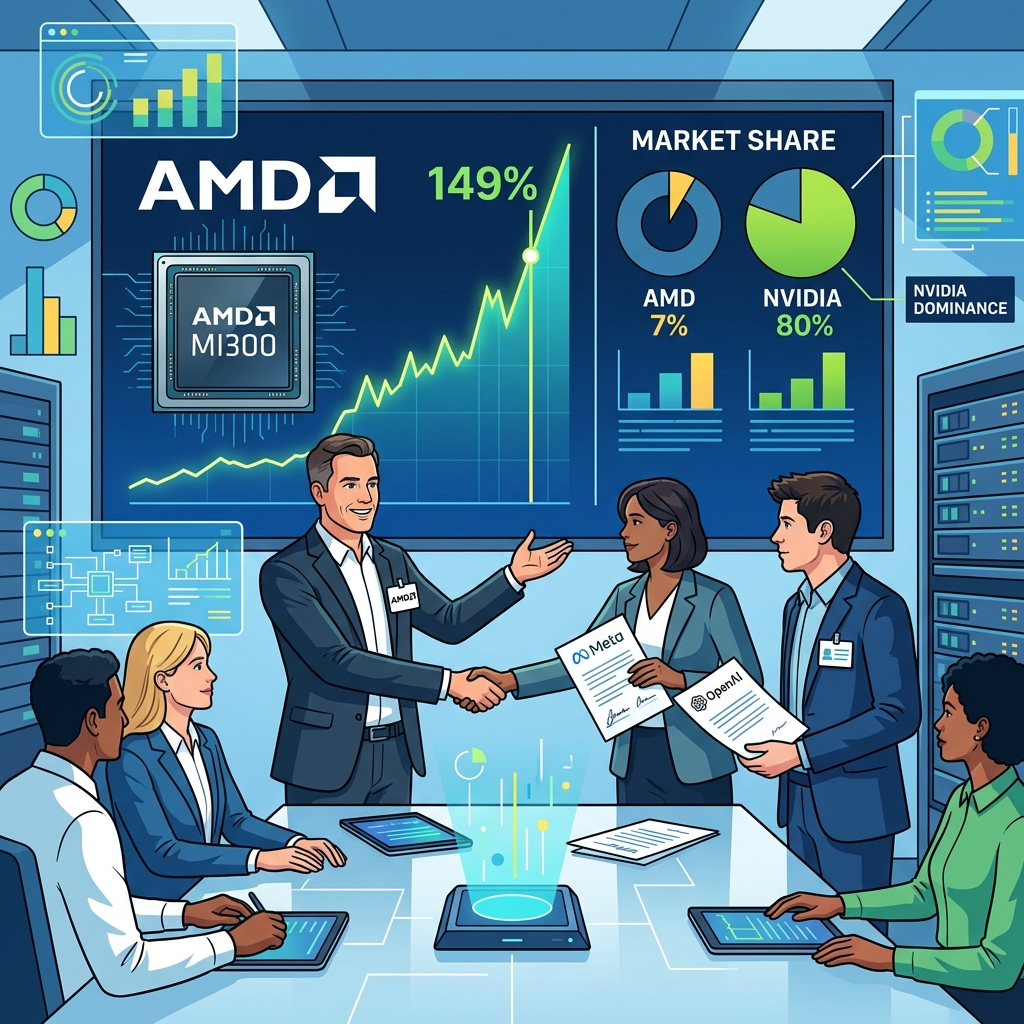

AMD at 7% Market Share, Up 149% — The Real Story Behind Betting on the Runner-Up

Summary

AMD's stock has surged 149% year-to-date in 2026 — the highest single-stock return in the entire semiconductor sector — while its actual AI accelerator market share sits at a stubborn 5–7%, creating one of the starkest mismatches between valuation and competitive position in recent technology market history. First-quarter 2026 revenues of $10.25 billion, up 38% year-over-year with a data center segment now representing 57% of total sales, demonstrate genuine business momentum that few large-cap semiconductor companies can match in absolute dollar terms. Yet the twin megadeals at the center of the AMD bull narrative — Meta's $60 billion five-year AI infrastructure contract and OpenAI's six-gigawatt GPU deployment commitment — reveal on closer examination that the primary driver of AMD's premium is not hardware superiority but hyperscalers' deep-seated fear of NVIDIA's CUDA monopoly strangling their long-run pricing leverage. AMD currently trades at 84x trailing earnings versus NVIDIA's 25x, an inversion of normal market logic where dominant leaders command higher multiples than challengers, implying markets are pricing AMD as a structurally necessary alternative rather than a technology leader earning its premium through competitive wins. The upcoming MI450 GPU and Helios rack-scale system launches in the second half of 2026, combined with the maturation timeline of AMD's ROCm software ecosystem and the pace at which hyperscaler-designed custom silicon eats into the third-party GPU market, will collectively determine whether AMD can convert its alternative premium into durable, technology-driven competitive advantage.

