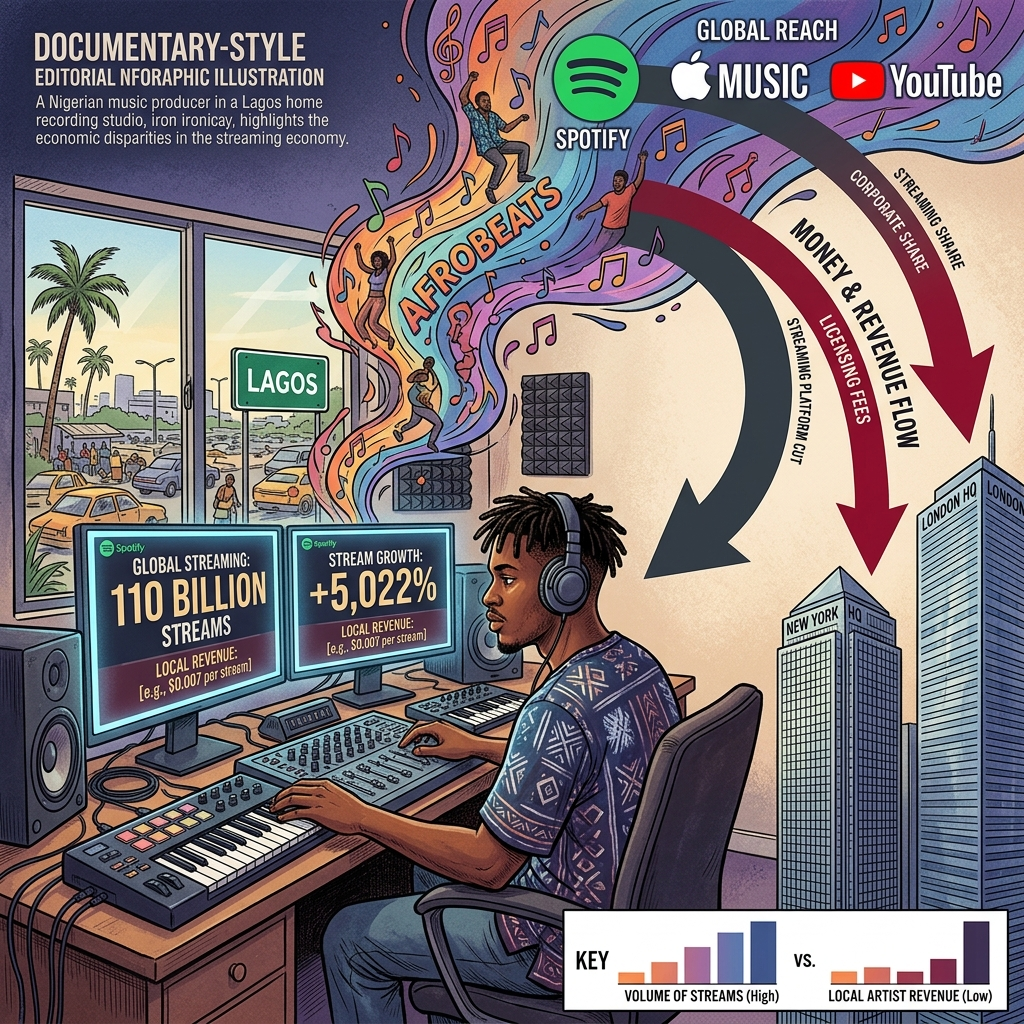

Congrats on 5,022% Streaming Growth — Africa Gets 0.37% of the Money

Summary

Afrobeats streaming surged 5,022% between 2021 and 2025, cementing the genre's status as a dominant force in global music alongside K-pop and Latin pop, with Wizkid becoming the first African artist to surpass 11 billion career Spotify streams in early 2026. Despite this explosive cultural momentum, Sub-Saharan Africa's share of the $29.6 billion global recorded music market in 2024 amounted to just $110 million — 0.37% — a figure that barely moved to 0.38% of a $31.7 billion market by 2025. A structural 10x per-stream royalty gap, embedded in Spotify's subscription-price-proportional payout model, means Nigerian artists earn $300–$400 per million streams while the same streams in the United States generate $3,000–$4,000. Three foreign conglomerates — Empire, Sony Music, and Universal Music Group — control 68% of Nigeria's streaming volume, and $286 million in annual music royalties goes unclaimed in Nigeria and Kenya alone due to failed collective management infrastructure. Harvard University's CSASE report, released in December 2025, concluded that the Afrobeats boom is generating revenue almost everywhere except the continent that created it — a structural paradox that time and market growth alone cannot resolve.

