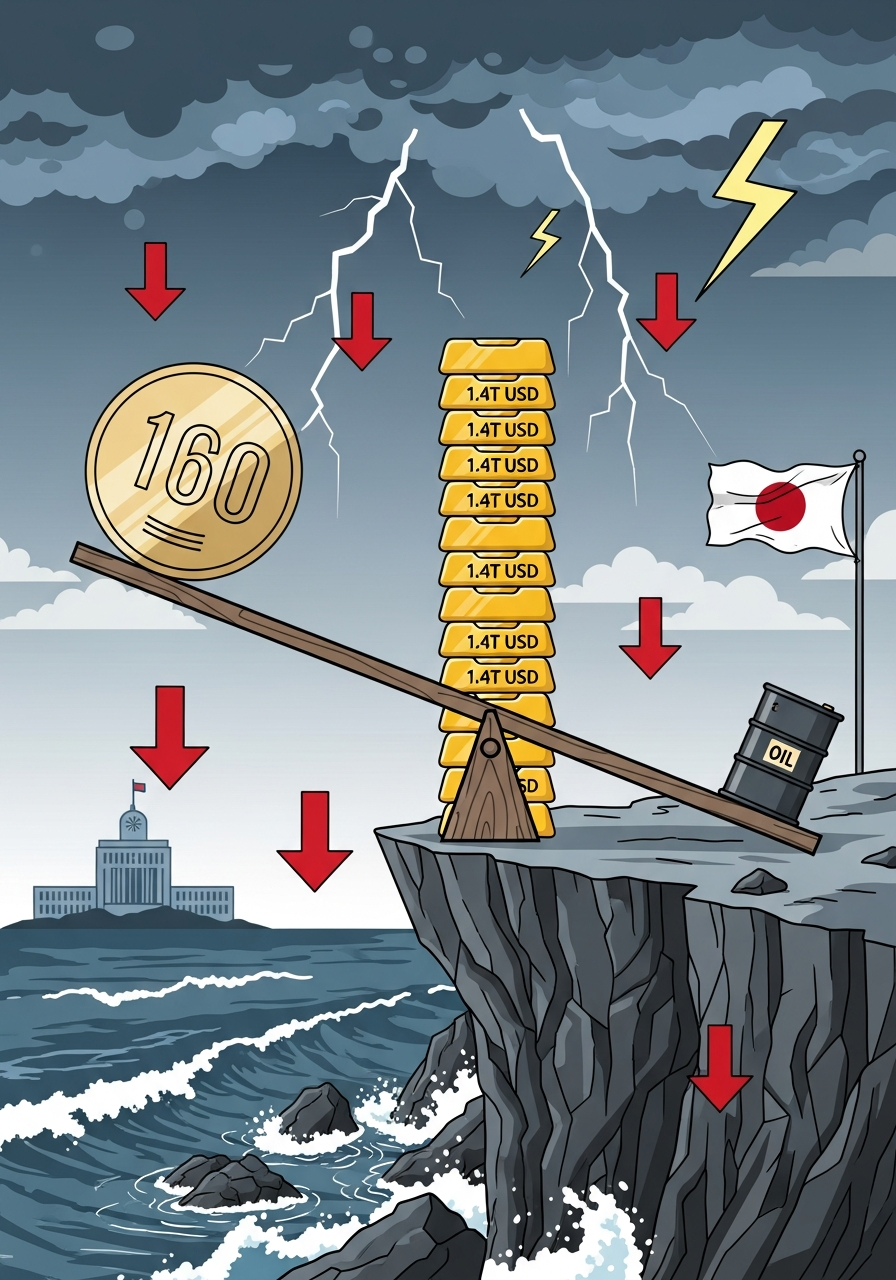

Japan's $1.4 Trillion Gamble from the Edge of 160 Yen

Summary

Japan explores shorting oil futures with $1.4T reserves to defend the yen — an unprecedented gamble facing massive structural risks.