Key Points

The 7% Market Share vs. 149% Stock Gain Paradox

AMD's 149% year-to-date stock gain in 2026 is the highest return in the semiconductor sector by a wide margin, yet the company holds only 5–7% of the AI accelerator market by revenue — a divergence that cannot be explained by conventional valuation logic. In most market environments, a stock rising this aggressively would belong to either a dominant market leader or a company rapidly expanding its competitive position, and AMD currently fits neither description. NVIDIA retains more than 80% of AI accelerator revenue share, meaning AMD's 7% slice is not the result of competitive inroads but rather an enduring structural reality that has persisted through AMD's entire MI300-series product cycle. Q1 2026 revenues of $10.25 billion and 38% year-over-year growth are objectively impressive figures, but they alone cannot arithmetically explain a 149% stock advance when the company's revenue base is still a fraction of NVIDIA's scale. What actually explains the gap is that markets are assigning a structural premium to AMD's position as the only credible alternative to a monopolist supplier — a kind of "fear of NVIDIA" trade that inflates AMD's price beyond what fundamentals alone would justify. This premium is real and persistent as long as NVIDIA's dominance remains threatening to the hyperscalers who depend on it, but it is also categorically different from the kind of valuation support that comes from genuine competitive leadership. Investors who conflate AMD's stock performance with AMD's competitive performance are looking at two very different stories that happen to be producing the same headline number at this particular moment in time.

The Meta-OpenAI 12-Gigawatt Double Deal and What It Really Signals

Meta's $60 billion five-year AI infrastructure partnership with AMD and OpenAI's six-gigawatt GPU deployment commitment — combining for 12 gigawatts of total AMD compute procurement — represent the largest dual-vendor hardware commitment in the history of the AI industry, and the surface-level narrative describes this as unambiguous validation of AMD's technology credentials. The deeper read, however, looks quite different: both Meta and OpenAI entered these agreements not because AMD's hardware is categorically superior to NVIDIA's, but because concentrating 80–90% of their AI compute dependency on a single supplier had become strategically untenable. A monopolist supplier can allocate scarce capacity toward favored customers, price with minimal competitive pressure, and effectively hold customer product roadmaps hostage during supply-constrained periods — all of which NVIDIA was in a position to do. By funding AMD at scale, Meta and OpenAI restored leverage in their NVIDIA negotiations, and the $60 billion contract can be read as much as a threat to NVIDIA's pricing power as it is an endorsement of AMD's silicon. What makes this read even more convincing is the simultaneous behavior of both customers: Meta is actively deploying MTIA generation 4 custom silicon in parallel with its AMD procurement, and OpenAI is running its own internal chip development program. The companies signing AMD's largest-ever contracts are building the replacements for AMD's chips at the same time. This "strategic temporary marriage" dynamic is something AMD investors need to hold alongside the headline contract numbers when modeling the durability of AMD's revenue relationships with these two customers beyond the current contract horizons.

How CUDA's Software Monopoly Created AMD's “Alternative Premium”

Understanding AMD's 149% gain requires first understanding what CUDA actually is and why it creates the kind of structural fear that drives hyperscaler capital toward AMD. CUDA is not simply a programming interface for NVIDIA GPUs — it is 20 years of accumulated developer tools, optimized libraries, framework integrations, and community knowledge that has become so deeply embedded in AI development workflows that switching away from it carries significant real-world costs even when alternative hardware is technically competitive. Virtually every major AI framework — PyTorch, TensorFlow, JAX — received its first-class CUDA optimization years before ROCm support was available, and specialized CUDA libraries like cuDNN, TensorRT-LLM, FlashAttention 3, and NCCL still have no ROCm equivalents at equivalent production maturity. This lock-in effect means hyperscalers pay a "NVIDIA tax" not just on hardware prices but on their entire AI development infrastructure, and it is the fear of that tax compounding indefinitely that has pushed them to invest in AMD as a counterweight. The paradox this creates for AMD investors is instructive: AMD's "alternative premium" is strongest precisely when CUDA's monopoly is strongest, and it weakens as CUDA's grip loosens. If ROCm matures to the point where switching costs are negligible, AMD's hardware competes purely on specs and price — which is a more demanding competition but one with a broader addressable market. My view is that ROCm crossing approximately 90% functional parity with CUDA by late 2027 will mark the inflection where AMD's premium transitions from primarily sentiment-driven to primarily fundamentals-driven — a structural shift that AMD investors should be actively tracking.