Key Points

The 5,022% Streaming Paradox vs. the 0.37% Revenue Reality

Afrobeats has recorded 5,022% streaming growth on Spotify from 2021 to 2025, rising alongside K-pop and Latin pop to become one of the defining genres of global music in the 2020s. Wizkid became the first African artist to surpass 10 billion career Spotify streams in January 2026 — now at 11 billion and climbing — while Burna Boy follows at 9.5 billion streams. Yet according to IFPI's 2025 Global Music Report, Sub-Saharan Africa's share of the $29.6 billion global recorded music market in 2024 was just $110 million — 0.37%. By 2025, the region had grown to $120 million out of a $31.7 billion global market, but its share barely moved to 0.38%, even as Africa's 22.6% growth rate outpaced the global average of 4.8% by nearly five times. Africa is home to 18% of the world's population, making its 0.37% music revenue share a 25x undervaluation relative to population weight alone. The growth rate of 22.6% sounds impressive until you run the arithmetic: 22.6% of $110 million produces roughly $25 million in new revenue, while the global market's 4.8% growth produces roughly $1.4 billion — the absolute gap widens every year, not narrows. Spotify's February 2026 five-year Nigeria anniversary report celebrated the streaming explosion in promotional detail while including zero royalty distribution data — a telling asymmetry that symbolizes the broader paradox: cultural credit without economic return.

The Geographic Penalty — 10x Royalty Gap for the Same Song

Burna Boy disclosed publicly in April 2025 that one million streams in Nigeria yields $300 to $400 in royalties, while the same one million streams in the United States or United Kingdom generates $3,000 to $4,000. This factor-of-ten disparity is not a platform error or market anomaly — it is structurally embedded in Spotify's subscription-price-proportional royalty model, which ties per-stream payouts directly to local subscription prices. Nigeria's premium subscription costs $1.08 per month; the United States premium costs $10.99 per month. When subscriptions are priced one-tenth as high, royalties follow by design. Ecofin Agency's analysis confirmed that African artists receive 55 to 77% less per stream than their North American and European counterparts, and crucially, this gap is structurally fixed — it does not improve as Africa's streaming growth rate climbs. South Africa, the wealthiest music market on the continent, still sees 100 million streams return only $1,568 — less than half the U.S. equivalent. A music video connected to the Africa Cup in Côte d'Ivoire generated 10 million views but returned just 971 euros to its creator, a case study in the severity of the geographic royalty penalty in practice. This mechanism is not neutral market pricing — it is a structural tax on being an artist whose audience lives in a lower-income country, a system that permanently undervalues creative work based on geography rather than on the quality or cultural impact of the work itself.

Foreign Label Control at 68% and the Master Rights Trap

Empire, Sony Music, and Universal Music Group collectively controlled 68% of Nigeria's total streaming volume as of 2025, making them the dominant arbiters of how Afrobeats revenue flows globally — and flows away from Africa. African artists seeking international distribution must, as a practical matter, work with one of these three companies, and doing so typically requires surrendering master rights as part of the deal structure. Even celebrated artists like Wizkid and Burna Boy reportedly transferred masters to labels like Sony and Atlantic when signing international contracts, which means that as their music becomes more culturally valuable over time, the long-term revenue accrues increasingly to label headquarters in New York and London rather than to the artists themselves. Harvard University's CSASE report noted that the Big Three labels, alongside platforms like Spotify, YouTube, and TikTok, monopolize distribution infrastructure, royalty accounting systems, data ownership, algorithmic visibility, and licensing relationship networks. UMG's 2024 acquisition of a stake in Nigeria's Mavin Global was simultaneously a validation of African music IP value and a further extension of foreign capital's structural control — a dual reality that makes "international investment" a complicated gift for African creators. Independent artists and newcomers face even weaker negotiating positions and surrender masters at higher rates with almost no leverage to negotiate favorable terms. The architecture of this system structurally parallels colonial resource extraction: Africa produces the raw material, the West controls processing and distribution, and the profits repatriate to Western shareholders.