Key Points

An Unprecedented Currency Defense Through Oil Futures Shorting

Japan's Ministry of Finance has been formally sounding out financial institutions on the feasibility of intervening in crude oil futures markets. The proposed mechanism involves leveraging the country's $1.4 trillion foreign exchange reserves to build short positions in oil futures, thereby pushing down crude prices and reducing dollar demand for energy imports — which in turn would ease downward pressure on the yen. No sovereign nation in history has attempted anything like this, making it a radical experiment at the intersection of monetary policy and energy policy. Nikkei reported that this reflects a 'shortage of conventional tools to combat yen weakness,' effectively an admission by Japanese financial authorities that traditional forex market intervention has reached its limits. The target markets under consideration reportedly include WTI on NYMEX, Brent crude on ICE, and Dubai crude futures, with the Ministry of Finance currently in the comparative analysis phase evaluating each market's liquidity and potential impact.

The Double Squeeze: 160 Yen and 90% Energy Import Dependence

With the USD/JPY exchange rate breaching the 160 yen level, Japan's economy finds itself caught in a vicious double squeeze. The country depends on imports for over 90% of its energy needs — nearly all of its crude oil, natural gas, and coal comes from overseas. Rising oil prices increase dollar demand, which further weakens the yen, creating a self-reinforcing downward spiral. The weaker the yen gets, the more expensive it becomes to purchase the same volume of energy, widening the trade deficit with each tick. In 2024, Japan deployed approximately $99 billion in direct forex market intervention, but the effects lasted only a matter of weeks. As long as the structural factor of the US-Japan interest rate differential persists, conventional intervention will remain limited in its effectiveness. Japan's total annual energy import bill runs roughly $137.5 billion (22 trillion yen as of 2025), and every 10-yen depreciation adds billions of dollars in additional costs — a structural vulnerability with no easy fix.

Can $10–20 Billion Actually Move the Global Oil Market?

Analysts estimate that Japan would need to commit at least $10–20 billion to have any meaningful impact on oil prices. Given that global crude oil futures markets see daily trading volumes running into the hundreds of billions of dollars, this amount falls far short of what a single country's unilateral intervention could accomplish. An IG Group analyst pointed out that without physical crude oil supply entering the equation, purely financial instruments cannot move the needle — multilateral cooperation would be essential. In an extreme scenario where oil surges to $200 per barrel, margin calls would rapidly drain Japan's foreign exchange reserves. The $1.4 trillion figure sounds enormous, but against the scale of global crude markets, it is anything but an absolute guarantee of influence.

The Symptom-Treatment Trap — The Real Causes of Yen Weakness Lie Elsewhere

Multiple experts, including the CEO of Yuri Group, have characterized this strategy as 'treating the symptoms.' The fundamental drivers of yen weakness are the US-Japan interest rate differential, the Bank of Japan's ultra-accommodative monetary policy, demographic decline, and chronic fiscal deficits. Energy costs contribute only an estimated 15–20% to yen fluctuations, leaving roughly 80% of the structural causes completely untouched by oil futures intervention. Japan could strengthen the yen by raising interest rates significantly, but doing so would trigger a surge in government bond servicing costs that could destabilize the entire fiscal position — which is precisely why that card remains unplayed. Oil market intervention is a desperate workaround to avoid this dilemma, but it cannot serve as a fundamental solution.

Global Chain Reactions — The Potential Dawn of a Currency-Energy War

If Japan sets the precedent of sovereign-level speculative intervention in oil futures markets, other energy-importing nations could follow suit. South Korea (93% energy import dependence), India (80%+ crude import reliance), and Taiwan are all potential candidates. If multiple governments begin deploying similar strategies, global commodity markets risk being reduced to instruments of national currency warfare. By around 2027, a new agenda item — norms governing state actors' participation in commodity futures markets — is expected to emerge at the G7 or G20 level. This could become the most significant international financial norm discussion since Bretton Woods in 1944. The structural increase in commodity price volatility that would result could paradoxically raise energy costs for every nation involved — the ultimate self-defeating outcome.