84x Earnings vs. NVIDIA's 25x — Why the Challenger Costs More Than the King

AMD's 84x trailing price-to-earnings ratio versus NVIDIA's approximately 25x is arguably the most analytically interesting valuation anomaly in the semiconductor sector today, because it inverts the standard expectation that dominant market leaders command higher multiples than challengers. In most industries and most market cycles, the company with 80%+ market share trades at a premium to the company with 7% share — investors pay up for the durability, pricing power, and ecosystem depth that come with market leadership. In the AI accelerator market in 2026, this relationship is precisely reversed, and understanding why reveals something important about how the market is thinking about AMD. The trailing P/E divergence reflects the fact that NVIDIA has already captured so much market share and revenue that its current earnings base is enormous, compressing its multiple, while AMD's earnings base is still small relative to its potential earnings in a scenario where it captures 15–20% of a $400–600 billion AI accelerator market. Essentially, markets are paying for AMD's future in a world where the AI accelerator market grows 5x or more from here, and AMD's data center revenues compound at 25–35% annually for the next three years. That scenario — which requires Helios and MI450 success, ROCm maturation, and continued hyperscaler buying — is plausible but optimistic. There is also a paradoxical structural logic embedded in AMD's premium: AMD investors win both when NVIDIA succeeds (expanding AI spending lifts AMD with it) and when NVIDIA faces antitrust or supply constraints (AMD captures displaced demand). That double-sided payoff structure commands a premium that no single-path investment thesis normally receives.

Hyperscaler Custom Silicon — AMD's Most Overlooked Long-Term Competitor

The most systematically underweighted risk in most AMD bull cases is not NVIDIA's competitive response but the maturation of hyperscaler in-house silicon development programs. Meta's MTIA is currently in its fourth generation with production deployment underway. Amazon's Trainium 2 began mass production in Q2 2026 and claims 50% cost improvements versus GPU alternatives. Google's TPU lineup powers more AI computation than any other custom chip program in the world. Microsoft's Maia is advancing on a parallel development track targeting the same Azure data center footprint that AMD's MI-series is also serving. These are not speculative future programs — they are shipping silicon in production workloads at the customers who have just signed AMD's largest-ever contracts. Tom's Hardware's 2026 analysis of the custom ASIC landscape estimates that hyperscaler custom silicon is already growing at a 27% compound annual rate, double the pace of the GPU market. I project that by 2027–2028, the four major hyperscalers will shift 25–35% of their internal AI compute workloads to in-house designs from the current 10–15%. This creates a structural revenue ceiling for AMD with its most valuable customers: the existing contracts will be honored, but renewal volumes and pricing leverage will shift as hyperscalers' in-house alternatives mature. The partially offsetting factor — and this is the paradox AMD investors need to hold — is that hyperscaler custom silicon competes against NVIDIA at roughly the same rate as against AMD, so if the third-party GPU market as a whole contracts, AMD's relative position within it may actually improve even as its absolute revenue trajectory faces headwinds.

Positive & Negative Analysis

Positive Aspects

- Exceptional Revenue Growth and a Decisive Data Center Pivot

AMD's Q1 2026 revenue of $10.25 billion and 38% year-over-year growth rank among the highest top-line growth rates achievable for a semiconductor company of AMD's scale, and the composition of that growth tells an even more important story. Data center revenue reaching $5.8 billion — 57% of total company revenue, up from 42% one year ago — signals that AMD has completed a fundamental business model transformation from a PC CPU company into an enterprise AI infrastructure provider. This is not merely a mix shift in reported segments; it represents a permanent change in AMD's earnings quality, since data center revenue carries higher gross margins, more predictable purchasing cycles, and better visibility into forward demand than consumer-facing segments. The earnings surprise itself — $1.37 Non-GAAP EPS against a $1.27 consensus — was the fifth consecutive quarter in which AMD beat analyst expectations on the bottom line, establishing a track record of under-promising and over-delivering that reduces guidance risk premium in the stock. Lisa Su's public guidance of $11.2 billion for Q2 2026 implies AMD's annualized revenue run rate is approaching $45 billion, and if the data center segment continues compounding at its current rate, AMD's 2027 data center revenues alone could approach $26–28 billion based on current trajectory.