CMO Infrastructure Collapse and the $286 Million Black Hole

CISAC's 2025 Global Collections Report found that all African CMOs combined collected only 90 million euros in royalties — 0.7% of the global total — while research estimates Nigerian artists' international royalty collection rate sits below 5% of what they are owed. In Nigeria and Kenya alone, an estimated $286 million in annual music royalties goes unclaimed each year, the result of metadata mismatches, unregistered artists, and the absence of functioning international reciprocal collection agreements. Kenya's Music Copyright Society had its operating license revoked between 2025 and 2026, rendering collection and distribution legally impossible during a critical period of industry growth. South Africa's SAMRO is simultaneously undergoing a forensic audit over governance and alleged fraud, and Nigeria's MCSN faces ongoing disputes among competing CMO structures that reduce operational efficiency and artist trust. The compounding systemic failure here is that uncollected royalties held without successful matching for three to five years are redistributed to existing registered rights holders based on market share formulas — formulas that inherently favor Western rights holders with larger registered portfolios, effectively transferring African artists' money to foreign rightsholders by default. Prince Nshogoza of Rwanda's Dajah Group captured the human reality: "Rwandan artists have for years received compensation for only half of their works. The composing revenue was just evaporating internationally." Nigeria's 2025 Collective Management Regulations represent a necessary legislative step, but building functional CMO infrastructure from a degraded baseline typically requires five to ten years of sustained implementation work before artists see material improvements in royalty receipt rates.

The Streaming Democratization Myth and the Structure of Digital Colonialism

The narrative that streaming platforms democratized global access for African music is factually true but strategically incomplete in a way that obscures more than it reveals. Spotify's five-year Nigeria report detailed the 5,022% streaming surge in extensive promotional terms while omitting every line of royalty distribution data — an asymmetric transparency that captures the essential dynamic: claim the cultural credit, conceal the economic structure. Nigeria's music industry generated approximately $600 million in total revenue in 2024, but 65.7% came from live performance and touring, not streaming — streaming royalties accounted for just 30.1% of total revenue. This breakdown proves that for African artists, streaming functions primarily as a promotional mechanism rather than a genuine income stream, which is precisely the inverse of what streaming's democratization narrative promised. Burna Boy's "Love, Damini" world tour grossed approximately $40 million across 12 countries and 600,000 fans — a figure that dwarfs what streaming contributed to his annual income in the same period. The Creative Brief Africa's formulation is apt: "Music flows. Audiences listen. But money doesn't flow efficiently." I read this not as market inefficiency but as the digital incarnation of the same structural logic that governed 19th-century resource colonialism — Africa's creative output enriches distant platforms and label headquarters, and the wealth generated does not return to Lagos, Accra, or Nairobi in proportion to the cultural value created there.

Positive & Negative Analysis

Positive Aspects

- Explosive Global Visibility for African Music at Unprecedented Scale

The most concrete and undeniable benefit Afrobeats has gained from streaming is global visibility at a scale that was structurally impossible for African music before the platform era. The 5,022% streaming surge has propelled Afrobeats into the same conversation as K-pop, Latin pop, and reggaeton as one of the world's recognized non-English language genre forces. Wizkid's 11 billion Spotify streams prove that an African artist can compete at the absolute top tier of global music, which opens commercial and creative doors that were structurally closed before streaming existed at all. This visibility translates directly into revenue opportunities well beyond streaming itself — brand sponsorships, global festival headline slots, Hollywood and Netflix soundtrack placements, and luxury brand partnerships that generate significant income independently of per-stream royalty rates. Burna Boy's ability to sell 600,000 tickets across a world tour was only possible because Afrobeats streaming had built his global recognition to critical mass over years of cumulative exposure. While streaming royalties themselves fall far short of fair economic compensation for the value they help create, their function as the foundation for indirect revenue generation and as the mechanism that inscribed Africa onto the global cultural map represents a genuine transformation of what African music can commercially achieve.