Positive & Negative Analysis

Positive Aspects

- Policy Imagination Beyond the Limits of Traditional Forex Defense

After more than three decades trapped in deflation and low growth, the fact that Japan is exploring tools that exist in no textbook represents the boldest policy experiment since Abenomics. When Abenomics was announced in 2013, the dominant reaction was 'this is absurd,' yet it achieved considerable results in its early stages. The very attempt to diversify the policy toolkit could strengthen Japan's crisis-response capacity going forward and opens the door for other nations to consider unconventional policy instruments. Sometimes the audacity of the idea is precisely what forces a reassessment of what is possible.

- Built-in Hedge Function for Energy Import Costs

Short positions in crude oil futures can serve a hedging function for energy import costs independent of the currency defense objective. Japan's annual crude oil imports run approximately $75 billion (10.65 trillion yen as of 2024), and a well-structured futures position would effectively function as insurance against oil price spikes. Even if the yen defense component fails entirely, partial cost savings on energy imports would remain as a tangible benefit. This would essentially add a sovereign-level complement to the hedging strategies already employed by private-sector energy companies — a layered defense that covers gaps the private sector cannot address alone.

- A Powerful Policy-Will Signal to Markets

The mere fact that Japan is considering such a radical measure sends a powerful message to markets: 'We will do whatever it takes to defend the yen.' Much like ECB President Mario Draghi's famous 'whatever it takes' speech in 2012 that single-handedly calmed the eurozone crisis, there are cases where the expression of policy will has a greater impact than the policy itself. The psychological deterrent effect against speculative yen short-sellers should not be underestimated — when a government signals willingness to deploy unconventional weapons, it changes the risk calculus for every trader on the other side. Hedge funds and institutional speculators who have been aggressively shorting the yen would need to factor in an entirely new category of sovereign risk, potentially forcing position unwinds even before Japan takes any concrete action.

- A Catalyst for Policy Innovation Among Energy-Importing Nations

Japan's initiative could prompt countries with similarly high energy import dependence — South Korea, India, Taiwan — to examine comparable policy tools. If this eventually leads to a coordinated response framework among Asian energy importers, the result could be collective bargaining power in crude oil markets. Such a coalition would function as a counterweight to OPEC on the demand side, potentially reshaping the power dynamics of global energy pricing in ways that benefit importing nations for the first time in decades. The collective energy import bill of these Asian nations exceeds $400 billion annually, giving a unified bloc genuine market-moving leverage that no single country could achieve alone.

- Political Momentum for Accelerating the Energy Transition

The controversy surrounding oil futures intervention lays bare the vulnerability inherent in fossil fuel dependence and strengthens the political case for energy transition policies: nuclear reactor restarts, expanded renewable energy investment, and restructured long-term LNG contracts. It could help build the social consensus needed for Japan's goal of reducing energy import dependence to the 80% range by 2030. History repeatedly shows that crisis drives structural reform — and this episode provides exactly the kind of political cover that makes difficult energy policy decisions easier to push through. Public opinion that previously resisted nuclear restarts or large-scale renewable subsidies may shift decisively when the alternative is staking the nation's financial stability on commodity market speculation.

Concerns

- Theoretically Unlimited Loss Exposure on Rising Oil Prices

Short positions in crude oil futures carry theoretically unlimited downside exposure if prices rise. A full-scale Middle Eastern conflict that sends crude to $150–200 per barrel could generate losses measured in the tens of billions of dollars. Considering Japan already burned through roughly $99 billion in forex intervention in 2024, losses from oil market positions could vastly exceed that figure. The rapid depletion of foreign exchange reserves would trigger a domino effect that undermines confidence in the Japanese economy as a whole — the very outcome this strategy is designed to prevent.

- Corruption of Price Discovery in Global Oil Markets

No central bank in history has entered crude oil futures markets with speculative intent — this would be an absolute first. Even Nikkei's own reporting raised concerns that 'the market's basic function of supply-demand adjustment could be compromised.' The crude oil market is the lifeblood of the global economy, and distorting it for one country's currency defense creates negative ripple effects across the entire global energy supply chain. If other nations launch retaliatory interventions, market chaos would escalate exponentially, with no clear mechanism to restore order.