- Hyperscaler Dual-Contract Pipeline Stability

Meta's five-year, estimated $60 billion AI infrastructure contract and OpenAI's six-gigawatt GPU deployment commitment — totaling an unprecedented 12 gigawatts of committed AMD compute capacity — collectively represent the most durable revenue pipeline in AMD's corporate history. Five-year contract structures of Meta's scale are genuinely unusual in the semiconductor industry, where most procurement cycles run 12–18 months, and the multi-year commitment substantially reduces AMD's exposure to quarter-to-quarter demand variability that has historically made AMD's revenue harder to forecast than NVIDIA's more predictable data center ordering patterns. Having two of the world's most visible and resource-rich AI customers simultaneously on multi-year AMD commitments creates a powerful reference effect for other hyperscalers evaluating AMD adoption: if Meta and OpenAI trust AMD at this volume, the vendor validation risk that might otherwise give a CTO pause is substantially reduced. This reference effect is already producing downstream interest: Oracle has publicly announced plans for a 50,000-GPU AMD MI450 cluster deployment, suggesting AMD's large-customer momentum is generating follow-on business beyond the original two megadeals. The combined 12-gigawatt commitment also provides meaningful production visibility for TSMC capacity allocation, which improves AMD's ability to negotiate favorable pricing and priority access for the advanced packaging technologies that are currently supply-constrained across the entire AI semiconductor industry.

- MI450 and Helios as Next-Generation Technology Proof Points

AMD's current hardware foundation — the MI300X with its 192GB HBM3E memory configuration — has already demonstrated competitive or superior performance versus NVIDIA's H100 in large language model inference workloads, giving AMD a credible baseline from which MI450 and Helios will launch. The MI450 architecture is expected to bring a generation-over-generation advance in both compute density and memory bandwidth, with AMD's Helios rack-scale system packaging 72 MI455X accelerators with 31 terabytes of HBM4 memory delivering 2.9 FP4 exaflops of inference compute according to NextPlatform's reporting. This is AMD's most direct answer to NVIDIA's NVL72 rack-scale system and the strongest signal yet that AMD is competing at the full-stack system level rather than just selling discrete GPUs into existing infrastructure. Competing at the system level carries significant strategic value: it allows AMD to capture a larger share of total customer AI infrastructure spend per installation, strengthens the relationship between AMD engineers and customer infrastructure teams, and meaningfully raises switching costs once a customer has deployed a Helios rack-scale environment. Oracle's planned 50,000-GPU AMD cluster deployment specifically references MI450 hardware, suggesting the market is already anticipating Helios-class deployments in production environments within the next 12 months.

- Lisa Su's Proven Execution Track Record as a Valuation Multiplier

Lisa Su's ability to execute consistently against aggressive roadmaps over a sustained period has earned what markets call a management premium — a willingness to pay a higher earnings multiple than the company's current fundamentals alone would justify. When she joined AMD as CEO in 2014, the company's stock was trading around $2, the balance sheet was strained, and Intel was winning the CPU performance race at every market segment from consumer laptops to enterprise servers. Over the subsequent decade, she orchestrated Zen architecture to restore AMD's CPU performance leadership against Intel across all price tiers, built EPYC into a server CPU product line now claiming 46.2% of server CPU revenue market share as of Q1 2026, and pivoted the company's R&D and manufacturing partnerships toward AI accelerators before most competitors recognized the scale of the AI infrastructure opportunity. This consistent track record of identifying secular trends early, executing product roadmaps on schedule, and taking share from larger incumbents is the kind of demonstrated capability that market participants genuinely discount into a stock price at a premium to peers. The cousin dynamic with NVIDIA CEO Jensen Huang is an amusing footnote, but the more substantive point is that two of the most respected execution-track-record CEOs in global semiconductors are now in direct competition for the same infrastructure dollars, and Lisa Su has given investors every reason to believe AMD can hold its own in that contest.