- Overall Growth of Nigeria's Music Industry Ecosystem and Employment

The Afrobeats streaming boom is functioning as a rising tide for Nigeria's broader music industry ecosystem well beyond individual artist revenues. Nigeria's music industry reached approximately $600 million in total revenues in 2024, creating direct and indirect employment for more than 4.2 million people across production, management, marketing, creative services, and live event infrastructure. Spotify's Nigeria five-year report noted a 158% increase in the number of Nigerian artists registered on the platform — a clear signal that music remains an attractive professional pathway even for emerging artists who understand the royalty economics clearly. The live performance market has grown in direct tandem with streaming visibility, with Lagos's Detty December festival season in December 2024 drawing over one million attendees across music events and creating significant economic activity across hospitality and services industries. Recording studios, content production houses, music technology companies, and social media management services have all expanded rapidly, creating a thicker and more resilient industry infrastructure than existed before the streaming era. This ecosystem growth, however uneven in its distribution of financial rewards, creates a structural foundation that makes it harder for the industry to regress even in challenging economic periods, and provides meaningful employment to millions of Nigerians beyond the artists themselves.

- International Investment Capital Beginning to Recognize African Music IP Value

The Afrobeats global success story is attracting institutional and strategic capital into African music infrastructure in ways that represent a genuine structural shift, even if the dynamics of that investment carry their own complications. UMG's 2024 acquisition of a stake in Mavin Global was the most visible signal that international capital markets are formally beginning to value African music intellectual property — not just streaming play counts, but underlying IP with compounding long-term commercial potential. Afreximbank's CANEX Creative Industries Fund has been expanded to $1 billion, directing institutional capital toward creative economy infrastructure across the continent's major markets. An IFC-Sony Creative Sector Partnership has launched with explicit goals around digital infrastructure development and music industry workforce training. These capital flows, even when they carry the complexity of foreign ownership stakes identified earlier as structurally problematic, do fund recording infrastructure, digital distribution capacity, and skills programs that benefit the broader ecosystem. AfroSoundtrack's success in recovering unclaimed royalties for over 50 artists by building proper rights management and metadata infrastructure demonstrates that targeted investment in the mechanics of rights administration can directly and meaningfully improve artist incomes — a proof of concept for what larger, coordinated investment could achieve at the industry level.

- Institutional Reform Momentum Building Across Policy and Industry Levels

Greater international attention on the Afrobeats revenue paradox is generating reform momentum at policy, industry, and advocacy levels that is more concrete and better organized than at any previous moment in African music history. Nigeria's 2025 Collective Management Regulations provide a formal legal framework for CMO transparency requirements and operational efficiency standards — a legislative foundation without which systemic reform cannot begin at all. Harvard's CSASE report laid out five specific policy priorities for Africa's creative economy: regional creative economy regulations, updated intellectual property models, live market development infrastructure, data systems investment, and financial ecosystem reform — an unusually actionable and evidence-backed framework for a problem of considerable complexity. CISAC has formally recognized African CMO capacity-building as a global organizational priority and is actively expanding its network of international reciprocal agreements to cover more African territories and rights categories. The contrast with five years ago is meaningful: the problem has moved from being inadequately documented to being defined with verified data, attributed to specific structural mechanisms, and addressed with concrete legislative and industry proposals. This transition from problem recognition to actionable reform agenda is the necessary precondition for real structural change.

Concerns

- Structural Entrenchment of the Geographic Royalty Penalty Shows No Path to Self-Correction

The 10x royalty gap between Nigeria ($300–$400 per million streams) and the United States ($3,000–$4,000) is not a market distortion that competition, growth, or time will naturally correct — it is engineered into the subscription-price-proportional payout model that Spotify and most major streaming platforms apply globally. Nigeria's per capita GDP of approximately $2,000 makes it economically impractical to raise subscription prices to U.S. levels, and even incremental price increases risk driving subscriber churn in a market where the overwhelming majority of listeners use free tiers rather than paying for premium access. Ecofin Agency's confirmed 55 to 77% per-stream payout deficit for African artists is not expected to narrow meaningfully under the current structural model regardless of how rapidly Africa's streaming growth rates climb. The optimistic reading — that Africa's 22.6% growth rate will eventually close the gap — ignores the arithmetic reality that 22.6% of $110 million produces far less absolute revenue than 4.8% of $29.6 billion, and the absolute gap widens every year. South Africa's relatively higher-income streaming market still yields only $1,568 per million streams compared to the U.S. equivalent, demonstrating that the structural penalty is endemic across the entire continent regardless of local income levels. This is not a gap that market forces will heal organically — it is a gap that requires deliberate platform policy intervention that no major streaming company has yet publicly committed to making.

