, if Samsung proves its 2nm capability and AMD shifts even 20-30% of its volumes, it becomes an industry-altering event. It could be the first genuine crack in TSMC's monopoly over cutting-edge process nodes, and other fabless companies would begin seriously considering Samsung as an alternative. Qualcomm, MediaTek, and even big tech companies like Google and Microsoft with their own chip design teams could start knocking on Samsung Foundry's door.

The global economic environment during this period cannot be ignored. A prolonged Hormuz crisis could dampen IT investment through higher energy costs and recession fears. Paradoxically, however, AI infrastructure spending is likely to remain relatively resilient even amid an economic slowdown. Microsoft, Google, Meta, and Amazon continue pouring hundreds of billions into AI data centers through 2026, providing a structural demand floor that backstops Samsung's massive investment.

Over the two-to-five-year horizon, both success and failure scenarios are plausible. In the bull case, Samsung secures 30-35% HBM4 share and succeeds at 2nm foundry production, with the memory-foundry-packaging vertical integration model finally bearing fruit. Samsung forms a duopoly with TSMC as the two pillars of the global semiconductor industry, with market capitalization potentially doubling from current levels.

In the base case, HBM share improves meaningfully to 25-30%, but the foundry gap with TSMC remains. The AMD collaboration focuses on memory while foundry volumes stay limited. Samsung solidifies its position as the world's best memory company plus the world's second-best foundry without triggering a fundamental power shift.

In the bear case, an AI bubble burst causes HBM demand to collapse, Samsung's massive investment converts to excess capacity, 2nm yields stagnate, AMD stays with TSMC, and Chinese competitors like CXMT and YMTC squeeze Samsung's commodity memory margins through price wars.

The most likely outcome sits close to the base case. Samsung will achieve a meaningful rebound in HBM, but threatening SK Hynix's throne will take another two to three years. The foundry battle requires an even longer horizon. But what matters most is this: had Samsung not made this investment now, it risked being permanently relegated in the AI semiconductor race. This is not an investment for victory — it is an investment for survival.

Sources / References

- Samsung to Invest Record $73 Billion in AI Chip Comeback Bid — Bloomberg

- Samsung and AMD Expand Strategic Collaboration on Next-Generation AI Memory Solutions — Samsung Global Newsroom

- AMD Secures Samsung HBM4 for MI455X — TrendForce

- SK Hynix holds 62% of HBM, Micron overtakes Samsung — Astute Group

- What the closure of the Strait of Hormuz means for the global economy — Federal Reserve Bank of Dallas

- Samsung Unveils HBM4E AI Memory Chips at GTC 2026 — WinBuzzer

- Samsung and AMD Expand Strategic Collaboration — AMD