The Theme Park Guy Just Inherited the Kingdom — What Disney's CEO Swap Really Asks of Hollywood

Summary

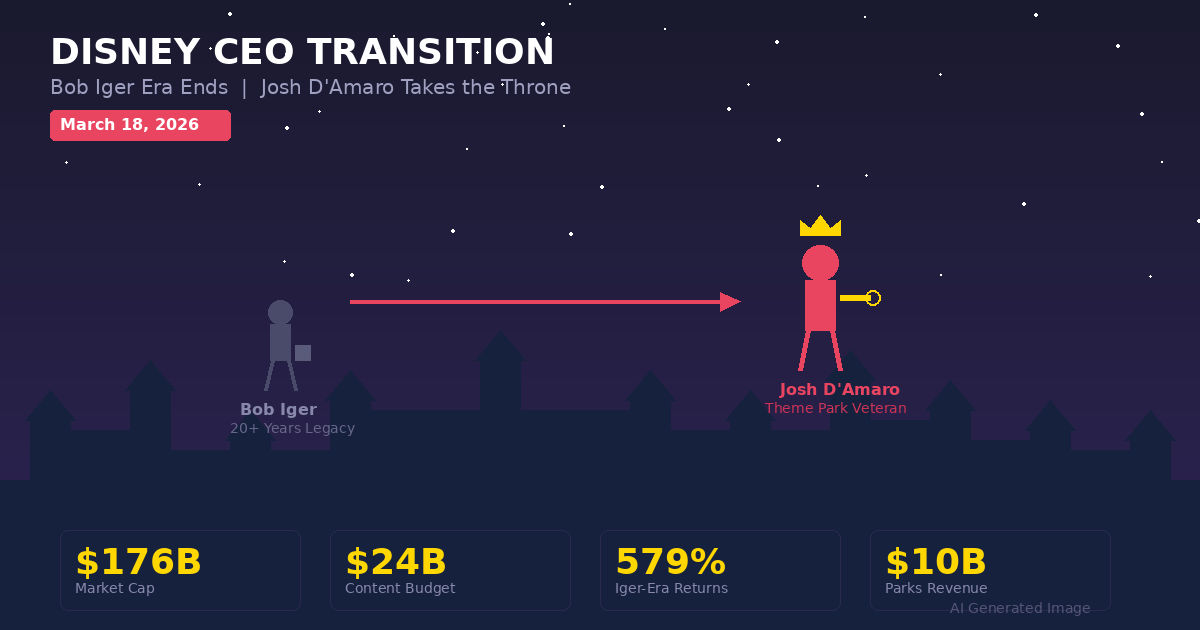

Bob Iger handed the Disney throne he held for over two decades to theme park veteran Josh D'Amaro. Entrusting the keys of a content empire to an 'experience' expert may be a declaration that Hollywood's future lies not on screens, but in spaces.

Key Points

Bob Iger Closes the Book on Two Decades of Empire Building

Bob Iger led Disney from 2005 onward, acquiring Pixar ($7.4 billion), Marvel ($4 billion), Lucasfilm ($4.05 billion), and 21st Century Fox ($71.3 billion) to build the most aggressive IP portfolio in Hollywood history. During his first tenure (2005-2020), Disney delivered a 579% total shareholder return, dwarfing Warner Bros at 244%, Fox at 104%, and Paramount at 49%. After returning as a rescue act following Bob Chapek's failure in 2022, he shouldered the challenge of making Disney+ profitable, and ultimately stepped down after achieving streaming profitability. Yet his biggest blemish remains the succession debacle. Having to go through the failed Chapek experiment before finally handing the reins to D'Amaro is an ironic coda to two decades of empire management.

Josh D'Amaro: From Aspiring Sculptor to Disney's 9th CEO

Josh D'Amaro dreamed of becoming a sculptor as a teenager. He enrolled in Skidmore College's arts program but switched directions in his sophomore year, graduating from Georgetown with a business degree and starting his career in finance at Gillette before joining Disney in 1998. He built his entire 28-year career inside Disney. As VP of Animal Kingdom, he spearheaded the massive Pandora: The World of Avatar expansion. He served as president of Disneyland, then president of Walt Disney World, before becoming chairman of Disney Experiences in 2020, right in the middle of the COVID-19 pandemic. He is the architect behind immersive spaces like Star Wars: Galaxy's Edge, Avengers Campus, and World of Frozen. His Experiences division generated $10 billion in operating income in FY2025, accounting for more than half of Disney's total profits.

Putting an Experience CEO at the Helm of a Content Empire — Strategic Choice or Dangerous Gamble?