- The Permanent Second Place Math in an Expanding Total Addressable Market

The most underappreciated element of the AMD bull case is not the prospect of overtaking NVIDIA, but the sheer arithmetic of what a stable 15% market share position means as the AI accelerator total addressable market expands toward the ranges multiple research firms are projecting. Bloomberg Intelligence forecasts the AI accelerator market exceeding $600 billion by 2033, growing at 16% compound annual rate from the $116 billion recorded in 2024; Goldman Sachs projects annual AI capital expenditure reaching $1.6 trillion by 2031. At 15% share of a $600 billion AI accelerator market, AMD generates $90 billion in AI accelerator revenue alone — more than double AMD's current total company annual revenue of roughly $40 billion. This is the mathematical case for AMD without requiring AMD to win any head-to-head benchmark competition with NVIDIA: the market grows fast enough that being a well-positioned, technically credible number two generates revenues that are enormous in absolute terms. AMD demonstrated the viability of this playbook in the x86 CPU market, where EPYC captured 46% of server CPU revenue despite Intel retaining unit volume leadership, by focusing on the high-margin, high-value portions of the market where AMD's cost-efficiency advantages were most decisive.

Concerns

- The CUDA Ecosystem Switching Cost as an Enduring Structural Barrier

CUDA has been accumulating developer tools, optimized libraries, and deep framework integrations since 2006 — nearly 20 years of compounding ecosystem depth that represents the most durable competitive moat in the AI infrastructure landscape. The practical consequence is that every enterprise team working on serious AI development has built pipelines, tooling, debugging workflows, and institutional knowledge on top of CUDA, and migrating those assets to ROCm imposes real costs in engineering time, testing, and production risk that do not disappear simply because AMD's hardware performance converges toward parity. Current research from Spheron shows ROCm achieving 90–95% of H100 throughput on standard PyTorch inference workloads, which is a meaningful improvement, but this throughput figure obscures the gaps that matter most in enterprise production: CUDA-specific training libraries like TensorRT-LLM, FlashAttention 3, cuDNN, and the NCCL collective communications library still lack mature ROCm equivalents, which means AMD GPUs remain noticeably inferior for the large-scale distributed training workloads that consume the most compute budget at hyperscalers. AMD's ROCm team is working aggressively to close these gaps, and the trajectory is clearly positive, but the ecosystem depth that took NVIDIA 20 years to build cannot be replicated in two or three years of accelerated investment regardless of how well AMD's engineers execute. Any enterprise considering an AMD adoption today must budget for meaningful software migration costs that are entirely separate from the hardware acquisition decision, and this friction serves as an effective brake on AMD's penetration of customers who are not large enough to absorb those migration costs with dedicated teams.

- Hyperscaler Custom Silicon as a Structural Revenue Ceiling

The single most important structural risk for AMD's long-term growth trajectory is not NVIDIA's competitive response to MI450 but the maturation of hyperscaler in-house AI chip programs that will progressively reduce the addressable market available to any third-party GPU vendor. Meta's MTIA is in its fourth generation with active production deployment; Amazon Trainium 2 entered mass production in Q2 2026 with claims of 50% cost improvements versus GPU alternatives; Google's TPU deployment scale leads all custom silicon programs; and Microsoft's Maia is advancing in parallel. Tom's Hardware's 2026 analysis estimates hyperscaler custom silicon is growing at 27% compound annual rate, double the pace of the GPU market, and I project that by 2027–2028 the major hyperscalers will shift 25–35% of their internal AI compute to in-house designs from the current 10–15%. This means the customers who just signed AMD's largest-ever contracts are simultaneously building their way out of needing AMD at the same volumes in the medium term. The existing contracts will be honored, but renewal volumes will face downward pressure as custom silicon matures, and the pricing leverage that Meta and OpenAI bring to any renegotiation will be substantially stronger in 2028 than it is today.

- The 84x P/E Valuation Premium and Its Vulnerability to Disappointment

AMD's trailing price-to-earnings ratio of approximately 84x embeds a very specific and demanding set of assumptions about AMD's future competitive position that must all be approximately correct for the current valuation to be justified. At a minimum, the market is pricing in AMD's data center revenues compounding at 25–30% annually for the next two to three years, AMD's AI accelerator market share expanding from the current 7–9% toward 15%+ by 2028, and MI450 and Helios executing without meaningful delays or benchmark underperformance. If any one of these conditions fails to materialize — a Helios production slip, an MI450 benchmark that disappoints versus Blackwell, or hyperscaler custom silicon adoption accelerating faster than expected — the valuation compression could be swift and severe. The June 2026 semiconductor selloff demonstrated this vulnerability empirically: when Broadcom's earnings disappointed on AI networking revenue, AMD fell over 16% from its 52-week high to $466 despite AMD-specific fundamentals remaining unchanged. High-multiple growth stocks historically reprice faster and further on sentiment shifts than earnings-based multiples, because the premium embedded in the valuation has no fundamental floor — it exists only as long as the narrative remains intact.