- Unaddressed Structural Causes — The Limits of 'Symptom Treatment'

The fundamental drivers of yen weakness — the US-Japan interest rate differential, BOJ's ultra-accommodative policy, demographic decline, and chronic fiscal deficits — cannot be resolved through oil futures positions. Energy import costs account for only 15–20% of yen fluctuation factors, with the remaining 80% of structural forces continuing to push the yen lower regardless. The Yuri Group CEO's assessment of this as 'symptom treatment' is a precise diagnosis. Attempting to paper over structural problems with financial instruments is simply not sustainable over any meaningful time horizon.

- Risk of Retaliatory Production Cuts by OPEC+

If OPEC+ member states respond to Japan's large-scale short positions with additional production cuts, the resulting supply squeeze could actually push oil prices higher — the exact opposite of the intended effect. Oil-producing nations have far stronger incentives and far more powerful tools to defend crude prices, which are directly tied to their fiscal revenues. Saudi Arabia alone holds more than 2.5 million barrels per day of spare production capacity that it deploys strategically. Any financial intervention by Japan can be easily offset by physical supply adjustments from the producing side.

- International Backlash and Financial Norm Violations

A sovereign state entering commodity futures markets with speculative intent for currency defense purposes does not align with existing international financial norms. The United States and Europe are highly likely to view this as market manipulation and apply pressure accordingly. Japan's standing within the G7 could be weakened, and the risk of being placed on the US Treasury's currency manipulator watchlist is real. Bloomberg's reporting also noted that this approach 'raises questions about international financial norms' — a diplomatically worded warning that Japan would be crossing a line with consequences.

Outlook

Let's start with what is likely to happen in the next few months. The fact that the Ministry of Finance is sounding out financial institutions tells us that no concrete execution plan has been finalized yet. I expect a clearer outline to emerge during Q2 2026 — somewhere between April and June. The Ministry will need at least two to three months to determine a feasible scale, select target markets (whether to concentrate on WTI, Brent, or Dubai crude), and decide on position entry timing.

During this process, markets will begin reacting well before any actual positions are built. The mere possibility that 'Japan might short crude oil' could increase oil futures market volatility by 20–30%. Speculative traders will attempt to front-run or counteract Japan's anticipated positions, which would paradoxically amplify the very price swings Japan is trying to suppress. In the short term, the yen might rally 1–2%, but this would be a sentiment-driven blip rather than a structural reversal. Meanwhile, OPEC+ will not respond immediately, but behind closed doors they will be monitoring Japan's moves closely and preparing production-cut adjustment cards for deployment in the second half of 2026. The energy policy line led by Saudi Crown Prince Mohammed bin Salman has strong incentives to keep crude above $80 per barrel, and if Japan's futures shorting becomes reality, Saudi Arabia can leverage more than 2 million barrels per day of spare capacity to pressure Japan's positions.

Looking six months to two years out, the picture gets considerably more complicated. If Japan actually begins building crude oil futures positions, this moves beyond simple currency policy and opens an entirely new chapter in international financial order. I expect that between the second half of 2026 and some point in 2027, a new agenda item will surface at the G7 or G20 level: norms governing sovereign participation in commodity futures markets. The United States and Europe are likely to frame this as market disruption and push back hard against Tokyo. The US Commodity Futures Trading Commission (CFTC) could impose enhanced reporting requirements on large positions tied to Japanese government accounts, or even apply position limits. These regulatory responses have the potential to shut down Japan's strategy entirely before it gains any traction.

What makes this even more interesting is the potential reaction from other Asian energy importers. South Korea's energy import dependence sits at roughly 93%, comparable to Japan's, while India relies on overseas sources for more than 80% of its crude oil. The possibility that these nations benchmark Japan's strategy or explore joint responses is realistic and cannot be dismissed. By around 2027, we might see movements toward an 'Asian energy importer coalition' aiming to establish collective price-bargaining power in crude markets. If such a coalition materializes, the power dynamics of the oil market itself would shift fundamentally. That said, the practical barriers to forming such an alliance are substantial — divergent political interests among member nations, varying alliance relationships with the United States, and differences in energy mix composition all present significant hurdles.