- Foreign Label Master Rights Monopoly Compounds Revenue Outflows Over Time

Empire, Sony Music, and Universal Music Group's combined 68% control of Nigeria's streaming volume means that as Afrobeats grows commercially, the revenue acceleration disproportionately benefits foreign corporations rather than the African creators whose work drives that growth. Artists who surrender master rights in exchange for distribution access lose perpetual control over their music's long-term economic value — and as cultural works appreciate over decades, the financial returns increasingly flow to label headquarters rather than to artists. Even Wizkid and Burna Boy, as global superstars with significant negotiating leverage, reportedly transferred master rights when signing with Atlantic and Sony internationally, which means their music's legacy revenues — the streams that will accumulate as they become historical figures — are not primarily theirs to collect. For independent artists and newcomers without superstar leverage, master rights surrender rates are typically even more unfavorable, and the terms of such contracts are rarely made public. UMG's 2024 Mavin Global stake acquisition, while representing formal recognition of African music IP value, simultaneously deepens foreign capital's structural control over the continent's most commercially successful music infrastructure. The African creative economy generating raw material processed and monetized abroad, with profits repatriated to foreign shareholders, replicates with digital precision the extractive economic colonial relationships that shaped Africa's economic development in earlier centuries.

- Simultaneous CMO Infrastructure Collapse Across Multiple Key Markets

Africa's collective management organization crisis is not isolated to one country — it is occurring simultaneously across the continent's largest and most economically significant music markets in ways that compound the damage severely. Kenya's MCSK, covering East Africa's most significant music economy, has had its operating license revoked, making royalty collection and distribution legally impossible during a critical period of industry growth. South Africa's SAMRO, the continent's most technically sophisticated CMO, is undergoing a forensic audit over serious governance and fraud allegations that have undermined artist trust and operational confidence. Nigeria's MCSN operates under ongoing internal disputes among competing CMO structures that reduce efficiency and create uncertainty for artists attempting to register works and claim royalties. The compounding systemic effect is severe: uncollected royalties that remain unmatched for three to five years are redistributed to existing registered rights holders based on market share formulas that inherently favor Western rights holders with larger pre-existing registered portfolios, permanently transferring money owed to unregistered African artists to other parties by bureaucratic default. The $286 million annual unclaimed royalty figure for Nigeria and Kenya alone therefore continues accumulating each year rather than being reduced. Nigeria's 2025 Collective Management Regulations are a necessary but insufficient legislative response — building functional CMO infrastructure from a degraded baseline typically requires five to ten years of sustained, well-funded implementation before artists see material improvements.

- AI-Generated Music Threatens to Dilute an Already Inadequate Royalty Pool

The AI-generated music problem represents a structural threat layered on top of existing structural disadvantages, and it affects African artists disproportionately relative to their already marginal royalty position within the global system. Deezer's January 2026 disclosure that it receives 60,000 AI-generated tracks per day — with 85% accompanied by anomalous streaming patterns consistent with artificial play inflation — signals that royalty pool dilution from AI content is already occurring at industrial scale. Afrobeats' highly distinctive sonic patterns, rhythmic structures, and melodic conventions are precisely the kind of clearly identifiable genre fingerprints that make it especially susceptible to AI replication and mass production of near-identical content designed to capture genre-associated algorithmic placement. As AI-generated Afrobeats-style tracks flood streaming platforms, the royalty pool gets distributed across a vastly larger number of tracks, and each authentic African artist's per-stream share deteriorates further from an already inadequate baseline. Africa's underdeveloped CMO infrastructure means that the continent lacks the technical and administrative capacity to identify, systematically challenge, and exclude AI-generated content from royalty calculations — leaving African artists exposed without the protective mechanisms that more developed markets are beginning to implement. Harvard CSASE's warning about structural income losses driving talented African artists away from music careers becomes a dramatically accelerated timeline when combined with an AI content wave that further compresses the already insufficient earnings available to non-superstar creators.