- Extreme Selloff Sensitivity Amplified by the Alternative Premium Structure

AMD's June 2026 selloff experience — declining from a 52-week high near $558 to a low of $466, a drop of over 16% in days triggered by Broadcom earnings rather than any AMD-specific news — reveals an important structural characteristic of how AMD's stock behaves under macro or sector stress. Because a significant portion of AMD's valuation premium is sentiment-driven rather than earnings-driven, AMD is particularly exposed to episodes where risk sentiment deteriorates across the semiconductor sector or the broader technology universe. The Philadelphia Semiconductor Index dropped 6–10% during the June episode; AMD's decline was roughly proportional at the high end or worse, reflecting the additional vulnerability of a high-multiple stock with a narrative-dependent premium. This is not simply normal sector beta amplification — it reflects the specific nature of AMD's alternative premium, which, like all sentiment-driven premiums, compresses rapidly when market participants reduce their tolerance for speculative risk. AMD recovered from $466 to $537 by June 18, a 15% rebound in under two weeks, but the round-trip illustrated the kind of 20%+ drawdowns that AMD shareholders have to be prepared to absorb in normal market episodes.

- The Strategic Temporary Marriage Expiration Risk

The most structurally complex risk for AMD over a three-to-five year horizon is the possibility that its two largest customer relationships — Meta and OpenAI — were never intended to be permanent commitments but rather temporary diversification trades that expire as each company's in-house silicon capabilities mature. Meta entered its $60 billion AMD contract while simultaneously running MTIA generation 4 in production; OpenAI signed its six-gigawatt commitment while actively developing its own internal AI chip program. These are not the behaviors of companies that have chosen AMD as their long-term strategic compute partner — they are the behaviors of companies using AMD as a bridge technology while their preferred long-run solution matures. The current contracts provide meaningful revenue security through their initial terms, but the renewal negotiating environment in 2028–2029 will be fundamentally different: by then, Meta's MTIA and OpenAI's custom chips will be further along, AMD's leverage as the only credible alternative will have diminished, and both companies will have internal benchmarks demonstrating what their own silicon can do at scale. Additionally, if NVIDIA responds to AMD's customer gains by aggressively pricing its CUDA platform or by opening up portions of its software ecosystem, the hyperscalers' motivation to maintain AMD as a funded alternative diminishes significantly — and the premium AMD currently receives for filling that structural role could deflate rapidly and with limited warning.

Outlook

The most immediate catalyst for AMD's stock over the next one to six months is the planned H2 2026 launch of the MI450 GPU and Helios rack-scale system. Both Bank of America's $560 price target and Citi's $575 target assume MI450 ships on schedule and posts competitive benchmark results against NVIDIA's Blackwell architecture. If MI450 delivers performance at parity or better in the workloads that matter most to hyperscalers — large model training throughput, inference latency at scale, and energy efficiency — I'd put $600 during 2026 as a live possibility rather than just an analyst target. NextPlatform's reporting indicates the Helios rack-scale system will pack 72 MI455X accelerators, deliver 2.9 FP4 exaflops of inference compute, and integrate 31 terabytes of HBM4 memory — a genuinely formidable specification on paper. The critical risk is the execution timeline: NextPlatform's analysis suggests that while engineering samples are on track for H2 2026, meaningful production volume ramping may not begin until Q2 2027. If Helios production volumes slip from H2 2026 samples to Q2 2027 mass production, the market's patience with AMD's 84x P/E will face real pressure. A meaningful Helios timeline delay could pull AMD back toward the June 2026 low of $466, and sentiment-driven stocks often overshoot on the downside when a key narrative catalyst disappoints.