Disney's past CEOs have mostly come from content or media backgrounds. Michael Eisner was a programming executive from Paramount, and Bob Iger rose through the ranks at ABC. Breaking that tradition by tapping D'Amaro, who led theme parks, cruises, and consumer products, represents a deliberate pivot by the board. The rationale is clear: Disney Experiences delivered $10 billion in operating income in FY2025, while Disney+ streaming has only just crossed into profitability. The logic is to entrust the whole company to someone who has proven results where the money is made. The question is whether the success formula of theme parks and cruises will translate to content creation and the streaming wars.

The One Disney Strategy and the $24 Billion Content Investment Crossroads

D'Amaro's three stated priorities are creative excellence, technology innovation, and One Disney. The third principle is particularly intriguing — a declaration to connect Disney's dispersed business units (film, TV, streaming, parks, cruises, merchandise) into a single organism. The FY2026 content investment budget is $24 billion, split evenly between sports (ESPN) and entertainment. The fact that ESPN's $29.99/month premium pricing still drives an 80% conversion rate to the Disney+/Hulu/ESPN trio bundle signals that the One Disney strategy is already working.

Disney's Positioning in the $111B Paramount-WBD Merger Era

In the very same week D'Amaro took the CEO chair, another tectonic shift was unfolding in Hollywood. Paramount Skydance is acquiring Warner Bros. Discovery for $111 billion. This came right after Netflix's $83 billion acquisition attempt was derailed by DOJ antitrust concerns. If this merger closes, Hollywood effectively consolidates into a three-power structure: Disney, Netflix, and Paramount-WBD. D'Amaro's Disney enters this new competitive landscape with a dual moat: depth of content library (Marvel, Star Wars, Pixar, Disney classics) and offline experiences (six theme parks, cruises).

Positive & Negative Analysis

Positive Aspects

- A Proven Operator at the Revenue Engine

D'Amaro led Disney's highest-earning division. Disney Experiences' $10 billion operating income in FY2025 exceeded half of the company's total profits. His monetization track record through park price increases, premium services like Genie+, and cruise line expansion is beyond question. In an era of ever-increasing content investment, having a CEO who has actually generated profits is a reassuring signal to Wall Street.

- 28 Years of Insider Organizational Command

Having built his career exclusively at Disney since 1998, D'Amaro has internalized the company's DNA. Considering that one of the reasons for Bob Chapek's failure was his clash with organizational culture, D'Amaro's internal network built across every business unit is a significant asset. His day-one memo stating he spent the best days of his life at Disney rang authentic, and early employee reactions have been positive.

- The Right Leader for the Experience Economy Era

In an era where streaming has become a red ocean, Disney's differentiator increasingly lies in physical experiences. Star Wars hotels, Avatar theme zones, and Disney Cruise expansion represent a strategy of monetizing content IP in the real world — precisely D'Amaro's area of expertise. The fact that he can deepen the offline moat that Netflix and Paramount-WBD cannot replicate gives him temporal fitness.

- Role Division Structure with Dana Walden

To complement D'Amaro's content weakness, Dana Walden, former co-chairman of Disney Entertainment, was elevated to President and Chief Creative Officer. This effectively creates a structure where D'Amaro handles business and Walden handles content. Walden has been a TV content veteran since her Fox days and played a key role in the Disney+ original lineup. A dual leadership structure where each person focuses on their strengths is a pragmatically wise choice.

Concerns

- Concerns About Absence of Content Vision

Iger's greatest strength was his intuition for content. The Pixar acquisition, Marvel Universe expansion, and Disney+ launch all stemmed from deep understanding of the content business. D'Amaro spent most of his 28-year Disney career in parks and resorts. No matter how brilliant an operator, building the next decade's IP strategy requires an entirely different muscle. Delegating creative to Walden is pragmatic, but if the ultimate decision-maker cannot read the pulse of content, Walden cannot move either.

- ROI Pressure on $24 Billion Content Investment

Of the $24 billion FY2026 content budget, half goes to ESPN sports rights and half to entertainment content. Achieving the 10% streaming margin target requires either higher hit rates or lower costs, and neither is easy. With recent Disney films delivering inconsistent box office results, Marvel fatigue and Star Wars directional confusion remain unresolved.

- Cyclical Sensitivity of the Parks Business

The theme park business that underpins D'Amaro's success story is extremely sensitive to economic cycles. The memory of parks shutting down entirely during COVID, shaking all of Disney, remains vivid. At a time when global economic slowdown concerns are growing, the biggest risk for a parks-background CEO is the inertia of overinvesting in familiar territory while neglecting content and streaming.

- Intensifying Survival War in Hollywood's Three-Power Structure

If the Paramount-WBD merger closes, it creates a mega-studio releasing 30 theatrical films annually. Netflix is armed with 325 million subscribers and AI-powered content personalization. If Disney fails to break free from franchise dependence and create new IP in this three-power structure, theme park revenue alone cannot sustain the content war.