However, I believe the realistic scenario is more probable than the optimistic one. There is a better than 50% chance that the Bank of Japan will implement additional rate hikes between the second half of 2026 and early 2027. The BOJ's benchmark rate currently sits at 0.75% — the highest since 1995 following the March 2026 hold decision — and raising it to 1.0–1.5% would narrow the US-Japan rate differential enough to ease fundamental pressure on the yen. In that scenario, the oil futures intervention strategy would be quietly shelved as 'a card that was no longer needed.' The yen would likely stabilize in the 150–155 range, though a return to the 140s would require both rate hikes and energy price stabilization to occur simultaneously. The critical variable here is the pace of BOJ rate increases. Move too fast and the Japanese government bond market destabilizes; move too slow and the yen defense proves ineffective. The most probable path is a gradual quarter-point-per-meeting approach, which means it would take at least 12–18 months before the yen sees meaningful stabilization.

Zooming out to the two-to-five-year horizon, the legacy of this episode may prove larger than it appears right now. Even if Japan never executes the oil futures intervention, the mere fact that this discussion took place could mark the starting point of a new policy paradigm: the fusion of monetary policy and energy policy. By 2030, Japan aims to reduce its energy import dependence to the 80% range, which will require accelerating nuclear reactor restarts, expanding renewable energy investment, and restructuring long-term LNG contracts. The oil futures intervention controversy serves to strengthen the political mandate for these energy transition investments — an ironic but valuable side effect.

From a broader perspective, by 2028–2030 we could see serious discussions around linking a digital yen to energy settlement systems. Japan may attempt to use a central bank digital currency (CBDC) to reduce its dependence on dollar-denominated energy import payments. This would be a far more structural and long-term solution than oil futures intervention. Of course, such a move would also be interpreted as a challenge to dollar hegemony and would draw pushback from Washington. Combined with China's ongoing push to internationalize the yuan, this could create a scenario where multiple simultaneous challenges to the dollar settlement system unfold in parallel — a development that goes beyond simple currency wars to represent a structural reordering of the international financial architecture.

Let me break this down into scenario analysis. The bull case looks like this: Middle Eastern tensions ease and crude oil drops to the $60–70 per barrel range while the BOJ raises rates to 1.5%. Under these conditions, the yen recovers to the 140 range and the oil futures intervention plan is scrapped at the review stage. Japan's economy benefits from the dual tailwinds of a stable yen and reduced energy costs, with the current account balance improving materially. I put this scenario at about 20% probability. In this case, Japan's GDP growth could recover to 1.5–2.0% in 2027, the Nikkei could set new all-time highs, and foreign investment capital would flow back in.

The base case — and the most likely scenario at 50% probability — is that Japan builds small, experimental oil futures positions but fails to move the market in any meaningful way. A limited intervention in the $5–10 billion range might push oil prices down 2–3%, but the yen would continue oscillating in the 150–160 range. Combined with the BOJ's gradual rate hikes, the yen would avoid extreme weakness but a return to the 130–140 range would remain out of reach. Japan would accelerate its energy transition investments while searching for medium-to-long-term solutions. On this path, Japan's current account would gradually improve from a slight deficit toward balance, but the structural burden of energy import costs would remain at roughly 3–4% of GDP. What is worth noting about this base case is the signaling effect. Even a failed or underwhelming intervention would demonstrate Japan's willingness to cross traditional policy boundaries, and that alone might deter the most aggressive yen speculators from pushing beyond the 165 mark.

There is also a dimension to this story that deserves dedicated attention: the institutional mechanics. If Japan proceeds, the execution would almost certainly flow through the Government Pension Investment Fund (GPIF) or a newly created special purpose vehicle, rather than the Bank of Japan directly. The BOJ taking direct futures positions would create an unprecedented conflict of interest between its monetary policy mandate and market participation. Using a separate entity provides legal and operational cover, but it also introduces layers of bureaucratic complexity that could slow execution to the point of irrelevance. In commodity futures markets, timing is everything — a sovereign actor that needs three layers of approval before adjusting a position is a sovereign actor that will consistently be late to the trade. The institutional design question is arguably as important as the strategic question, and the Ministry of Finance's consultations with financial institutions are reportedly focused as much on execution architecture as on market impact modeling.