The Q2 2026 earnings report — expected in late July or early August — will serve as the first concrete test of whether AMD's megacontracts are translating into accelerating recognized revenue. AMD's Q2 guidance of $11.2 billion implies roughly 9% sequential growth, but the more important question is whether the data center segment is running materially ahead of that headline figure, driven by early MI450 ramp deployments into Meta's and OpenAI's infrastructure. I think Q2 data center revenue has a reasonable shot at posting 15–20% sequential growth versus Q1's $5.8 billion, which would push AMD's annualized data center run rate well above $30 billion and start making the current valuation more arithmetically defensible when measured on a forward basis. The Federal Reserve's rate environment introduces an independent variable: Fed Chair Kevin Warsh's policy signals will directly affect growth stock multiples across the board, and AMD at 84x trailing earnings is exactly the kind of high-multiple name that reprices sharply when the risk-free rate outlook shifts. For short-term trading purposes, I'd frame AMD's current fair range as $466 to $575, with MI450 benchmark releases and Q2 earnings as the two decisive data points for determining where within that range the stock settles.

Stepping back to a six-month to two-year medium-term view, the ROCm software ecosystem's maturation trajectory is arguably the more consequential variable than any individual product launch. AMD can win head-to-head hardware benchmark comparisons with NVIDIA and still fail to capture meaningful incremental market share if the software experience remains noticeably inferior in production environments. The current data is genuinely encouraging: Spheron's 2026 analysis shows ROCm achieving 90–95% of H100 throughput on PyTorch and vLLM inference workloads, a significant improvement over the 60–70% parity figures of two years prior. But raw throughput convergence is not the same as ecosystem convergence. CUDA's specialized libraries for training — cuDNN, TensorRT-LLM, FlashAttention 3, and NCCL — still have no ROCm equivalents of comparable production maturity, which means AMD GPUs remain meaningfully inferior for heavy training workloads at enterprise scale. My working assumption is that ROCm will cover approximately 90% of CUDA's core functionality by late 2027. When that threshold is crossed, the population of mid-sized AI companies that have been holding off on AMD due to software friction will begin adopting MI-series hardware in volume. That is the inflection point that moves AMD from 9–10% share toward the 15–20% range — and if it materializes on that timeline, the mathematics of an expanding AI accelerator market make AMD a dramatically larger business than it is today.

The medium-term wildcard is the hyperscaler custom chip maturation timeline, which will determine how much of AMD's near-term contract revenue translates into sustained long-term relationships versus one-time diversification trades. Meta's MTIA is in its fourth generation with production deployment underway; Amazon's Trainium 2 began mass production in Q2 2026 with claimed 50% compute cost improvements; Google's TPU lineup leads all custom silicon in raw deployment scale; and Microsoft's Maia is advancing on a parallel roadmap. I project that by 2027–2028, the four major hyperscalers will shift 25–35% of their internal AI compute workloads to in-house silicon, up from the current estimated 10–15%. This represents a structural ceiling on AMD's revenue-per-customer trajectory with its most important accounts. What partially offsets this concern — and this is the paradox AMD investors need to internalize — is that hyperscaler custom silicon takes share from NVIDIA at roughly the same pace as from AMD. If the overall third-party GPU market shrinks as a proportion of total AI compute spending, but AMD maintains its current 7–10% share of that market, AMD still grows in absolute revenue because the AI infrastructure market itself is expanding fast enough to more than compensate.

Extending the view to two to five years, the total addressable market numbers change the conversation at a fundamental level. Bloomberg Intelligence projects the AI accelerator market will exceed $600 billion by 2033, growing at a 16% compound annual rate from $116 billion in 2024. Goldman Sachs projects annual AI capital expenditures reaching $1.6 trillion by 2031, with hyperscalers and Tier-2 cloud providers committing more than $3.5 trillion in AI-related capital expenditures through 2030 alone. Within that expansion, AMD capturing 15% market share would imply AI accelerator revenue of $90 billion or more annually — versus AMD's current total company revenue of roughly $40 billion per year. The arithmetic of being a credible number two in an exploding market is genuinely compelling, even without ever directly overtaking NVIDIA. AMD demonstrated the same principle in server CPUs: the EPYC lineup never needed to defeat Intel on every dimension to capture 46.2% of server CPU revenue market share by Q1 2026. AMD CEO Lisa Su has publicly set a goal of serving a $120 billion server CPU TAM by 2030, more than double prior estimates, driven by agentic AI's intensifying demand for CPU-side compute. AMD is positioning itself as the only company offering the full range of compute engines — GPUs, CPUs, NPUs, and custom accelerators — which reduces its single-product risk and provides more durable exposure to multiple AI infrastructure spending streams.