- Next-Generation Music Talent Drain Threatens Long-Term Cultural Sustainability

The economic reality facing non-superstar African artists — $300 to $400 per million streams in Nigeria, barely enough to cover a month's rent in Lagos — is increasingly driving talented young musicians to abandon music careers before they can fully develop their craft or establish sustainable professional trajectories. In Nigeria, generating a livable income from streaming alone requires achieving hundreds of millions of streams per year, a threshold accessible only to the top fraction of one percent of artists on any platform. For the vast majority of talented but developing artists, 100 million streams in Nigeria returns roughly $3,000 to $4,000 annually — less than a living wage by any reasonable standard applied to a major urban market. Harvard CSASE's explicit warning that structural income losses risk driving the next generation of African artists to abandon music careers is supported by emerging reports from Lagos and Abuja of young musicians actively transitioning to technology, fintech, and professional services because the economic math of streaming simply does not work for creators who haven't yet achieved superstar status. This talent drain represents an existential threat to the cultural sustainability of Afrobeats itself: the genre's creative vitality depends on continuous generational renewal, on new producers, vocalists, and songwriters entering the ecosystem with energy and ambition. If the structural economic conditions prevailing today continue for another decade without meaningful reform, Afrobeats risks becoming a legacy genre sustained by established names while the pipeline of emerging talent dries up — an irreversible cultural loss that no amount of retroactive royalty correction could undo.

Outlook

The next six months will almost certainly make this paradox more visible and politically charged than it's been at any point in Afrobeats' history. The second half of 2026 is expected to bring an IFPI mid-year report and additional Spotify data releases that could, for the first time, place geographic royalty disparities under formal international scrutiny. Nigeria's Collective Management Regulations, passed in 2025, are entering full implementation in the second half of 2026 — which could represent the beginning of incremental efficiency gains at MCSN and other local CMOs. That said, I'd caution against overestimating near-term impact. Policy on paper and operational infrastructure on the ground are separated by years of implementation work. Kenya's MCSK license revocation is a vivid reminder of how fragile CMO governance in Africa truly is, and South Africa's SAMRO forensic audit signals that the continent's two most significant music economies are both navigating CMO governance crises simultaneously. My best estimate is that Nigerian artists' international royalty collection rates could edge up from under 5% today to somewhere around 7 to 8% by end of 2026 — meaningful directional progress, but nowhere near proportional to the genre's actual global commercial footprint.

Another short-term variable worth watching closely is Spotify's Africa pricing strategy. Nigeria's $1.08 per month premium subscription is among the lowest in the world — a price point that made sense during Spotify's user-acquisition phase but becomes increasingly difficult to justify as the platform shifts toward monetization. Spotify raised prices in India roughly three years after entering that market, and a similar pattern could realistically emerge in Africa between 2026 and 2027. If Nigerian subscription prices climb from $1.08 to somewhere in the $2 to $3 range, per-stream royalties would improve proportionally. But there's a genuine danger: price increases could trigger significant subscriber churn in a market where the majority of users are on free tiers to begin with. Nigeria's per capita GDP of approximately $2,000 makes streaming price hikes a real economic burden for millions of listeners. I think this dilemma — raise prices to fix royalties, or hold prices and keep royalties depressed — won't resolve cleanly in the short term, and Spotify may opt for cautious micro-increments rather than a decisive correction, meaning the 10x royalty gap persists well into the foreseeable future.

Looking further out over the medium term — roughly six months to two years — the structural dynamics of the Afrobeats economy could begin shifting meaningfully, even if the pace feels frustratingly slow. The biggest catalyst is investment capital flowing into African music infrastructure. Universal Music Group's 2024 acquisition of a stake in Nigeria's Mavin Global is an unambiguous signal that international capital markets are beginning to price African music IP seriously. Afreximbank's CANEX Creative Industries Fund has been expanded to $1 billion, directing institutional capital toward creative economy infrastructure across the continent. An IFC-Sony Creative Sector Partnership has launched with stated goals around digital infrastructure development and music industry workforce training. I predict that between 2027 and 2028, at least two to three Africa-based independent digital distributors will capture meaningful market share, and the foreign Big Three's combined control of Nigeria's streaming volume could fall from 68% to somewhere in the 55 to 60% range. That reduction alone would give African artists meaningfully more negotiating leverage — not just symbolically, but in the actual contract terms they're able to secure when signing distribution deals.