Now for the bear case. A full-scale military conflict erupts in the Middle East and the Strait of Hormuz faces a blockade crisis. Crude oil spikes to $150–200 per barrel and Japan's short positions generate losses in the tens of billions of dollars. Foreign reserves drain rapidly as the yen plummets to the 170–180 range. In this scenario, turmoil spreads to the Japanese government bond market and the specter of a 'Japan financial crisis' becomes real. Just as the Russian ruble crisis shook global financial markets through the 1998 LTCM collapse, financial instability in Japan — the world's third-largest economy — could trigger a domino effect across Asia and indeed the entire global financial system. I put this scenario at 30% probability, which is far too high to dismiss. The current uncertainty in Middle Eastern geopolitics and the prolonged instability of global energy supply chains stemming from the Russia-Ukraine war are structurally elevating the probability of this bear case — a fact that should not be overlooked.

One final dimension of this outlook deserves attention: the chain reaction effect. If Japan sets the precedent of sovereign-level intervention in oil futures markets, it would be the equivalent of opening Pandora's box. What happens when India follows suit, South Korea starts reviewing similar options, and the EU tries something analogous in natural gas markets? The worst-case endgame is a world where global commodity markets devolve into instruments of national currency warfare. In such a scenario, structural commodity price volatility increases permanently, and the ultimate irony materializes — energy costs rise for every single country involved, including the ones that started the interventions. I put the probability of this 'currency-energy war' scenario materializing between 2028 and 2030 at roughly 15–20%.

There is a historical parallel worth considering here. In the 1990s, the Asian Financial Crisis demonstrated what happens when individual nations attempt to defend their currencies against market forces through reserve depletion. Thailand, South Korea, and Indonesia all burned through their reserves before eventually capitulating to market reality. Japan's proposed oil futures intervention carries echoes of that era — a sovereign actor deploying finite financial resources against structural market forces that operate on a fundamentally different scale. The critical difference is that Japan's reserves are vastly larger and its economy far more developed, but the underlying dynamic of fighting the current rather than redirecting it remains troublingly similar.

For investors and market participants watching this unfold, the practical implications are clear. Crude oil implied volatility will likely command a sustained premium as long as Japan's intervention remains on the table — pricing in the tail risk of sovereign participation on the short side. Japanese government bond markets will also reflect the uncertainty, with the 10-year JGB yield potentially testing the BOJ's yield curve control ceiling more aggressively as traders price in the fiscal risk of potential intervention losses. For the yen itself, the irony is that the intervention discussion may provide more support through uncertainty than any actual positions ever could — because once positions are established and their size is estimated by the market, they become a target rather than a deterrent.

At its core, this issue comes down to a fundamental question: is it justified — and is it even effective — for one nation to attempt privatizing a global public good like the energy market in order to defend its exchange rate? The answer, in my assessment, is that the strategy is far more valuable as a threat than as an action — and Japan's policymakers may already understand this better than anyone.

Sources / References

- Japan Is Said to Sound Out Market on Oil Futures Intervention — Bloomberg

- Japan Shifts Focus to Oil in Unorthodox Yen Defense — Yahoo Finance / Reuters

- Japan Explores Oil Futures Intervention — Sounds Out Financial Institutions on Feasibility — Nikkei

- Yen Defense: Japan Plans to Directly Short Crude Oil Futures — TradingKey

- Panicking Japan Considers Shorting Oil to Prop Its Crashing Currency — ZeroHedge

- Japan Considers Unconventional Crude Oil Futures Intervention to Stem Yen Decline — Markets.com

- Japan Eyes Oil Futures Intervention to Stabilize Yen Amid Middle East Crisis — EconoTimes

- JPY/USD: How Japan Can Use the Oil Market to Support Weak Yen — Bloomberg