Outlook

The ripple effects of Disney's CEO transition will unfold across multiple layers, from short-term stock fluctuations to the long-term structural reshaping of Hollywood.

In the short term, over the next one to six months, Wall Street's focus will be locked onto D'Amaro's first earnings call. When FY2026 Q2 results (January through March) are reported around May, the market will scrutinize streaming margin improvement, ESPN DTC subscriber growth, and park attendance trends. Since Iger-era momentum still carries through this period, dramatic shifts are unlikely, but the tone D'Amaro sets in his first earnings call will determine market confidence. The fact that ESPN's $29.99/month premium pricing is still driving an 80% conversion rate to the Disney+/Hulu/ESPN trio bundle is a positive signal, but whether this momentum sustains through the spring and summer sports seasons is the real question. In terms of stock scenarios, based on Disney's current $176B market cap, a bull case sees a 5-8% rise driven by streaming profitability and park expansion optimism, while a bear case sees a 5-10% decline if economic slowdown fears and content underperformance converge.

In the medium term, six months to two years is where D'Amaro faces his true test. The Paramount-WBD merger will likely clear regulatory review and close during this period, and at that moment, Hollywood officially enters a three-power era. Disney's response strategy will likely branch into three directions. First, a Marvel Cinematic Universe reset. With Marvel fatigue intensifying, how the D'Amaro-Walden regime revitalizes Marvel IP is a critical challenge. Avengers: Doomsday is set for a December 2025 release, and that film's performance will serve as the litmus test for Marvel's future. Second, AI integration. D'Amaro's day-one memo stated the company will embrace technology to unlock new possibilities, which is effectively a declaration to bring AI into Disney's content production and park operations. AI-powered personalization on Disney+, AI character interactions within parks, and AI-automated content production workflows will become concrete agenda items. Third, theme park mega-expansion. Responses to Universal's Epic Universe, expansion of Shanghai and Hong Kong Disneyland, and new cruise ship deployments will proceed sequentially. Capital expenditure for all of this is projected at $8-10 billion annually, and when combined with streaming and content investment, the total outflow exceeds $30 billion per year.

In the long term, looking at a two-to-five-year horizon, D'Amaro-era Disney is likely to see its identity shift from content company to experience platform. This could represent the most significant paradigm shift in Disney's century-long history since Mickey Mouse was born. In the bull case scenario, D'Amaro realizes his One Disney vision, connecting film, streaming, parks, cruises, and merchandise into a single ecosystem where each IP is born on screen and maximizes revenue in physical spaces through a virtuous cycle. AI technology accelerates this connectivity, and Disney+ becomes not just a streaming service but the digital front door to the Disney experience. In this scenario, Disney's market cap could reach $250B-$300B.

In the base case scenario, D'Amaro maintains stable park revenue as a foundation for sustained content investment but shows limited results in creating innovative new IP. Streaming maintains profitability but fails to close the gap with Netflix, and content competition intensifies after the Paramount-WBD merger closes, driving up content investment costs. Disney stays on a trajectory of gradual growth while holding its current position. Market cap at $180B-$220B.

In the bear case scenario, a global economic downturn strikes the parks business directly, shaking Disney's revenue foundation. Marvel and Star Wars franchise fatigue deepens to an irrecoverable level, and as AI lowers content production costs, it paradoxically favors technology companies like Netflix and Amazon. Long-term capital investments tied up in parks become anchors, D'Amaro's lack of content vision materializes, and CEO replacement discussions resurface. Market cap could decline to $120B-$150B.

Here is the essential point. Disney's choice of D'Amaro is both an admission that content alone cannot win the fight and an investment in the hypothesis that experience is the new content. Netflix has 325 million subscribers but no theme parks. Amazon pours billions into Prime Video but cannot build a Disneyland. D'Amaro's Disney carries a dual mandate: maximizing the moat of physical experience while not falling behind in the content war. This is a challenge that exceeds what any single CEO can handle, which is precisely why how well the dual leadership with Dana Walden functions will ultimately determine everything.

Sources / References

- Bob Iger Officially Exits as Disney CEO as Josh D'Amaro Takes Helm — Variety

- Disney's Josh D'Amaro becomes CEO as company embarks on new chapter — CNBC

- As Disney CEO Bob Iger Steps Aside, a Look at His Tenure as a Dynamic, Transformative Leader — Variety

- Josh D'Amaro First Day as Disney CEO Creative Excellence North Star — Variety

- Bob Iger's Next Moves Amid Disney CEO Transition — Deadline

- Disney's Projected $24 Billion Content Spending for 2026 — Variety

- The Paramount-Warner Bros Deal Explained — Variety