The sync licensing market represents a medium-term catalyst that doesn't receive enough serious attention in these discussions, and I think it deserves more. Global sync licensing — the business of placing music in advertisements, films, games, and streaming originals — is projected to grow from $5.9 billion in 2024 to over $12 billion by 2033. Afrobeats is increasingly showing up in global campaigns from Nike, Coca-Cola, and Netflix, and I predict Afrobeats sync revenues could triple to quintuple over the next two years as global brands double down on the genre's energy and demographic reach. The structural reason this matters is fundamental: sync deals are negotiated on a per-placement basis, entirely disconnected from subscription-based royalty rates. A Lagos-produced track and an LA-produced track both command the same sync licensing fee from Nike. This bypasses the geographic royalty penalty entirely. Africori's success in recovering proper revenues from Master KG's "Jerusalema" — achieved largely through metadata corrections alone — demonstrates that when rights administration mechanics work correctly, the economics can reverse dramatically. Sync licensing is, in my view, the most practical near-term pathway for African artists to escape the structural trap that streaming royalties have become.

Over the longer arc — 2028 to 2031 — Africa's music streaming market will be operating in a completely different weight class than it does today. Mobility Foresights projects the African music streaming market will expand from $1.25 billion in 2025 to $4.96 billion by 2031, a compound annual growth rate of 25.5%. Nigeria's music industry has set an internal target of $10 billion by 2030. Africa's smartphone penetration is expected to rise from approximately 37% today to over 60% by 2030, which would expand the paid streaming subscriber base three to four times over current levels. If 5G infrastructure rollout proceeds as planned, falling data costs will make streaming consumption patterns in Africa converge toward developed-world norms. These are genuinely exciting projections that deserve to be taken seriously as indicators of structural change to come.

But market size and equitable distribution are entirely different things, and the history of extractive economies teaches us they do not naturally converge. If the structural inequities in royalty distribution, master rights ownership, and CMO infrastructure aren't actively addressed through deliberate policy and business model reform, a bigger pie will simply mean larger absolute revenues flowing to foreign labels and platforms — while African artists' relative share stays flat or deteriorates. This is precisely the dynamic of 19th and 20th century resource extraction: Africa's raw materials fueled industrialization in Europe and North America, while Africa's economies remained structurally excluded from the wealth they generated. Drawing that parallel is not alarmism. The geometric pattern of resource flows, value capture, and profit repatriation is too consistent and too persistent to attribute to market coincidence.

The longest-range wild card in this picture is AI-generated music, and it worries me considerably more than most current industry commentary acknowledges. Deezer reported in January 2026 that it was receiving 60,000 AI-generated tracks per day, with 85% accompanied by anomalous streaming patterns consistent with artificial play inflation. If AI systems learn to produce Afrobeats-style tracks at industrial scale — and they can; the genre's sonic fingerprints are among the most learnable in contemporary music — the royalty pool gets diluted and authentic African artists earn even less per stream than they do today. African creators, already operating at a structural disadvantage, would absorb the heaviest impact from AI music flooding precisely because Africa's underdeveloped CMO infrastructure lacks the technical and administrative capacity to identify, challenge, and exclude AI-generated content from royalty calculations. Harvard CSASE's warning about structural income losses driving talented African artists away from music careers accelerates catastrophically when combined with an AI-generated music wave that further compresses already inadequate per-stream earnings.

There are already emerging reports from Nigeria of talented young musicians pivoting to tech and fintech because streaming economics don't support a music career for anyone outside the top fraction of one percent. A monthly streaming income sufficient to pay Lagos rent requires hundreds of millions of streams — a threshold statistically inaccessible to all but a handful of artists. If that brain drain continues at scale for another five to ten years, the cultural soil that Afrobeats grows in could genuinely be depleted — and that would be an irreversible loss, not merely an economic one.

Let me lay out the three scenarios explicitly, because precision matters here more than strategic optimism.