The long-term wildcard that could reframe AMD's competitive position entirely is the potential erosion of CUDA's software monopoly from below. Open-source AI frameworks are progressively moving toward hardware-agnostic compilation layers: OpenAI's Triton compiler and the MLIR intermediate representation are two concrete examples of infrastructure designed to reduce vendor lock-in at the software abstraction level. If by 2028–2029 a substantial proportion of AI workloads can run efficiently on hardware-neutral software stacks, AMD's physical hardware would compete purely on performance, memory bandwidth, and energy efficiency metrics rather than fighting against a software ecosystem disadvantage. In that environment, AMD's CDNA architecture — backed by TSMC's advanced process nodes and AMD's established relationships across the hyperscaler customer base — could be genuinely competitive across a broader range of workloads than it is today. There is also a geopolitical dimension that deserves acknowledgment. China currently represents approximately 20% of AMD's total revenue, a figure Lisa Su has confirmed publicly. U.S. semiconductor export control tightening creates meaningful downside risk for that exposure, particularly if higher-capability MI-series chips face additional licensing scrutiny. However, in any scenario where NVIDIA faces more severe export restrictions than AMD, AMD becomes the primary beneficiary of redirected Chinese procurement — and AMD has been developing lower-specification chip variants explicitly designed to remain within export control thresholds.

Let me put the scenarios in concrete terms for investors trying to frame a position. In the bull case — which I assign approximately 25% probability — MI450 outperforms Blackwell architecture on critical benchmarks, Helios ramps ahead of schedule, and ROCm achieves meaningful ecosystem parity by late 2027. AMD's AI accelerator market share climbs to 18–20% by 2028, data center revenues approach $30 billion annually, and the stock has a credible path to $700–$800. A trillion-dollar market capitalization becomes mathematically achievable in this scenario, and TIKR's bull case analysis implies an IRR of approximately 48% annually for shareholders.

In the base case — which I put at 55% probability — MI450 delivers solid but unspectacular results, Helios ramps gradually from H2 2026 into 2027 production volume, and AMD's AI market share rises slowly toward 12–15% by 2028. The stock trades in the $500–$600 range as earnings growth compresses the valuation toward a more defensible 40–50x multiple; TIKR estimates this implies roughly 37% annual IRR. In the bear case — 20% probability — MI450 disappoints, Helios production slides into 2027, and hyperscaler custom silicon matures faster than expected, holding AMD's share flat at 5–7%. The P/E of 84x becomes untenable and the stock corrects toward $300–$350, though TIKR's bear case analysis still implies roughly 34% IRR, suggesting the downside floor is less catastrophic than simple multiple compression implies. Probability-weighted across all three scenarios, expected value lands near $550 — modestly above the current price of approximately $512.

Finally, I want to be transparent about the specific conditions that would cause my analysis to be wrong. If ROCm development accelerates beyond my expectations and achieves genuine CUDA production parity by early 2027 rather than late 2027, AMD's premium transforms from sentiment-driven to fundamentally justified — and the stock deserves a materially higher valuation than my base case implies. If U.S.-China geopolitical escalation constrains NVIDIA's global supply chain more severely and durably than AMD's, AMD could capture accelerated share in non-U.S. markets beyond what I have modeled. If NVIDIA makes a strategic decision to open-source significant portions of its CUDA software stack or to compete aggressively on pricing to reassert market share, AMD's hyperscaler-funding motivation diminishes rapidly — and AMD's alternative premium could deflate faster than most bulls currently assume. For investors weighing a position, I would suggest watching three specific data points over the next six months: MI450 benchmark releases versus Blackwell comparisons, the Q2 and Q3 2026 earnings trajectories for data center revenue growth rate, and any public statements from Meta or OpenAI about the pace of their own custom silicon deployment relative to AMD hardware ramp schedules. A staged entry in the $466–$512 range, with AMD representing no more than 5–10% of total portfolio exposure, reflects what I think is an appropriate risk-return framing given the wide dispersion of potential outcomes here.

Sources / References

- AMD Q1 2026 Earnings Report — CNBC

- AMD-Meta $60B Deal and NVIDIA AI Monopoly — TechI

- AMD vs NVIDIA AI GPU Market Share 2026 — Silicon Analysts

- AI Chip Stocks Sold Off — Yahoo Finance

- Chip Stocks Rebound Investment Strategy June 2026 — Intellectia

- AMD Stock Forecast 2026 — TIKR

- AMD Stock Analysis — Lisa Su, Meta, AI Client Accelerators — TradingKey