In the bull scenario, African CMO reform, Spotify price normalization, growth of independent African distributors, and expanded sync licensing revenues all converge simultaneously. Sub-Saharan Africa's recorded music revenues climb to $500 to $600 million by 2030, and the region's global market share rises to 1.5 to 2%. Nigerian artists' international royalty collection rates surpass 25%, and a substantial portion of the $286 million in unclaimed annual royalties gets recovered and properly distributed. The Africori-Jerusalema model becomes a replicable industry standard rather than an exceptional outlier. I put the probability of this scenario at roughly 20 to 25%. Every favorable condition has to materialize simultaneously, which keeps the odds modest — but if a virtuous cycle ignites, progress could come faster than current trend lines suggest.

In the base scenario, the current growth trajectory continues but structural gaps close only gradually and frustratingly slowly. Africa's streaming growth rate continues to outpace Goldman Sachs's projected global CAGR of 8%, but the per-stream geographic royalty gap persists through 2030 — still roughly $300 to $400 per million streams in Nigeria versus $3,000 to $4,000 in the United States, a gap representing more than 70% payout disparity. Sub-Saharan Africa's music revenues reach $300 to $400 million by 2030, global market share lands around 0.7 to 1.0%, and CMO reform yields real results in Nigeria while remaining stagnant elsewhere. The Big Three foreign labels ease from 68% to 55 to 60% market share in Nigeria through the growth of independent distributors. This is the "things are getting better, but the fundamentals haven't changed" scenario, and I assign it 50 to 55% probability. It is the most likely outcome — and simultaneously the most frustrating one.

The bear scenario is uncomfortable to reason through, but intellectual honesty requires it. Sixty-three percent of Africa's population still lacks mobile internet connectivity, and if digital infrastructure investment disappoints, CMO governance crises remain entrenched across key markets, AI-generated music floods and dilutes the royalty pool, and a global economic slowdown compresses streaming subscription growth, the numbers turn genuinely grim. Sub-Saharan Africa's global market share stagnates at 0.3 to 0.4%, unclaimed royalties accumulate past $500 million in aggregate, and the continent's next generation of music talent migrates to other industries in significant numbers. With Kenya's MCSK under operating suspension and South Africa's SAMRO simultaneously undergoing forensic audit, a combined CMO reform failure and AI music surge is not a remote tail risk scenario. I assign this scenario 20 to 25% probability.

One final note on where my analysis could prove wrong in either direction. If Spotify or Apple Music voluntarily establish a geographic royalty equalization fund — essentially compensating artists in low-subscription-price markets to narrow the 10x gap — or if the African Union fast-tracks a continent-wide digital music regulation modeled on the EU's Copyright Directive, the timeline for improvement could compress dramatically. A regulatory framework forcing real-time transparency on African royalty distributions would be a genuine structural game-changer that my base scenario does not currently price in. In the opposite direction, if the entire global music industry undergoes a paradigm shift toward AI-generated content and human artist revenues collapse industry-wide, the African music crisis expands from a regional structural problem into a universal industry crisis — one where African artists are simply the first and most severely affected. Both of these represent plausible but non-consensus outcomes that deserve serious monitoring.

What I am confident about is this: if Afrobeats is in your playlist — and statistically, there is a reasonable chance it is — it is worth pausing for a moment to think about what the artist who created that track actually earns from your listen. Changing the structural reality is the job of policymakers and platform executives. But understanding that structure is something all of us can do. Afrobeats has the potential to break through this paradox. But that breakthrough will not come from organic market growth alone. It can only come from conscious, deliberate structural transformation — and every year it is delayed, the cost falls on the people who made the music.

Sources / References

- Global Music Report 2026 — IFPI

- Global Music Report 2025 — IFPI

- 5 Years in Nigeria: Music Trends — Spotify Newsroom

- Harvard Report Warns Africa of Losing Economic Value from Afrobeats Boom — Vanguard Nigeria

- Nigerian Artists Earn 90% Less from Local Streams Than U.S. and U.K. Markets — Nairametrics

- African Artists Face a Geographic Penalty in Streaming Payouts Despite 22% Revenue Growth — Ecofin Agency

- CISAC 2025: African Music Royalty Growth — Afro Soundtrack

- Unlocking Africa's Untapped $286 Million Music Economy — CNBC Africa

- Foreign Music Distributors Control 68% of Nigeria Streaming Market — Daba Finance

- Spotify Royalties to Nigerian and South African Artists Surged to $59 Million in 2024 — Arise News